Executive Summary

- Maximize Qualified Plans: Use increased 401(k) limits ($23,000) and the overall defined contribution limit ($69,000) for 2025.

- Note Roth Shift: High-income earners (wages over $160,000) must make 2025 catch-up contributions ($7,500) to qualified plans on a Roth basis.

- Use Backdoor Roths: Bypass income limits for Roth IRAs using traditional non-deductible contributions and conversions.

- Explore NQDC Plans: Defer significant income beyond qualified plan limits, but ensure strict compliance with IRC Section 409A.

- Consider Defined Benefit Plans: Business owners can achieve substantial tax deductions and higher contribution limits ($275,000 maximum annual benefit).

- Strategize RMDs and Roth Conversions: Manage Required Minimum Distributions (RMDs) starting at age 73 and convert pre-tax funds strategically for future tax-free growth.

- Seek Professional Advice: Tax laws are complex and change; always seek personalized advice.

Advanced workplace retirement strategies for high-net-worth individuals in 2025 often require careful planning. As a high-net-worth individual, you understand that standard retirement planning often misses significant tax benefits. For 2025, new IRS limits and changing regulations require careful planning. Are you using every available strategy to protect your wealth and accelerate your retirement savings? Discover five advanced, compliant tactics that can improve your 2025 tax situation and secure your financial future.

This information is for educational purposes only and does not constitute financial, tax, or legal advice. Always consult with a qualified tax advisor, financial planner, or attorney regarding your specific financial situation. Tax laws and regulations are complex and subject to change. The information provided is accurate as of the date of publication but may be superseded by future legislative or regulatory actions.

Why 2025 Demands Advanced Retirement Planning for HNWIs

The Changing Tax Environment: Inflation Adjustments and SECURE Act 2.0

The financial world constantly shifts. Each year, the IRS adjusts various retirement plan limits for inflation. Furthermore, recent legislation, such as the SECURE Act 2.0, continues to reshape how individuals save for retirement. These changes create both challenges and opportunities for those with substantial assets.

The HNWI Challenge: Maximizing Savings Beyond Standard Limits

Standard 401(k) limits often fall short for high-net-worth individuals. These limits rarely meet their tax deferral and wealth accumulation goals. Therefore, HNWIs must look beyond basic savings to optimize their financial future.

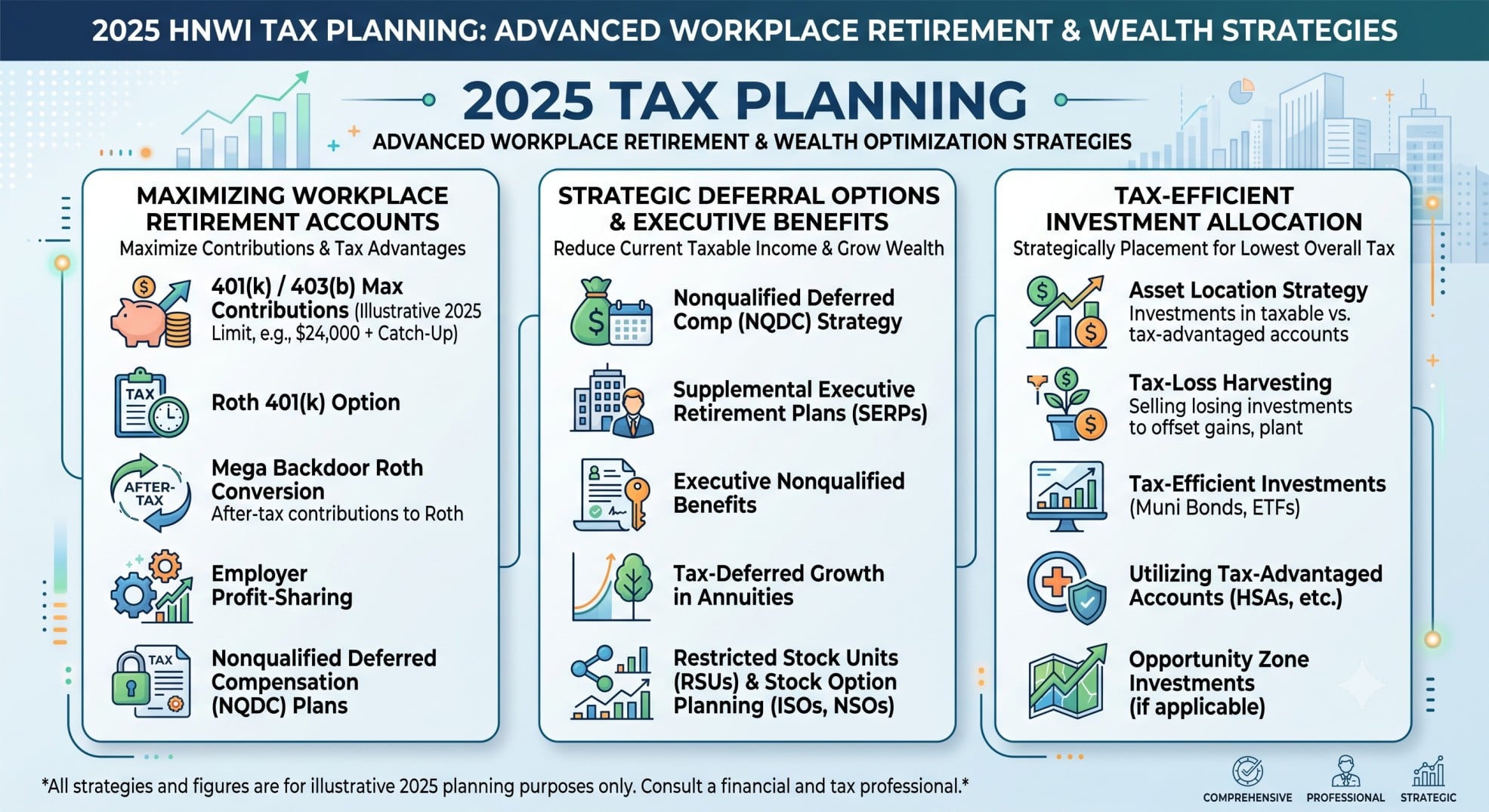

Tip 1: Maximize Qualified Plan Contributions (and Understand the Roth Shift)

Using Increased 401(k), 403(b), and 457(b) Limits

For 2025, the elective deferral limit for employee contributions to 401(k), 403(b), and 457(b) plans increased to $23,000. This is up from $22,500 in 2024. Additionally, the overall defined contribution limit (under IRC Section 415(c)) reached $69,000 for 2025, an increase from $66,000 in 2024. HNWIs should coordinate both employee and employer contributions to reach this maximum. This strategy helps maximize current tax savings.

Understanding 2025 Catch-Up Contributions for Age 50+

Individuals aged 50 and over can make additional catch-up contributions. For 2025, this limit remains $7,500 for 401(k), 403(b), and 457(b) plans. However, a critical change from the SECURE Act 2.0 takes effect in 2025. For participants whose prior year’s wages exceeded $160,000 (indexed for 2025), these catch-up contributions must be made on a Roth (after-tax) basis. This mandatory Roth catch-up has significant implications for high-income earners. It shifts a portion of their tax-deferred savings to tax-free growth in retirement.

Tip 2: Using Backdoor and Mega Backdoor Roth IRAs Strategically

The Backdoor Roth Strategy for HNWIs

Many HNWIs are phased out of direct Roth IRA contributions due to income limits. The Backdoor Roth strategy offers a solution. Individuals contribute to a Traditional IRA on a non-deductible basis. Then, they convert these funds to a Roth IRA. For 2025, the IRA contribution limit is $7,000, up from $6,500 in 2024. The IRA catch-up limit for individuals aged 50 and over remains $1,000. Roth IRA Modified Adjusted Gross Income (MAGI) phase-outs for 2025 are: Single filers: $146,000-$161,000; Married Filing Jointly: $230,000-$240,000. It is important to understand the “pro-rata rule” and ensure no other pre-tax IRA balances exist to execute this strategy effectively.

The Mega Backdoor Roth

The Mega Backdoor Roth strategy allows for even larger Roth contributions. This involves making after-tax contributions to a 401(k) plan, if the plan permits. Subsequently, these after-tax funds are converted to a Roth 401(k) or a Roth IRA. This strategy uses the overall defined contribution limit of $69,000 for 2025. It provides a powerful way to move substantial amounts into a Roth vehicle for tax-free growth.

Tip 3: Using Non-Qualified Deferred Compensation (NQDC) Plans

Beyond Qualified Plan Limits: NQDC Benefits

For executives and highly compensated employees, Non-Qualified Deferred Compensation (NQDC) plans are very useful. These plans allow individuals to defer income and associated taxes beyond the limits of qualified plans. NQDC plans offer significant benefits, including substantial tax deferral, potential for greater savings, and flexibility in distribution timing. This makes them a key part of advanced tax planning for HNWIs.

Strict Compliance with IRC Section 409A

NQDC plans are subject to strict rules under IRC Section 409A. Failure to comply can result in immediate taxation and penalties. Therefore, careful attention to election timing, payment events, and plan administration is essential. The IRS maintains ongoing scrutiny in this complex area, requiring meticulous adherence to regulations.

Tip 4: Considering Defined Benefit and Cash Balance Plans

Boosting Retirement Savings for Business Owners and Executives

Defined Benefit and Cash Balance plans offer unique advantages. These plans allow for significantly higher tax-deductible contributions compared to defined contribution plans. For 2025, the maximum annual benefit under a defined benefit plan (IRC 415(b)) increased to $275,000, up from $265,000 in 2024. These plans are particularly suitable for HNWIs with stable, high incomes and a strong desire for substantial tax deductions.

Understanding the Complexities and Benefits

While powerful, these plans involve actuarial requirements and administrative costs. However, the powerful tax advantages often outweigh these complexities. They provide a robust mechanism for accelerating tax deductions and building significant retirement wealth.

Tip 5: Planning for RMDs and Roth Conversions

Managing Required Minimum Distributions (RMDs) in 2025

The age for beginning Required Minimum Distributions (RMDs) remains 73 for 2025, as established by the SECURE Act 2.0. HNWIs should plan for these distributions carefully. Strategies like Qualified Charitable Distributions (QCDs) can be beneficial for individuals aged 70½ and older. QCDs allow direct transfers from an IRA to a qualified charity, satisfying RMDs while avoiding taxable income.

Proactive Roth Conversions for Future Tax-Free Growth

Consider proactive Roth conversions. Converting pre-tax retirement funds to Roth accounts in lower-income years can be highly advantageous. This strategy reduces future RMDs and provides tax-free growth. Furthermore, original Roth IRA owners are not subject to RMDs, offering greater flexibility and control over their retirement assets.

Real-World Impact: A 2025 HNWI Scenario

For a High-Net-Worth Individual (HNWI) couple filing jointly in California in 2025, with a combined income of $1,200,000 in wages and $220,000 in investment income (long-term capital gains, qualified dividends, and interest), their baseline tax liability without advanced retirement strategies is substantial. Assuming 2025 tax parameters align with 2024 projections, their Adjusted Gross Income (AGI) would be $1,420,000. This results in an estimated Federal Income Tax of $399,321.50, a Net Investment Income Tax (NIIT) of $8,360.00, and a California State Income Tax of $154,781.24. Their total estimated tax burden for the year would be $562,462.74. For this income level, the Section 199A (QBI) deduction is fully phased out, and Alternative Minimum Tax (AMT) is not triggered as an additional tax due to the high regular tax liability and absence of specific AMT preference items. By implementing advanced workplace retirement strategies, this HNWI couple can significantly reduce their tax liability. Contributing the maximum allowable to a pre-tax 401(k) ($23,000) and deferring an additional $100,000 through a Non-Qualified Deferred Compensation (NQDC) plan reduces their AGI to $1,297,000. This strategic deferral leads to a lower Federal Income Tax of $353,811.50 and a California State Income Tax of $137,192.24, while the NIIT remains $8,360.00. The total estimated tax burden with these strategies drops to $499,363.74, resulting in a substantial tax savings of $63,099.00 for the year 2025.

Key Points for Your 2025 Retirement Strategy

The 2025 tax year offers significant opportunities for HNWIs. Maximizing qualified plan contributions, understanding the Roth shift, and strategically using Backdoor and Mega Backdoor Roth IRAs are essential. Furthermore, using NQDC plans and considering Defined Benefit plans can dramatically impact your tax picture. Finally, proactive RMD planning and Roth conversions ensure long-term tax efficiency. Proactive planning and professional guidance are essential for success.

Download Your Practical 2025 Retirement Planning Checklist

To help you implement these strategies, we encourage you to download our comprehensive 2025 Retirement Planning Checklist. This resource will guide you through the steps necessary to improve your retirement savings.

Strategic planning is not merely about saving; it is about improving your financial future. For high-net-worth individuals, understanding and implementing advanced workplace retirement strategies for 2025 is essential. Consult a tax professional to adapt these strategies to your unique situation. This ensures compliance and helps grow your wealth.