Are you leaving money on the table? For 2026, understanding your workplace retirement plans isn’t just about saving for the future. It’s about smart tax planning today. New contribution limits and critical updates from the IRS mean maximizing your 401(k) or other employer-sponsored plan can significantly reduce your tax bill. This also accelerates your financial growth. Don’t miss out on these five essential tips to make the most of your workplace retirement plans in 2026.

Executive Summary

- Maximize your 2026 contributions to reduce taxable income.

- Understand both pre-tax and Roth options for tax advantages.

- Always contribute enough to get your full employer match.

- Be aware of new SECURE 2.0 Act rules, especially for high earners.

- Regularly review your plan and consider professional financial advice.

Tip 1: Know Your 2026 Contribution Limits

Maximize Your Elective Deferrals

For 2026, the IRS has increased the amount you can contribute to many plans. You can contribute up to $24,500 to your 401(k), 403(b), most 457 plans, and the Thrift Savings Plan. This is your personal elective deferrals limit. SIMPLE IRA limits are $17,000. However, for companies with 25 or fewer employees, this limit rises to $18,100. Traditional and Roth IRA limits also increased to $7,500. Therefore, contributing the maximum can significantly boost your retirement savings.

Don’t Forget Catch-Up Contributions (Age 50 and Over)

Individuals aged 50 or older can contribute even more. The standard catch-up contribution for 401(k)s, 403(b)s, and most 457 plans is $8,000. Furthermore, under the SECURE 2.0 Act, individuals aged 60 to 63 can make an even larger “Super Catch-Up” contribution of $11,250. For SIMPLE IRAs, the catch-up limit is $4,000. This increases to $5,250 for those aged 60 to 63. Traditional and Roth IRA catch-up contributions are $1,100. These additional contributions offer a powerful way to accelerate your retirement savings.

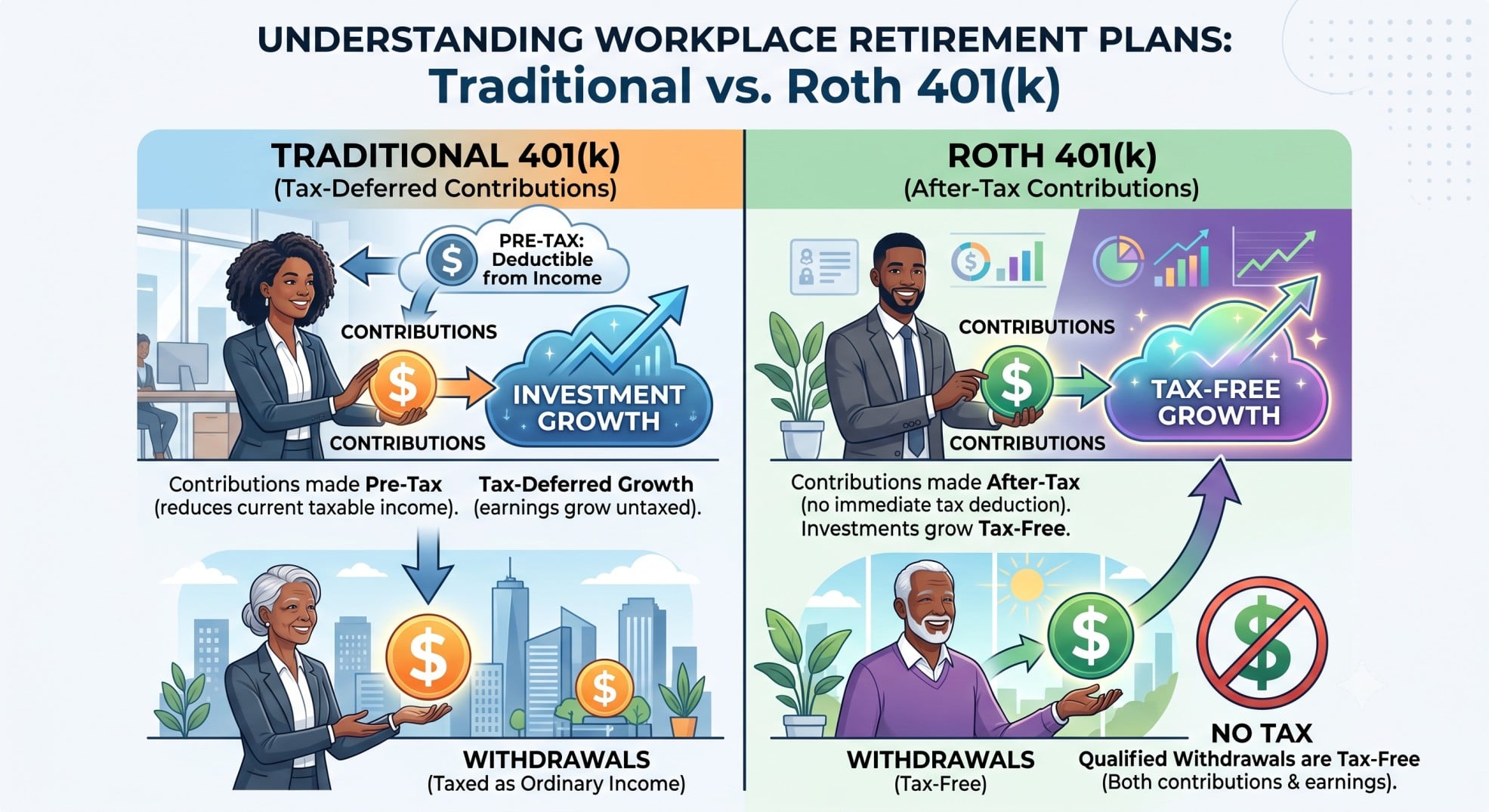

Tip 2: Understand the Tax Advantages

Pre-Tax Contributions Lower Your Taxable Income

Traditional 401(k) contributions are pre-tax. This means they reduce your current-year taxable income. Consequently, you pay less in taxes today. This immediate tax benefit makes pre-tax contributions very attractive. Consider Alex’s situation for 2026:

For 2026, consider Alex, a single general taxpayer residing in California, earning a gross annual salary of $150,000. Without utilizing a workplace retirement plan, Alex’s tax obligations would be substantial. Based on estimated 2026 federal and California state tax brackets, along with FICA taxes (Social Security and Medicare), Alex would face a federal income tax of $25,160.00, a California state income tax of $9,967.50, and FICA taxes totaling $11,475.00. This results in a combined tax burden of $46,602.50, leaving Alex with an after-tax income of $103,397.50 for the year. This scenario does not trigger Alternative Minimum Tax (AMT), Net Investment Income Tax (NIIT), or Section 199A (QBI) deduction phase-outs, keeping the focus on standard income and payroll taxes.

However, by strategically making the most of their workplace retirement plan, Alex can significantly reduce this tax liability. If Alex contributes the maximum estimated $24,500 to a traditional 401(k) in 2026, their Adjusted Gross Income (AGI) is lowered, directly impacting their taxable income. This contribution reduces Alex’s federal income tax to $19,280.00 and their California state income tax to $7,689.00, while FICA taxes remain $11,475.00 (as 401(k) contributions do not reduce FICA). The total tax burden drops to $38,444.00, representing a substantial tax savings of $8,158.50 for the year. While Alex’s immediate take-home pay is reduced by the 401(k) contribution, the effective out-of-pocket cost for contributing $24,500 to their retirement account is only $16,341.50 ($24,500 contribution minus $8,158.50 in tax savings), demonstrating the powerful tax efficiency of pre-tax retirement savings.

Consider Roth Options for Tax-Free Growth

Roth contributions are made with after-tax dollars. This means your withdrawals in retirement are tax-free. This can be a significant advantage if you expect to be in a higher tax bracket later. For 2026, Roth IRA income phase-out limits apply. For single filers, the phase-out range is $153,000 to $168,000. For married individuals filing jointly, it’s $242,000 to $252,000. Furthermore, a new rule for 2026 mandates Roth treatment for high-earner catch-up contributions. If your FICA wages exceeded $150,000 (indexed for inflation) in the prior year and you are aged 50 or over, your catch-up contributions must be Roth. This is an important change to note.

Tip 3: Leverage Employer Contributions

Don’t Miss Out on Matching Contributions

Many employers offer matching contributions to your retirement plan. This is essentially free money for your retirement. You should always contribute at least enough to get the full employer match. Otherwise, you are leaving money on the table. Be sure to understand your plan’s vesting schedule. This schedule dictates when employer contributions become fully yours.

Be Aware of Overall Contribution Limits

There’s a total limit on contributions from both you and your employer. For 2026, this combined limit for 401(k)s, 403(b)s, and most 457 plans is $72,000. This limit can be higher if you make catch-up contributions. For example, with the standard age 50+ catch-up, the limit can reach $80,000. SEP IRA limits are $72,000 or 25% of your compensation, whichever is less. Therefore, monitor these limits to ensure compliance.

Tip 4: Understanding SECURE 2.0 Act Changes for 2026

Mandatory Roth Catch-Up for High Earners

The SECURE 2.0 Act brings significant changes for 2026. As mentioned, individuals aged 50 or older with prior-year FICA wages over $150,000 (indexed for inflation) must make their catch-up contributions as Roth. This applies to 401(k), 403(b), and governmental 457(b) plans. If your plan does not offer a Roth option, you might be unable to make catch-up contributions. Check with your plan administrator for details.

Long-Term, Part-Time (LTPT) Worker Eligibility

The SECURE 2.0 Act also expanded eligibility for long-term, part-time workers. The service requirement for eligibility to make elective deferrals in 401(k)s and 403(b)s has been reduced from three years to two years. This change allows more part-time employees to save for retirement through their workplace plans. This is a positive development for many individuals.

Paper Statement Requirements

New requirements for plan statements are also in effect. Defined contribution plans must provide at least one paper statement annually. Defined benefit plans must provide one every three years. However, participants can still elect to receive electronic statements. This ensures better access to plan information for all participants.

Tip 5: Review Your Plan and Seek Guidance

Regularly Review Your Investment Choices

Your retirement plan is not a “set it and forget it” account. Regularly review your investment choices. Ensure your asset allocation aligns with your risk tolerance and financial goals. Market conditions and personal circumstances change. Therefore, periodic review is essential.

Understand Your Plan’s Specifics

Every workplace plan has unique rules. Check your plan documents for specific investment options, withdrawal policies, and other important details. Knowing these specifics helps you make informed decisions. You can often find this information through your employer’s HR department or the plan administrator’s website.

Consider Professional Advice

Retirement planning can be complex. Consulting a financial advisor or tax professional offers personalized guidance. They can help you optimize your contributions, understand tax implications, and align your plan with your broader financial strategy. The IRS website provides valuable resources, including details on contribution limits. Furthermore, you can find general tax information at IRS.gov.

Conclusion

Proactive planning for your workplace retirement plans in 2026 is vital. By understanding the new limits, leveraging tax advantages, and staying informed about SECURE 2.0 Act changes, you can significantly boost your retirement savings. Take action today to maximize your financial future and reduce your tax burden. Download our actionable checklist to get started.