For years, High-Net-Worth Individuals (HNWIs) faced a looming deadline. They strategized around the anticipated sunset of federal estate tax exemptions. Now, with the “One Big Beautiful Bill Act” (OBBBA) permanently establishing a $15 million individual federal estate tax exemption for 2026, the situation has changed significantly. This isn’t just a reprieve; it’s an opportunity to build more robust, long-term wealth transfer strategies. But permanence does not mean simplicity. Understanding how to effectively utilize this new exemption, address state-level taxes, and implement sophisticated planning tools is more important than ever.

Executive Summary

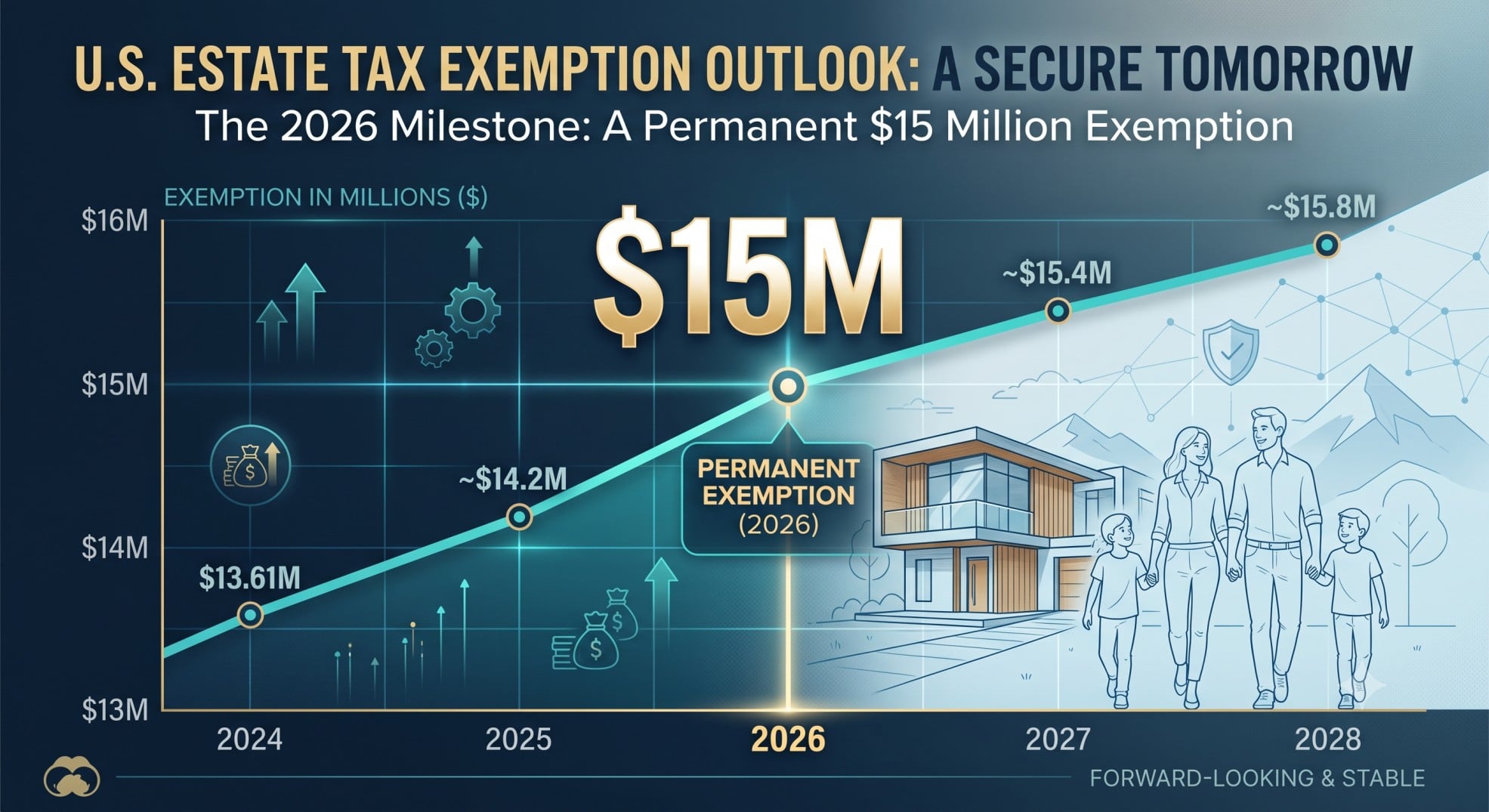

- The “One Big Beautiful Bill Act” (OBBBA) permanently sets the individual federal estate and gift tax exemption at $15 million for 2026.

- Married couples can transfer up to $30 million federally tax-free through portability.

- The federal estate tax rate remains 40% for amounts exceeding the exemption.

- The annual gift tax exclusion for 2026 is $19,000 per recipient.

- This permanence shifts focus from urgent “sunset planning” to long-term, strategic wealth transfer.

- Advanced trusts like GRATs, ILITs, SLATs, and Dynasty Trusts are still important tools.

- State-level estate and inheritance taxes still present significant planning challenges.

- Comprehensive planning combines income tax efficiency, charitable giving, and regular reviews.

- Consulting with qualified tax attorneys, CPAs, and financial advisors is essential for tailored strategies.

The New Situation: Permanent Federal Estate Tax Exemption for 2026

Understanding the “One Big Beautiful Bill Act” (OBBBA)

The “One Big Beautiful Bill Act” (OBBBA) significantly changed estate planning for HNWIs. This legislation was enacted on July 4, 2025. It made permanent the federal estate, gift, and Generation-Skipping Transfer (GST) tax exemptions. Specifically, it set the individual exemption at $15 million for 2026. This means the previous uncertainty about sunsetting provisions is gone. Furthermore, these exemption levels will be adjusted annually for inflation starting in 2027.

Federal Estate and Gift Tax Exemption Levels for 2026

For 2026, the individual Federal Estate Tax Exemption is $15 million. This amount is unified with the gift tax exemption. Therefore, individuals can transfer $15 million during their lifetime or at death without federal estate or gift tax. Married couples, utilizing portability, can effectively shield up to $30 million from federal estate and gift taxes. However, any portion of an estate exceeding these exemption amounts faces a federal estate tax rate of 40%.

Annual Gift Tax Exclusion for 2026

The annual gift tax exclusion for 2026 is $19,000 per recipient. This allows individuals to give away $19,000 to as many people as they wish each year without using any of their lifetime exemption. Married couples can combine their exclusions, permitting them to give $38,000 per recipient through gift-splitting. This strategy requires filing a gift tax return (Form 709) with the IRS.

Generation-Skipping Transfer (GST) Tax Exemption

The Generation-Skipping Transfer (GST) Tax exemption for 2026 aligns with the federal estate tax exemption. It is also $15 million per individual. This tax applies to transfers made to “skip persons,” typically individuals two or more generations younger than the transferor. Unlike the estate tax exemption, the GST exemption is not portable between spouses. Therefore, careful planning is necessary to fully utilize each spouse’s GST exemption.

Strategic Wealth Transfer: Using the Permanent Exemption

Re-evaluating Existing Estate Plans

The permanent higher exemption levels change the focus for HNWIs. The previous urgency of “sunset planning” has moved to a more deliberate, long-term strategy. Many individuals implemented aggressive gifting strategies in prior years. These plans often aimed to use exemptions before they were expected to decrease. Now, reviewing these strategies is crucial. Some complex structures may no longer be necessary or even beneficial.

Lifetime Gifting Strategies

Lifetime gifting is still a powerful tool for wealth transfer. It allows HNWIs to remove future appreciation from their taxable estate. This effectively “locks in” today’s asset values for tax purposes. Utilizing the annual gift tax exclusion is a simple yet effective method for tax-free wealth transfer over time. Furthermore, strategic use of the lifetime gift tax exemption can significantly reduce a future taxable estate. This is particularly true for assets expected to grow substantially.

Advanced Trust Structures for HNWIs

Trusts are still key to advanced estate planning. They offer control, asset protection, and tax efficiency.

- Grantor Retained Annuity Trusts (GRATs): These trusts transfer appreciating assets to beneficiaries with minimal gift tax. The grantor retains an annuity interest for a term. Any appreciation above the IRS-determined interest rate passes to beneficiaries tax-free.

- Irrevocable Life Insurance Trusts (ILITs): ILITs are important for removing life insurance proceeds from the taxable estate. This ensures the death benefit passes to heirs free of estate tax.

- Spousal Lifetime Access Trusts (SLATs): SLATs remove assets from the grantor’s estate while providing for a spouse. This can offer indirect access to funds for the grantor.

- Dynasty Trusts: The increased GST exemption makes Dynasty Trusts more appealing. They facilitate multi-generational wealth transfer, allowing tax-free growth across many generations.

- Family Limited Partnerships (FLPs): FLPs are still relevant for valuation discounts and controlled wealth transfer. They allow HNWIs to retain control while passing ownership interests to family members.

The Importance of Portability for Married Couples

Portability allows a surviving spouse to use any unused portion of their deceased spouse’s federal estate tax exemption. This is important for maximizing the combined $30 million exemption for married couples. However, portability is not automatic. It requires a timely filed Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return, for the deceased spouse’s estate. This election ensures the surviving spouse can fully utilize both exemptions. You can find more information on Form 706 on the IRS website.

Beyond Federal: Addressing State-Level Estate and Inheritance Taxes

Understanding State-Specific Rules

While federal exemptions are high, state-level taxes remain a major concern. Several states impose their own estate taxes. Other states levy inheritance taxes. These state taxes often have much lower exemption thresholds than the federal government. For example, some states may tax estates starting at $1 million or less. Therefore, a comprehensive estate plan must account for these state-specific rules.

Planning for State Tax Liabilities

Planning for state tax liabilities involves several considerations. Domicile, or where an individual legally resides, is a key factor. It determines which state’s tax laws apply. Strategies to mitigate state-level taxes may include relocating to a state without estate or inheritance taxes. Furthermore, certain trust structures or gifting strategies can sometimes reduce state tax exposure. A thorough review of state laws is essential for HNWIs.

Comprehensive Estate Planning: Integrating Financial and Tax Goals

Income Tax Efficiency Considerations

With federal estate tax concerns reduced for many, income tax optimization becomes a main planning focus. HNWIs must focus on capital gains, Net Investment Income Tax (NIIT), and trust income tax rates. Balancing estate tax savings with income tax implications is crucial. For instance, assets with a low-cost basis might be better held until death to receive a step-up in basis. This can reduce capital gains for heirs.

Charitable Giving Strategies

Integrating philanthropy into wealth transfer plans offers important benefits. Donor-Advised Funds (DAFs) provide flexibility and immediate tax deductions. Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) allow HNWIs to support causes while retaining income or passing assets to heirs. These strategies can reduce both income and estate taxes. They also fulfill philanthropic goals.

Reviewing Beneficiary Designations

Regularly reviewing beneficiary designations is very important. These designations for retirement accounts and life insurance policies often supersede a will. Therefore, they must align with the overall estate plan. Incorrect or outdated designations can lead to unintended consequences. They can also create tax inefficiencies or disputes among heirs. This simple step ensures your wishes are honored.

Real-World Scenario: A HNWI Couple’s 2026 Estate Plan

For a High-Net-Worth Individual (HNWI) couple residing in California with a combined estate valued at $30,000,000, addressing estate tax planning in 2026 is significantly simplified by the “One Big Beautiful Bill Act” (OBBBA). This legislation permanently established the individual federal estate tax exemption at $15,000,000 for 2026. For a married couple, utilizing portability, their combined federal exemption would be $30,000,000.

In this scenario, with a combined estate of $30,000,000 and a combined federal exemption of $30,000,000, the couple’s entire estate falls within the federal exemption limits. This means there is no federal estate tax liability for their $30,000,000 estate. It is important to note that California does not impose a state estate or inheritance tax, thus no additional state-level estate tax is incurred.

This scenario highlights the significant impact of the OBBBA’s permanent exemption levels. For many HNWIs, the immediate concern of federal estate tax liability is significantly reduced or eliminated. However, it underscores the continued importance of strategic wealth transfer planning, even when direct federal estate tax is not an issue. Strategies such as lifetime gifting, establishing irrevocable trusts (e.g., Grantor Retained Annuity Trusts or Irrevocable Life Insurance Trusts), or charitable giving can still be crucial for removing future appreciation from the estate, protecting assets, ensuring multi-generational wealth transfer, and achieving philanthropic goals. While other taxes like Alternative Minimum Tax (AMT), Net Investment Income Tax (NIIT), and Section 199A (QBI) deductions are crucial for overall financial planning, they are primarily income-related and do not directly factor into the calculation of federal estate tax on the transfer of assets at death.

Critical Considerations and Next Steps for HNWIs

The Need for Flexibility and Regular Review

Despite the permanence of the new exemptions, flexibility is still key in estate planning. Future legislative changes are always possible. Furthermore, family circumstances, such as births, deaths, marriages, or divorces, evolve over time. Therefore, regular reviews of your estate plan are essential. This ensures it continues to meet your goals and adapts to new realities.

The Role of Professional Advisors

Effective estate planning requires a collaborative approach. HNWIs should work closely with a team of professional advisors. This team includes tax attorneys, Certified Public Accountants (CPAs), and financial advisors. These experts can tailor strategies to individual circumstances. They also ensure compliance with complex tax laws. Their guidance is invaluable for securing your legacy.

Conclusion: Securing Your Legacy in a Stable Tax Environment

The “One Big Beautiful Bill Act” has brought a new period of stability for estate tax planning in 2026. The permanent $15 million individual federal estate tax exemption offers HNWIs unprecedented clarity. It also provides a significant opportunity for strategic wealth transfer. While federal estate tax concerns are reduced for many, the need for sophisticated planning remains. State taxes, income tax efficiency, and multi-generational wealth transfer strategies demand careful attention. Therefore, proactive and comprehensive planning, guided by experienced professionals, is essential. This approach will secure your legacy for generations to come.

Disclaimer: This information is for educational purposes only and does not constitute legal, tax, or financial advice. Tax laws are complex and subject to change. Individual situations vary significantly. High-net-worth individuals should consult with qualified tax attorneys, CPAs, and financial advisors to discuss their specific circumstances and develop personalized estate planning strategies. For more detailed guidance, refer to official sources like the IRS website or consult with a reputable tax professional.