Most taxpayers don’t need to itemize. Taking the standard deduction for 2026 is the fastest way to reduce your taxable income without tracking every single medical bill or charitable donation.

The IRS adjusts these baseline amounts annually for inflation, meaning the figures have gone up again. And if you’re over 65 or filing as head of household, you qualify for additional bumps that push your write-off even higher.

Knowing exactly how much you can deduct is the first step to a bigger refund. Here is exactly how much you can claim this filing season, and how to apply the new bonus deductions to your return.

⚡ Executive Summary: 2026 Standard Deduction Updates

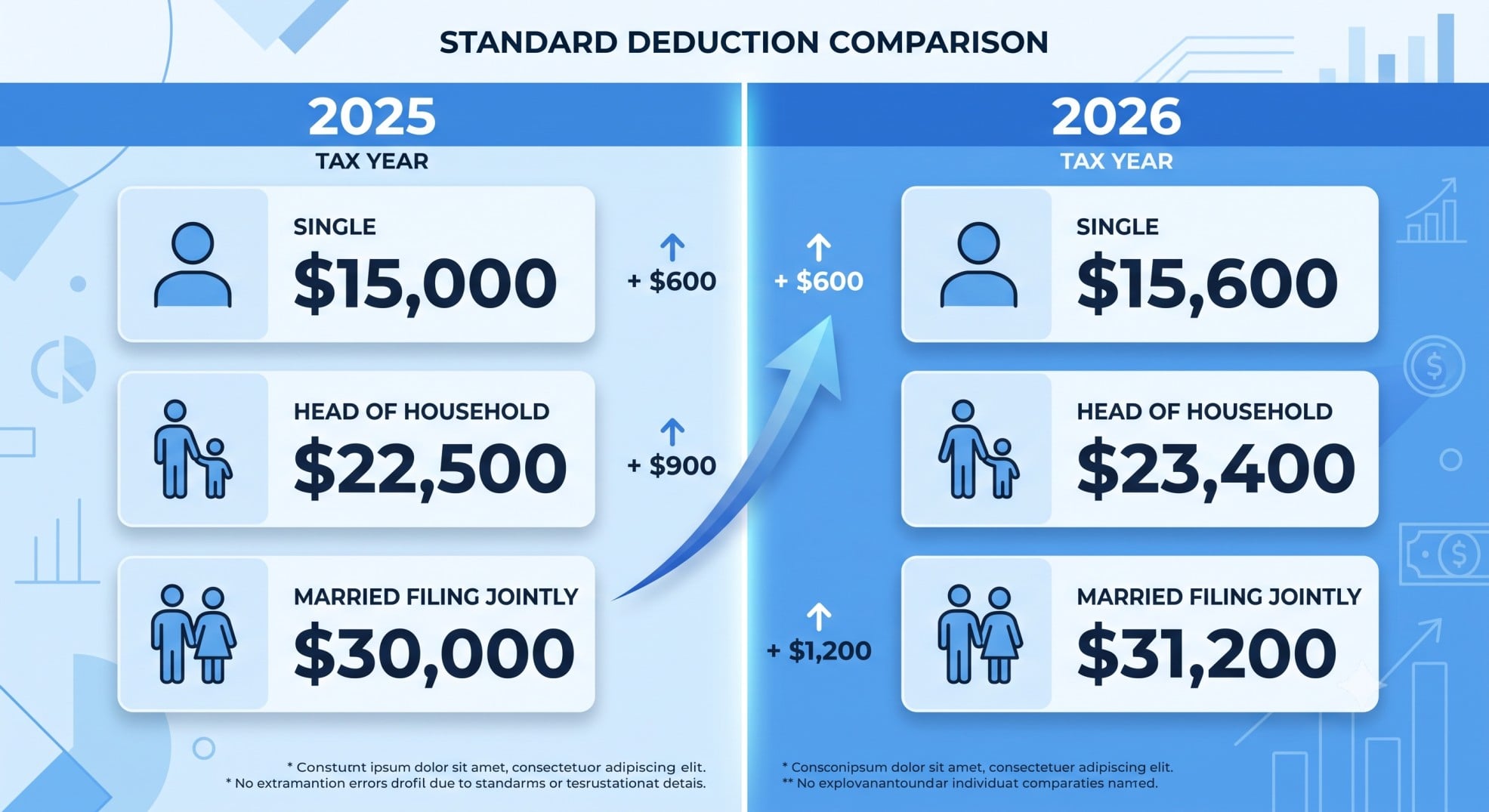

- The standard deduction for 2026 single filers has increased to $16,100.

- Married couples filing jointly can now deduct a baseline of $32,200.

- The official IRS standard deduction for 2026 includes a new $6,000 Senior Bonus Deduction for eligible taxpayers aged 65 and older.

- Non-itemizers can now deduct up to $1,000 (single) or $2,000 (joint) in charitable cash contributions on top of their standard deduction.

Table of Contents

- What is the Standard Deduction for 2026?

- 2026 Standard Deduction Amounts by Filing Status

- The Standard Deduction 2026 Single Filers Guide

- The Standard Deduction 2026 Married Jointly Breakdown

- Additional Standard Deductions for Seniors and the Blind

- The New 2026 Senior Bonus Deduction

- Standard Deduction for Dependents in 2026

- Standard vs. Itemized Deductions in 2026

- How to Claim the Federal Standard Deduction 2026

- Frequently Asked Questions About the 2026 Standard Deduction

What is the Standard Deduction for 2026?

For 2026, the base standard deduction is $16,100 for single filers and $32,200 for married couples filing jointly. This is a specific flat dollar amount that reduces your adjusted gross income (AGI) before the IRS calculates your tax bill.

Think of it as a tax-free zone. If you earn $60,000 a year and take a $16,100 deduction, you’re only taxed on $43,900. You don’t need to prove any expenses or fill out complicated extra schedules to claim it. You just check a box on your Form 1040.

Every fall, the IRS adjusts these figures to keep pace with inflation. This prevents “bracket creep”—a situation where cost-of-living wage increases push you into a higher tax bracket without actually increasing your purchasing power. For the 2026 tax year (which you file in early 2027), the IRS formalized these adjustments in Revenue Procedure 2025-32.

So, your baseline numbers are higher. But 2026 also brings new deduction categories based on recent legislation. Your total write-off could be significantly larger than the baseline numbers suggest. Understanding your tax bracket is only half the math. Stacking your eligible deductions is where the real savings happen.

2026 Standard Deduction Amounts by Filing Status

Your exact deduction depends entirely on how you file. The IRS categorizes taxpayers into five main filing statuses, and each gets a different baseline amount.

| Filing Status | 2025 Amount | 2026 Amount | Increase |

|---|---|---|---|

| Single | $15,750 | $16,100 | +$350 |

| Married Filing Jointly | $31,500 | $32,200 | +$700 |

| Head of Household | $23,625 | $24,150 | +$525 |

| Married Filing Separately | $15,750 | $16,100 | +$350 |

| Qualifying Surviving Spouse | $31,500 | $32,200 | +$700 |

These are just the starting points. Depending on your age, your vision status, and your charitable habits, you might be able to add thousands of dollars on top of these base figures.

The Standard Deduction 2026 Single Filers Guide

Unmarried, divorced, or legally separated taxpayers generally file as single. The standard deduction for 2026 single filers is exactly $16,100.

This represents a $350 increase from the previous tax year. For young professionals, freelancers, and renters who don’t have enough deductible expenses to justify itemizing, this flat rate is incredibly efficient. It instantly wipes out the tax liability on your first $16,100 of earnings.

Understanding the standard deduction for 2026 single amount in practice

Let’s look at how the single standard deduction for 2026 actually impacts a real-world tax return. The math is straightforward, but seeing it applied makes the benefit obvious.

Hypothetical Scenario 1: The Single Freelancer

Maria is a 29-year-old freelance graphic designer living in Texas. In 2026, her net business income (after deducting her software subscriptions and home office expenses on Schedule C) is $65,000.

- Gross Income: $65,000

- Less Single Standard Deduction: -$16,100

- Taxable Income: $48,900

Because Maria takes the standard deduction, she completely shields $16,100 from federal income tax. She will only calculate her income tax based on the remaining $48,900, which keeps her firmly in the 12% marginal tax bracket rather than spilling over into the 22% bracket.

Keep in mind that taking this deduction doesn’t prevent you from claiming business expenses. Freelancers and independent contractors can still write off their business costs on Schedule C to find their adjusted gross income, and then apply the standard deduction on top of that.

The Standard Deduction 2026 Married Jointly Breakdown

Couples who tie the knot get access to the largest baseline write-off in the tax code. The standard deduction for 2026 married jointly amount is $32,200.

This is exactly double the single rate. The IRS designed it this way to eliminate the “marriage penalty” for low-to-middle-income earners. If you’re legally married by the last day of the year, you qualify for this full amount, even if only one spouse actually earned income during the year.

What happens if you’re married but decide to file separately? The IRS allows it, but they strictly enforce a matching rule. If one spouse chooses to itemize their deductions, the other spouse is legally forced to itemize as well. You can’t have one spouse take the $16,100 flat deduction while the other writes off $20,000 in mortgage interest.

Additional Standard Deductions for Seniors and the Blind in 2026

The tax code offers extra relief for older Americans and those with severe vision impairments. If you’re age 65 or older by the end of 2026, or if you’re legally blind, you get to add an “additional standard deduction” to your baseline amount.

For 2026, the additional amounts are:

- $2,050 for Single or Head of Household filers.

- $1,650 for Married filers (per qualifying spouse).

These conditions stack. If you’re single, over 65, and legally blind, you get to add $4,100 ($2,050 x 2) to your base deduction. If you’re married filing jointly and both spouses are over 65, you add $3,300 ($1,650 x 2) to your joint baseline.

And remember, the IRS considers you to be 65 on the day before your 65th birthday. So, if your 65th birthday falls on January 1, 2027, you’re officially considered 65 for the 2026 tax year and can claim the extra money.

The New 2026 Senior Bonus Deduction

Here is where the 2026 standard deduction gets incredibly interesting. Recent legislation introduced a temporary “Senior Bonus Deduction” available from 2025 through 2028. This is entirely separate from the traditional age 65+ additional deduction we just discussed.

Eligible taxpayers aged 65 and older can claim a bonus deduction of $6,000 per person. That means a single senior can deduct an extra $6,000, and a married couple (if both are 65+) can deduct an extra $12,000.

But there’s a catch. This bonus deduction is income-restricted. It begins to phase out at a 6% rate once your Modified Adjusted Gross Income (MAGI) crosses specific thresholds:

- Single Filers: Phaseout begins at $75,000 MAGI.

- Married Filing Jointly: Phaseout begins at $150,000 MAGI.

Hypothetical Scenario 2: The Senior Bonus Stack

David (67) and Sarah (66) are married and filing jointly. They are both retired and have a combined MAGI of $90,000 from pensions and investments. Because their income is well below the $150,000 phaseout limit, they qualify for the full bonus.

- Base Joint Deduction: $32,200

- Age 65+ Additional ($1,650 x 2): $3,300

- Senior Bonus Deduction ($6,000 x 2): $12,000

- Total 2026 Standard Deduction: $47,500

By stacking these provisions, David and Sarah wipe out more than half of their taxable income before applying a single tax bracket rate. Their final taxable income drops to just $42,500.

This new provision is designed to protect middle-income retirees from paying excessive taxes on their Social Security and retirement account withdrawals. Planning your retirement withdrawals around these phaseout limits is now a critical tax strategy.

Standard Deduction for Dependents in 2026

Children and other dependents who work part-time jobs also have to file taxes if they earn enough money. However, the IRS standard deduction for 2026 rules are much stricter for anyone who can be claimed as a dependent on someone else’s return.

A dependent can’t simply claim the full $16,100 single amount. Instead, their deduction is limited to the greater of two calculations:

- A flat $1,350.

- Their earned income for the year plus $450 (not to exceed the regular $16,100 limit).

This rule exists to prevent wealthy parents from shifting unearned investment income (like stock dividends) to their children to avoid taxes. Earned income (money from a W-2 job) gets favorable treatment, while unearned income doesn’t.

Hypothetical Scenario 3: The Working Teenager

Leo is 17 years old and is claimed as a dependent by his parents. During the summer of 2026, he works as a lifeguard and earns $3,000 (earned income). He also receives $500 in stock dividends (unearned income) from an account his grandfather set up.

- Leo’s Total Income: $3,500

- Deduction Calculation: Earned income ($3,000) + $450 = $3,450.

- Leo’s Standard Deduction: $3,450 (since it is greater than $1,350).

- Taxable Income: $3,500 – $3,450 = $50.

Leo will only owe federal income tax on $50. The formula successfully shielded his hard-earned wages while capturing a tiny fraction of his unearned investment income.

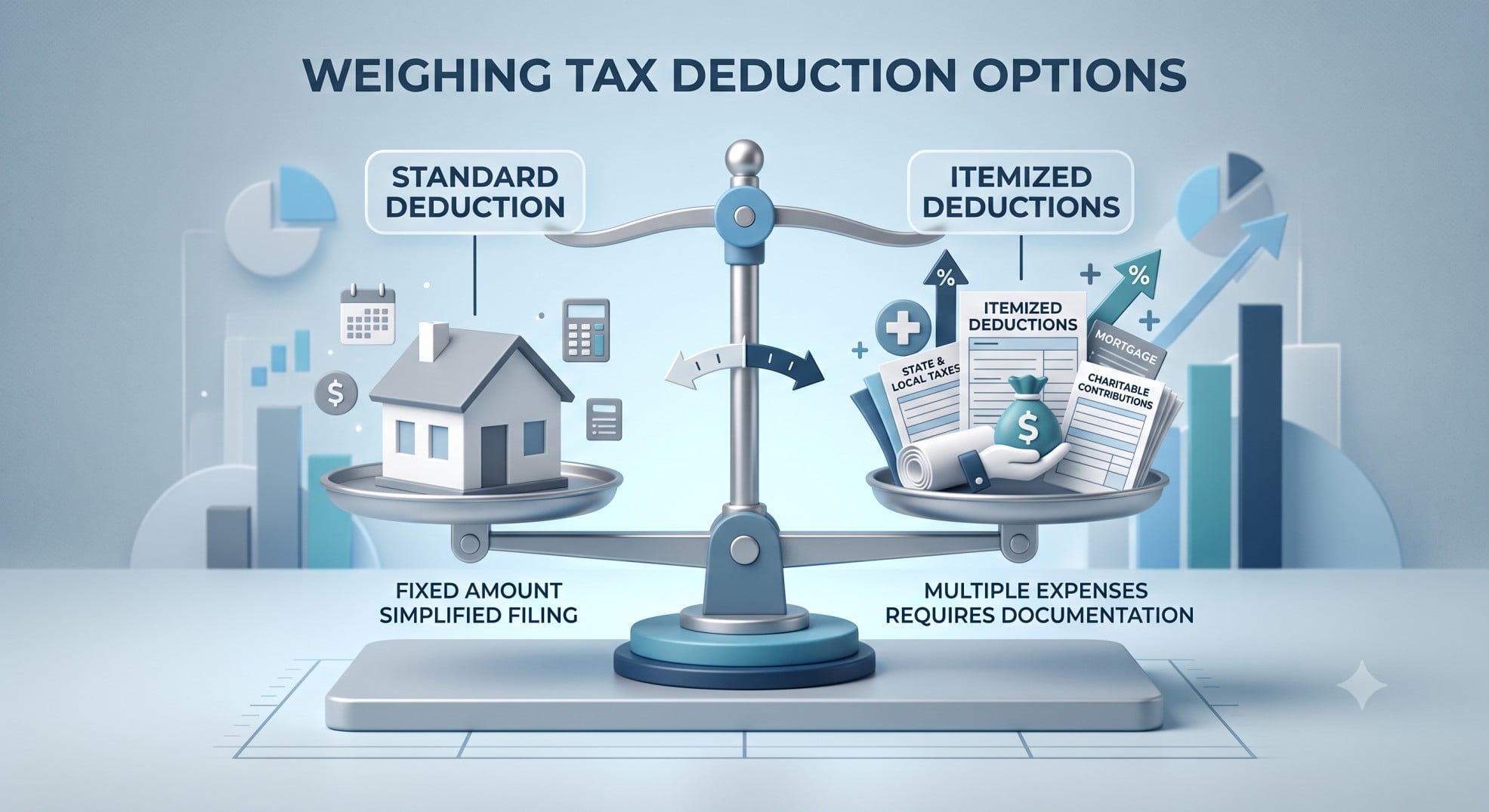

Standard vs. Itemized Deductions in 2026

Taxpayers always face a choice: take the flat 2026 standard deduction or itemize their actual expenses on Schedule A. You’re legally required to choose whichever method results in the lower tax bill, but you can’t do both.

Itemizing only makes sense if your total deductible expenses exceed your standard deduction amount. The most common itemized deductions include:

- Mortgage interest on up to $750,000 of debt.

- State and local taxes (SALT).

- Out-of-pocket medical expenses that exceed 7.5% of your AGI.

- Large charitable contributions.

For 2026, the math on itemizing has shifted dramatically due to changes in the SALT cap. Previously capped at $10,000, the SALT deduction limit has temporarily quadrupled to $40,400 for most filers in 2026. This means taxpayers in high-tax states like California, New York, and New Jersey might suddenly find that itemizing is worth it again.

Hypothetical Scenario 4: The SALT Cap Shift

James and Emily are married filing jointly in New Jersey. They pay $22,000 a year in property taxes and state income taxes. They also pay $12,000 in mortgage interest.

Under the old rules, their SALT deduction was capped at $10,000. Their total itemized deductions would have been $22,000 ($10k SALT + $12k mortgage). Because $22,000 is less than the $32,200 standard deduction, they would have taken the standard route.

Under the 2026 rules, they can deduct their full $22,000 in SALT because the cap is now $40,400. Their new itemized total is $34,000 ($22k SALT + $12k mortgage). Because $34,000 is greater than the $32,200 standard deduction, James and Emily will now choose to itemize, saving them additional money.

Note that the new $40,400 SALT cap phases out for ultra-high earners with a MAGI above $505,000. If your income is below that threshold, running the numbers both ways is highly recommended.

How to Claim the Federal Standard Deduction 2026

Claiming the federal standard deduction for 2026 is the easiest part of filing your taxes. If you use modern tax software, the system will automatically calculate your standard amount and compare it against any itemized deductions you enter. It will default to whichever number saves you the most money.

Filing paper forms? The deduction is claimed directly on the first page of Form 1040 (Line 12). You simply write in the amount that corresponds to your filing status.

There’s one big new benefit for non-itemizers in 2026. Historically, if you took the standard deduction, you couldn’t write off charitable donations. That rule has changed. Starting in 2026, taxpayers who take the standard deduction can also claim a “Universal Charitable Deduction” for cash gifts made to qualified operating charities.

You can deduct up to $1,000 if you’re single, or up to $2,000 if you’re married filing jointly. This amount is subtracted from your income on top of your standard deduction. Just be aware that contributions to Donor-Advised Funds (DAFs) or private foundations don’t qualify for this specific carve-out. You must give cash directly to a registered 501(c)(3) organization and keep the receipt.

Frequently Asked Questions About the 2026 Standard Deduction

What is the standard deduction for 2026?

The baseline standard deduction for 2026 is $16,100 for single filers, $32,200 for married couples filing jointly, and $24,150 for heads of household. These amounts reduce your taxable income before federal tax rates are applied.

How much is the standard deduction for 2026 single?

The standard deduction for 2026 single amount is exactly $16,100. This is a $350 increase from the 2025 tax year, designed to help taxpayers keep up with inflation.

What is the standard deduction for 2026 married jointly?

The standard deduction for 2026 married jointly is $32,200. This amount is available to any couple legally married by December 31, 2026, and it effectively doubles the single filer allowance.

How does the single standard deduction for 2026 work for seniors?

Seniors get the base single standard deduction for 2026 of $16,100, plus an age 65+ additional deduction of $2,050. Eligible seniors may also qualify for a new $6,000 Senior Bonus Deduction, potentially bringing their total write-off to $24,150.

Did the federal standard deduction for 2026 increase from last year?

Yes, the federal standard deduction for 2026 increased across all filing statuses. Single filers saw a $350 bump, while married couples filing jointly received a $700 increase compared to the 2025 tax year.

Where can I find the official IRS standard deduction for 2026 amounts?

The official IRS standard deduction for 2026 amounts were published in Revenue Procedure 2025-32. You can find these figures referenced in the Form 1040 instructions for the 2026 tax year.

Can I claim the 2026 standard deduction and still write off charity?

Yes. Starting in 2026, taxpayers who take the 2026 standard deduction can also claim a universal charitable deduction of up to $1,000 (single) or $2,000 (joint) for cash donations made to qualified charities.

How do I know if I should take the standard deduction or itemize?

You should itemize only if your total deductible expenses (like mortgage interest, state taxes, and large medical bills) add up to more than your standard deduction amount. Tax software will automatically calculate which option saves you more money.

What is the standard deduction for a dependent child in 2026?

For a dependent in 2026, the deduction is limited to the greater of $1,350 or their earned income plus $450. It cannot exceed the regular standard deduction for their filing status.

Can married couples filing separately claim the standard deduction?

Yes, married couples filing separately can claim a $16,100 deduction in 2026. However, if one spouse chooses to itemize their deductions, the IRS strictly requires the other spouse to itemize as well.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.

2 thoughts on “Standard Deduction 2026: Amounts by Filing Status and When to Itemize”