Last updated: May 16, 2026

If you are trying to understand taxable income vs gross income, here is the simple answer: gross income is your starting income number, while taxable income is the amount the IRS actually uses to calculate your federal income tax.

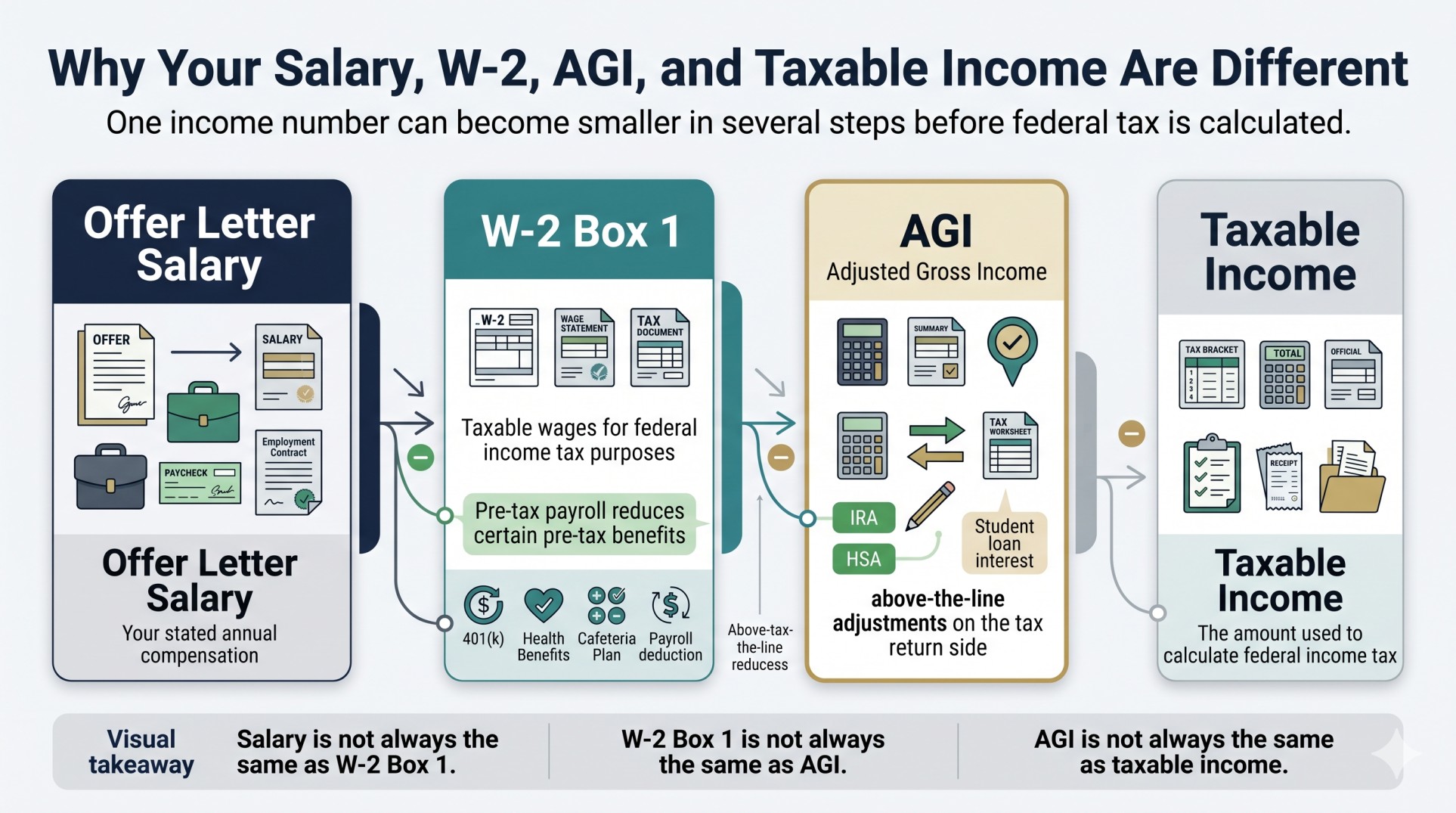

That difference matters more than most people realize. Your salary on an offer letter, your gross pay on a pay stub, your W-2 Box 1 amount, your adjusted gross income (AGI), and your taxable income are not always the same number.

This guide explains how the process works, where people get confused, and how deductions can lower the amount of income that is actually taxed.

Editorial note: This article discusses federal income tax concepts for educational purposes. State tax rules can differ.

Quick Answer

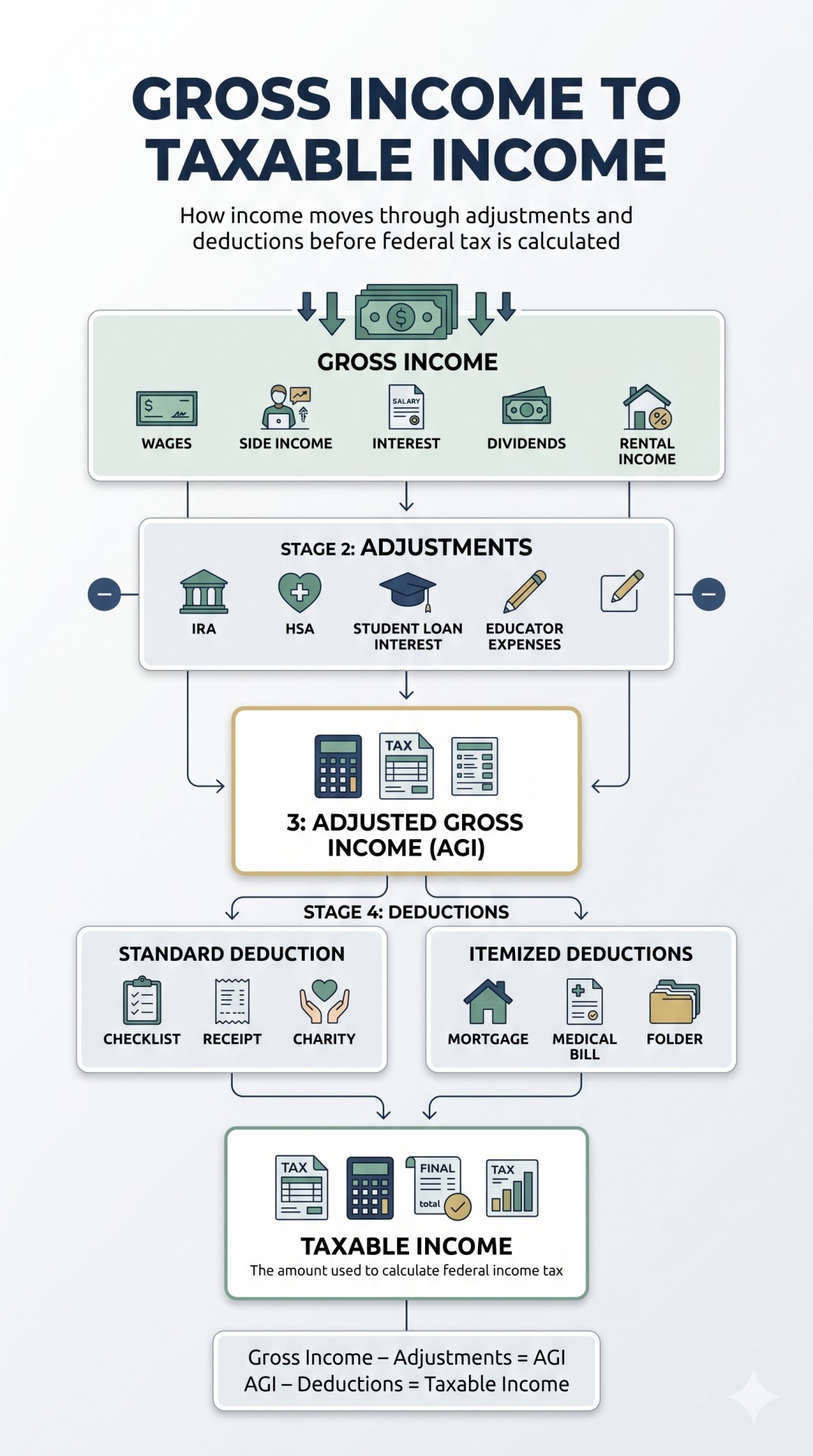

Gross income is generally your income before you subtract adjustments, the standard deduction (standard deduction 2026 ), or itemized deductions.

Taxable income is the smaller amount left after those allowed reductions are applied.

In other words:

Total income – adjustments = AGI

AGI – standard deduction or itemized deductions = taxable income

Taxable Income vs Gross Income at a Glance

| Feature | Gross Income | Taxable Income |

|---|---|---|

| Definition | Your starting income before later tax deductions are applied. | The amount of income the IRS uses to calculate your federal income tax. |

| Size | Usually the bigger number. | Usually the smaller number. |

| What it includes | Wages, tips, side hustle income, interest, dividends, rental income, and other taxable income. | AGI after subtracting the standard deduction or itemized deductions. |

| Where people look for it | Offer letters, pay stubs, year-end income records, and the total-income section of Form 1040. | Form 1040, line 15. |

| Why it matters | Useful for understanding earnings and cash flow. | Used to determine your federal income tax brackets and tax bill. |

What Is Gross Income?

Gross income is the starting point in the tax calculation. Broadly speaking, it includes income you receive in the form of money, property, goods, or services that is not excluded from tax.

Examples of gross income can include:

- Salary and hourly wages

- Tips and bonuses

- Freelance or 1099 income

- Side hustle income

- Interest and dividends

- Rental income

- Certain retirement distributions

So if you earn $75,000 from your job and another $5,000 from freelance work, your starting income for tax purposes may be $80,000 before later deductions are applied.

Important: if you are an employee, your W-2 Box 1 is usually not the same as your full gross pay. Box 1 generally reflects taxable wages for federal income tax, which may already be reduced by certain pre-tax contributions or benefits.

Where AGI Fits In

Before you reach taxable income, you typically pass through one middle step: adjusted gross income (AGI).

AGI is important because many tax rules, credits, and deductions are based on it. It also appears directly on Form 1040.

Common items that may reduce AGI include:

- Deductible traditional IRA contributions

- HSA contributions you make directly

- Student loan interest

- Certain educator expenses

- Certain self-employed deductions

One common point of confusion is payroll deductions. A traditional 401(k) contribution often reduces taxable wages before the amount appears in W-2 Box 1. By contrast, some other deductions are claimed directly on the tax return and reduce AGI there.

Simple formula:

Total income – adjustments = AGI

For a deeper explanation, see our guide on adjusted gross income vs taxable income.

What Is Taxable Income?

Taxable income is the amount left after you subtract either:

- the standard deduction, or

- your itemized deductions.

You do not take both. You generally use whichever gives you the larger deduction.

Formula:

AGI – standard deduction or itemized deductions = taxable income

Once you have your taxable income, that is the number used to apply the federal tax brackets.

Step-by-Step Example: From Income to Taxable Income

Here is a simple example using tax year 2026 numbers.

Meet David. David is a single filer for tax year 2026.

- Total income: David earns $80,000.

- Adjustments: David qualifies for a $5,000 deductible traditional IRA contribution and a $1,000 HSA deduction.

- AGI: $80,000 – $6,000 = $74,000.

- Standard deduction: David claims the 2026 single standard deduction of $16,100.

- Taxable income: $74,000 – $16,100 = $57,900.

Even though David started with $80,000 of income, his federal income tax is based on $57,900 of taxable income, not the full $80,000.

That is why understanding the difference between taxable income vs gross income matters so much for tax planning.

Important note: Tax results depend on filing status, eligibility rules, and the type of deduction involved. This example is simplified for education.

W-2 Box 1 vs Gross Income: The Most Common Confusion

If your offer letter says $75,000 but your W-2 Box 1 shows a lower number, that does not automatically mean something is wrong.

- Your offer letter usually shows salary or gross compensation.

- Your pay stub may show gross pay for each pay period.

- Your W-2 Box 1 usually shows taxable wages for federal income tax purposes.

That means pre-tax items such as traditional 401(k) contributions and some pre-tax benefits can reduce what appears in Box 1.

If you want a full breakdown, see our related guide on W-2 Box 1 vs Box 3 vs Box 5.

Why Knowing the Difference Matters

Understanding taxable income vs gross income can help you:

- Estimate your tax bill more accurately

- Understand why your W-2 may be lower than your salary

- Make smarter decisions about retirement and HSA contributions

- Use deductions to lower the amount of income that gets taxed

It also helps prevent a common mistake: assuming a tax bracket applies to your entire salary. Federal income taxes are marginal, so higher rates apply only to the income inside those higher brackets.

If you want to lower your bill, read how to reduce taxable income legally.

Gross Income vs Taxable Income vs Net Pay

These three terms are related, but they are not interchangeable.

- Gross income: your starting income before later tax deductions are applied.

- Taxable income: the amount the IRS actually taxes for federal income tax purposes.

- Net pay: your take-home pay after taxes, benefits, and other payroll withholdings.

That is why your take-home pay is often much lower than both your gross income and your taxable income.

Frequently Asked Questions

Is W-2 Box 1 my gross income or taxable income?

W-2 Box 1 usually shows your taxable wages for federal income tax purposes, not your full gross pay.

Do tax brackets apply to gross income or taxable income?

Federal income tax brackets apply to taxable income.

Where can I find AGI and taxable income on Form 1040?

AGI is on Form 1040 line 11, and taxable income is on Form 1040 line 15.

What is the difference between AGI and taxable income?

AGI is your income after certain adjustments. Taxable income is what remains after you subtract the standard deduction or itemized deductions from AGI.

Can I lower taxable income legally?

Yes. Depending on your situation, you may lower taxable income with deductible contributions, certain adjustments, and either the standard deduction or itemized deductions.