⚡ Executive Summary: Form 8606 Fundamentals

- The 2026 IRA contribution limit is $7,500, or $8,600 if you are age 50 or older.

- High earners who cannot deduct traditional IRA contributions must file Form 8606 to establish their after-tax basis.

- Failing to report these contributions results in double taxation when you eventually withdraw or convert the funds.

- You can submit this form independently if you do not meet the income threshold to file a full tax return.

Table of Contents

- What is Form 8606 and Why Do You Need It?

- Step-by-Step: How to Report Nondeductible IRA Form 8606

- The Pro-Rata Rule and Backdoor Roth Conversions

- How to Track IRA Basis Form 8606 Across Multiple Years

- Can You File Form 8606 Without 1040?

- What is the Penalty for Not Filing Form 8606?

- Real-World Examples: How to Report Nondeductible IRA Form 8606

- Form 8606 Instructions: Common Mistakes to Avoid

- Frequently Asked Questions About Form 8606

What is Form 8606 and Why Do You Need It?

Form 8606 is an IRS tax document used to report nondeductible contributions to a traditional IRA. You need it to track your after-tax basis, preventing the IRS from taxing those funds a second time when you withdraw or convert them.

Taxes rarely forgive mistakes, especially when it comes to retirement accounts. If you are trying to figure out how to report nondeductible ira form 8606 entries, you are likely trying to protect your hard-earned money from being taxed twice.

High earners often face strict income limits that prevent them from taking a tax deduction on their traditional IRA contributions. For 2026, the maximum contribution limit is $7,500, with an additional $1,100 catch-up allowance for those aged 50 and older.

When you make a contribution but cannot claim the deduction, that money becomes “after-tax” money. The IRS refers to this as your tax basis. Filing a nondeductible ira form 8606 is mandatory to prove to the government that you have already paid taxes on those specific dollars.

Without this form, the IRS assumes every penny inside your traditional IRA is pre-tax money. That means when you eventually withdraw the funds in retirement, you will pay ordinary income tax on money you already paid taxes on.

You must file this document if you meet any of the following conditions during the tax year:

- You made nondeductible contributions to a traditional IRA.

- You took distributions from a traditional, SEP, or SIMPLE IRA, and you have a historical basis.

- You converted funds from a traditional, SEP, or SIMPLE IRA to a Roth IRA.

Double taxation is an expensive and entirely avoidable error. Your nondeductible ira form 8606 proves to the IRS exactly how much of your account balance belongs to you free and clear. We see taxpayers lose thousands of dollars simply because they skipped this one-page document during tax season.

Step-by-Step: How to Report Nondeductible IRA Form 8606

To report these contributions, fill out Part I of the form. You will list your current year contributions, add prior year basis, and calculate the nontaxable portion of any distributions or conversions.

Let’s look at the actual mechanics of the paperwork. Understanding how to report nondeductible ira form 8606 data requires breaking the document down into three distinct parts.

Part I handles the core math for your contributions and calculates the taxable portion of any distributions you took during the year. Here is how the primary lines function:

- Line 1: Enter your total nondeductible contributions for the current tax year.

- Line 2: Bring in your historical basis from the previous year (found on Line 14 of your last filed form).

- Line 3: Add Lines 1 and 2 together to find your total after-tax money in the IRA system.

- Line 6: Enter the total value of all your traditional, SEP, and SIMPLE IRAs as of December 31.

- Line 14: This is your remaining basis to carry forward to next year.

Line 6 is where things get complicated for many taxpayers. You must aggregate every non-Roth IRA you own to get this number correct. If you leave out an old SEP IRA, your entire calculation will be wrong.

Part II is strictly for conversions. When you move money to a Roth IRA, this section calculates the final tax bill. Line 16 pulls the total conversion amount, and Line 17 pulls the nontaxable amount calculated in Part I. Line 18 subtracts the nontaxable amount from the total, leaving you with the exact taxable amount of your conversion to report on your Form 1040 tax return.

Part III deals with Roth distributions. Most taxpayers skip this section entirely unless they are pulling money out of a Roth account before reaching age 59½.

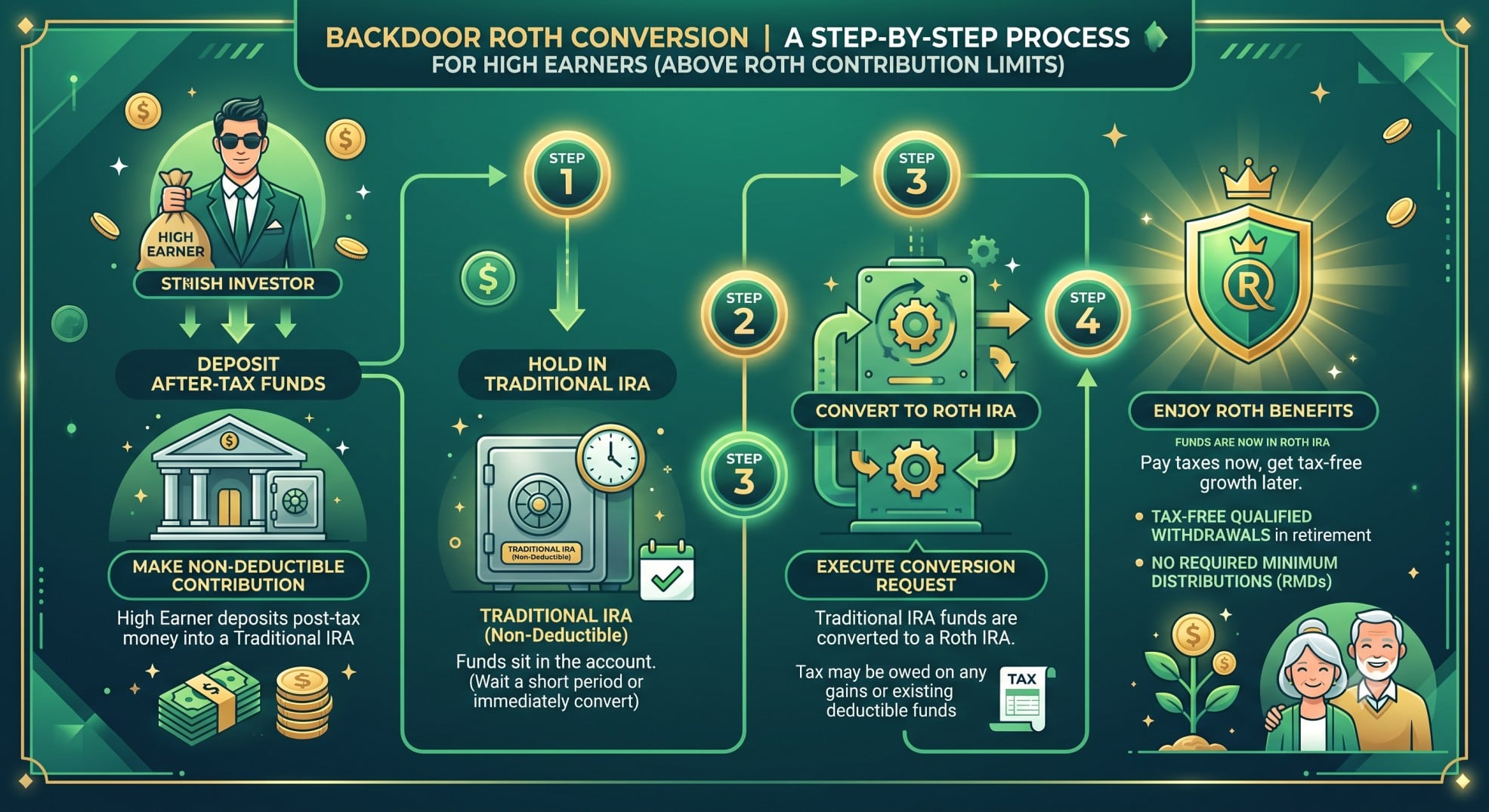

The Pro-Rata Rule and Backdoor Roth Conversions

The Pro-Rata rule dictates that IRA conversions are taxed proportionally based on your ratio of after-tax to pre-tax funds across all non-Roth IRAs. You cannot isolate just the after-tax money for a tax-free conversion.

This rule catches investors off guard every single year. Because the IRS views all your non-Roth IRAs as one giant bucket, you cannot hide pre-tax money in a different account or at a different brokerage firm to avoid this calculation.

If you have $90,000 of pre-tax money in a Rollover IRA and you make a $10,000 nondeductible contribution to a new traditional IRA, your total balance across all accounts is $100,000. Your basis in this scenario is exactly 10%.

If you attempt a Backdoor Roth conversion of that $10,000, the IRS dictates that only 10% ($1,000) is tax-free. The remaining $9,000 of the conversion is fully taxable as ordinary income.

To calculate the Pro-Rata rule correctly, the IRS requires you to aggregate the balances of specific accounts:

- Included in the calculation: Traditional IRAs, Rollover IRAs, SEP IRAs, and SIMPLE IRAs.

- Excluded from the calculation: Roth IRAs, Inherited IRAs, and workplace plans like a 401(k) or 403(b).

To avoid a massive tax bill, some investors roll their pre-tax IRA balances into a workplace 401(k) before December 31. Doing so empties the pre-tax bucket, leaving only the after-tax basis for a clean, tax-free conversion.

How to Track IRA Basis Form 8606 Across Multiple Years

You track your basis by carrying the amount from Line 14 of your current form to Line 2 of next year’s form. Keeping historical tax returns is essential because brokerage firms do not track this for you.

You must track ira basis form 8606 year over year to protect your money. Line 14 is arguably the most critical number on the entire page because it represents your total unrecovered basis carrying forward into the next tax year.

When you file your taxes the following spring, that exact number must be entered on Line 2 of your new form. Failing to track ira basis form 8606 means you will likely pay taxes twice when you finally withdraw the money in retirement.

Without this historical record, the IRS assumes every dollar in your account is pre-tax. Your custodian will not save you here. Form 5498, which your brokerage sends in May, only reports the total amount contributed, not whether you took a tax deduction for it.

If you change tax software or hire a new CPA, you must provide them with your most recent form. A common issue arises when a taxpayer switches accountants and forgets to hand over their prior-year basis information.

The new accountant files the return assuming a basis of zero, effectively wiping out years of after-tax contributions. Always verify that Line 2 on your current return matches Line 14 from your previous return.

Can You File Form 8606 Without 1040?

Yes, you can file this form by itself if your income is below the threshold required to file a standard tax return. Simply complete the form, sign page two, and mail it directly to the IRS.

You can file form 8606 without 1040 if you have no other filing requirement for the year. Retirees living exclusively on non-taxable income, such as certain Social Security benefits or municipal bond interest, often fall into this category.

Sometimes, a younger taxpayer makes a nondeductible contribution using savings but does not earn enough gross income during the year to trigger a mandatory federal tax return.

To file form 8606 without 1040, follow these exact steps:

- Print the form corresponding to the tax year the contribution was made.

- Fill out your name, address, and Social Security number at the top.

- Complete Part I to establish your basis.

- Sign and date the bottom of page two (mandatory for standalone filings).

- Mail it to the IRS processing center listed for your state.

Many people use this exact method to correct past mistakes. If you forgot to report a nondeductible contribution three years ago, you do not necessarily need to amend your entire tax return. You can just mail the standalone form for that specific tax year to establish your basis.

What is the Penalty for Not Filing Form 8606?

The IRS charges a $50 penalty for failing to file this form and a $100 penalty for overstating your basis. However, the true cost is the double taxation you will face in retirement.

The penalty for not filing form 8606 is $50 per year. While fifty dollars sounds minor, the real cost is the total loss of your tax basis.

Losing track of a $7,500 contribution could cost you $2,400 in unnecessary taxes if you sit in the 32% tax bracket during retirement. The IRS enforces a penalty for not filing form 8606 if they audit your conversion and find missing paperwork.

Overstating your basis carries a steeper $100 fine. This usually happens when a taxpayer guesses their historical basis instead of pulling the exact number from Line 14 of their previous return.

You can avoid the penalty for not filing form 8606 by showing reasonable cause. Attaching a brief letter explaining the oversight usually satisfies the IRS when submitting late forms. They generally prefer that you correct the record rather than hide the mistake.

Real-World Examples: How to Report Nondeductible IRA Form 8606

Let’s walk through some practical scenarios to see the math in action. These hypothetical examples illustrate exactly how different taxpayers handle the paperwork and how to report nondeductible ira form 8606 entries based on their unique financial situations.

Scenario 1: The Basic Nondeductible Contribution

Mark earns $200,000 in 2026 and participates in a workplace 401(k). He contributes $7,500 to a traditional IRA. Since his income exceeds the deduction limits, he reports this on Line 1.

He has no prior basis, so Line 2 is zero. His Line 14 shows $7,500, establishing his basis for future years.

| Form 8606 Line | Description | Amount |

|---|---|---|

| Line 1 | Nondeductible contributions for 2026 | $7,500 |

| Line 2 | Total basis from prior years | $0 |

| Line 3 | Total basis | $7,500 |

| Line 14 | Total basis for next year | $7,500 |

Scenario 2: The Clean Backdoor Roth Conversion

Sarah executes a clean Backdoor Roth conversion. She deposits $7,500 into a traditional IRA in 2026 and converts it immediately to a Roth IRA a few days later. She has no other pre-tax IRAs in her name.

Her paperwork shows $7,500 on Line 1 and $7,500 on Line 8 for the conversion. Because her December 31 balance for all traditional IRAs is zero, her nontaxable portion on Line 11 is $7,500.

Line 18 shows a taxable amount of $0. She successfully moved money into a Roth IRA without paying any additional taxes.

Scenario 3: The Pro-Rata Trap

David attempts the same strategy but already holds a $67,500 Rollover IRA from an old job. He contributes $7,500 nondeductible for 2026 and converts $7,500. His total IRA balance across all accounts is $75,000.

His $7,500 basis represents exactly 10% of the total. When he calculates Line 10, the decimal is 0.100. Multiplying his $7,500 conversion by 0.100 yields $750 on Line 11.

Only $750 of his conversion is tax-free. Line 18 shows that $6,750 is fully taxable as ordinary income, resulting in an unexpected tax bill.

Scenario 4: The Late Filer

Elena discovers she missed filing the form for a $7,000 contribution made in 2024. She prints the 2024 version of the document from the IRS website. After filling out Part I to establish her basis, she signs page two.

She mails it in standalone with a short letter explaining the oversight. By doing this, she ensures that when she eventually learns how to report nondeductible ira form 8606 entries for her future conversions, her historical basis is accurately recorded.

Form 8606 Instructions: Common Mistakes to Avoid

The most frequent errors include using the wrong year’s form, miscalculating the December 31 account value, and relying on a 1099-R instead of doing the math yourself.

The official form 8606 instructions span several pages of dense tax code, making it easy to overlook critical details. Reading the form 8606 instructions carefully prevents errors that trigger audits and unnecessary penalties.

Here are the most common pitfalls taxpayers face:

- Using the wrong year’s form: Always use the form that matches the tax year of the contribution, even if you are filing it several years late.

- Incorrect December 31 valuation: Taxpayers often use the account balance on the day of the conversion instead of the year-end balance. This throws off the entire Pro-Rata calculation.

- Forgetting to aggregate accounts: You must include all traditional, SEP, and SIMPLE IRAs on Line 6. Leaving one out invalidates your math.

- Relying on Form 1099-R: Box 2a on Form 1099-R often says “Taxable amount not determined.” Your custodian does not know your tax basis, so you must calculate the taxable amount yourself.

If the market goes up between your conversion date and December 31, your total balance increases, which changes the ratio and potentially increases your taxable amount. Always wait until January to finalize your year-end math.

Frequently Asked Questions About Form 8606

What happens if I forgot to file Form 8606 for past years?

You can file a late Form 8606 for previous tax years. The IRS allows you to submit this form retroactively to establish your basis, though you may need to attach a reasonable cause statement to avoid the late filing penalty. Simply print the form for the specific tax year you missed, fill it out, sign page two, and mail it to the IRS. Do not use the current year’s form for a past year’s contribution.

Do I need to file Form 8606 every year?

No, you only need to file it for years when you make a nondeductible contribution, take a distribution from an IRA with basis, or convert funds to a Roth IRA. If you simply hold the account and make no new contributions or withdrawals, you do not need to file the form for that specific tax year. Your basis simply remains intact until you need to use it.

Can I file Form 8606 electronically?

Yes, if you are filing it alongside your standard Form 1040 tax return using commercial tax software, it will be transmitted electronically. However, if you are filing it as a standalone document for a prior year, you must print it, sign it in ink, and mail it to the IRS processing center for your state.

Does a 401(k) balance affect Form 8606 calculations?

No, workplace retirement plans like a 401(k), 403(b), or TSP do not count toward the Pro-Rata rule calculation on Line 6. Only traditional, SEP, and SIMPLE IRAs are aggregated when determining the taxable portion of a conversion or distribution. This is why rolling pre-tax IRAs into a 401(k) is a popular strategy for isolating basis.

What is the easiest way to learn how to report nondeductible IRA Form 8606?

The easiest method is to use high-quality tax software that walks you through a step-by-step interview process. By answering questions about your contributions, existing IRA balances, and conversions, the software automatically populates the correct lines and carries your basis forward. However, understanding the underlying math ensures you catch any software input errors.

Is Form 8606 required for a Roth IRA contribution?

No, direct contributions to a Roth IRA are not reported on this form. This document is strictly for tracking after-tax money inside traditional IRAs and calculating the taxes owed when converting that money to a Roth IRA. Direct Roth contributions are tracked differently and do not require this specific paperwork.

How does the IRS know if I have IRA basis?

The IRS only knows you have basis if you tell them by filing this specific form. If you fail to file it, the IRS assumes your entire traditional IRA balance consists of pre-tax dollars. This assumption will result in full taxation upon withdrawal, meaning you will pay taxes twice on the same money.

What if my Form 5498 doesn’t match my Form 8606?

Form 5498 reports total contributions to the IRS, but it does not distinguish between deductible and nondeductible amounts. It is perfectly normal for Form 5498 to show a contribution while your tax return shows zero deduction, as long as it is properly reported as basis on your paperwork. The two forms serve different reporting purposes.

Can my spouse and I file a joint Form 8606?

No, IRAs are individual accounts. You and your spouse must each file your own separate form if you both make nondeductible contributions. Even if you file your taxes jointly as a married couple, the basis tracking remains completely separate for each person, and you cannot combine your IRA balances for the Pro-Rata calculation.

Do I include inherited IRAs on Form 8606?

Generally, no. Inherited IRAs are treated separately from your own personal IRAs for the Pro-Rata calculation. However, if the deceased person had unrecovered basis in their IRA, you may need to use their historical forms to ensure you do not pay taxes on their after-tax contributions when taking distributions from the inherited account.

Mastering how to report nondeductible ira form 8606 protects your wealth and ensures you keep more of your money in retirement. Take the time to file accurately, retain your records indefinitely, and consult a tax professional if your situation involves complex conversions or multiple account types.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.