High earners face a strict cutoff for direct Roth IRA contributions. The IRS sets the 2026 phase-out range at $153,000 to $168,000 for single filers, and $242,000 to $252,000 for married couples filing jointly. Earn one dollar over that upper limit, and you are entirely locked out of the front door.

You can bypass this restriction legally using a two-step conversion process. But there is a massive caveat hidden in the tax code. You must understand the IRS aggregation rules to avoid the backdoor roth tax trap. Failing to account for existing pre-tax IRA balances will turn a brilliant tax-free growth strategy into an immediate, unexpected tax liability.

Welcome to the definitive backdoor roth ira pro rata rule guide for 2026. We will break down the exact math the IRS uses, show you how to legally clear your accounts, and walk you through the required tax forms so you can invest with total confidence.

⚡ Executive Summary: 2026 Pro Rata Rule Facts

- The 2026 IRA contribution limit is $7,500, or $8,600 if you are age 50 or older.

- The IRS aggregates all Traditional, SEP, and SIMPLE IRAs on December 31 to calculate your pro rata tax liability.

- Workplace retirement plans like 401(k)s and 403(b)s do not count toward the pro rata calculation.

- You must file IRS Form 8606 to report your non-deductible basis and prove your conversion is tax-free.

Table of Contents

- Why You Need a Backdoor Roth IRA Pro Rata Rule Guide

- Understanding the IRS Aggregation Rules

- The Math: Pro Rata Rule for a Traditional IRA to Roth Conversion

- Step by Step Backdoor Roth IRA Instructions

- Strategies to Avoid the Backdoor Roth Tax Trap

- How to Avoid the Pro Rata Rule in a Backdoor Roth

- How to Empty a Traditional IRA for a Backdoor Roth

- Backdoor Roth IRA Form 8606 Walkthrough

- The December 31st Rule and Spousal Exceptions

- The Ultimate Backdoor Roth IRA Pro Rata Rule Guide Checklist

- Frequently Asked Questions About the Pro Rata Rule

Why You Need a Backdoor Roth IRA Pro Rata Rule Guide

Taxpayers researching backdoor roth ira high income limits quickly discover that while direct contributions are capped, the backdoor conversion process has no income ceiling. Anyone with earned income can make a non-deductible contribution to a Traditional IRA and immediately convert it to a Roth IRA.

A direct contribution requires you to meet strict modified adjusted gross income (MAGI) requirements. A conversion does not. Congress left this legal loophole open, and high-net-worth investors use it every single year to build tax-free wealth.

Following a reliable backdoor roth ira pro rata rule guide ensures you do not make unforced errors. The mechanics of the conversion are simple, but the tax reporting is unforgiving. If you have existing pre-tax money sitting in any non-Roth IRA, the IRS will force you to pay taxes on a portion of your conversion.

Understanding the IRS Aggregation Rules

The strategy sounds simple until you hit the aggregation rule. Under IRC Section 408(d)(2), the IRS views all your Traditional, SEP, and SIMPLE IRAs as a single, combined account. They do not care if you hold your pre-tax money at Vanguard and your new after-tax contribution at Fidelity.

You cannot cherry-pick which dollars you convert. If your total IRA holdings consist of 90% pre-tax money and 10% after-tax money, any conversion you make will be taxed at that exact 90/10 ratio. This proportional taxation is the core of the pro rata rule.

We built this guide to highlight the exact math the IRS uses. When you understand the formula, you can take proactive steps to isolate your after-tax dollars and protect your wealth from unnecessary taxation. Learn more about tracking IRA basis here.

The Math: Pro Rata Rule for a Traditional IRA to Roth Conversion

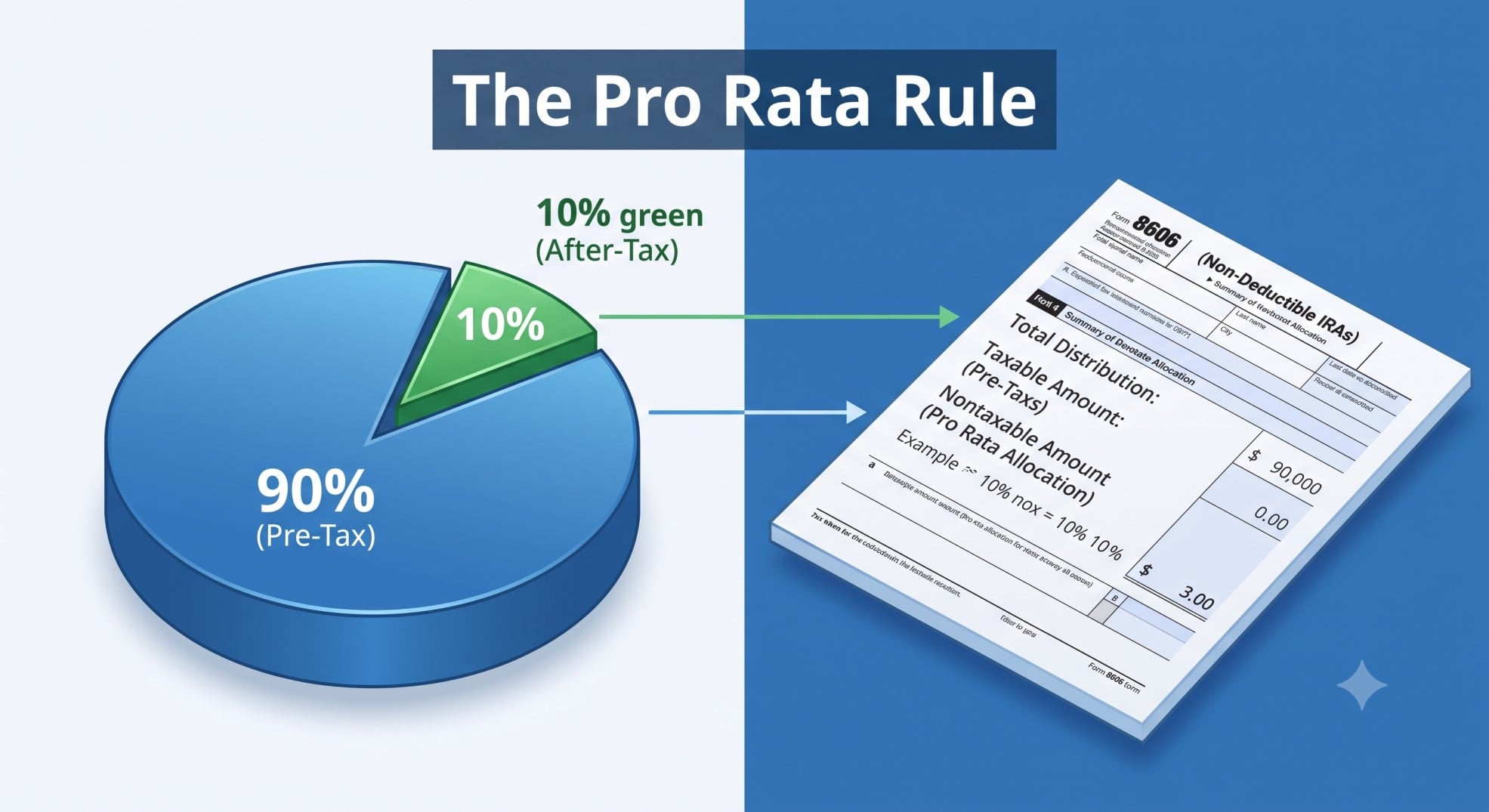

The pro rata rule for a traditional ira to roth conversion dictates that you cannot isolate after-tax dollars. The IRS calculates your tax liability by dividing your non-deductible contributions by your total IRA balance across all accounts.

Let us look at a real-world hypothetical scenario to see exactly how this impacts your tax return. Maria earns $200,000 as a single filer in 2026. She wants to execute a backdoor Roth conversion for the maximum $7,500. However, she has an old Rollover IRA from a previous employer containing $67,500 in pre-tax funds.

Her total combined IRA balance becomes $75,000 ($67,500 pre-tax + $7,500 after-tax). The IRS calculates her non-taxable percentage by dividing her after-tax basis ($7,500) by her total balance ($75,000). This equals exactly 10%.

If she converts $7,500 to her Roth IRA, only 10% of that conversion ($750) is tax-free. The remaining 90% ($6,750) is added to her taxable income for the year. Calculating the pro rata rule for a traditional ira to roth conversion requires precision, as Maria just accidentally triggered a tax bill on money she thought was protected.

She also leaves $6,750 of after-tax basis trapped inside her Traditional IRA. She will have to track this basis on Form 8606 for the rest of her life until the account is completely emptied.

Step by Step Backdoor Roth IRA Instructions

Executing this strategy cleanly requires strict adherence to the rules. Here are your step by step backdoor roth ira instructions for a flawless transaction.

Step one involves checking your existing IRA balances. Log into every brokerage account you own and verify that your Traditional, SEP, and SIMPLE IRA balances are exactly zero. If they are not zero, you must address them before proceeding.

Next, you will open a Traditional IRA and make a non-deductible contribution. For 2026, you can deposit up to $7,500 (or $8,600 if you are 50 or older). Do not invest these funds. Leave them in a cash or money market settlement fund to prevent any taxable earnings from accumulating.

Once the funds settle—usually within two to three business days—execute the conversion immediately. Your brokerage platform will have a specific button or form to convert the Traditional IRA balance into your Roth IRA.

Finally, you must report the transaction on your tax return. You will file Form 8606 to declare the non-deductible contribution and show the IRS that the conversion is not taxable. Skipping this final step will cause the IRS to assume the entire conversion was pre-tax, resulting in a massive tax bill.

Strategies to Avoid the Backdoor Roth Tax Trap

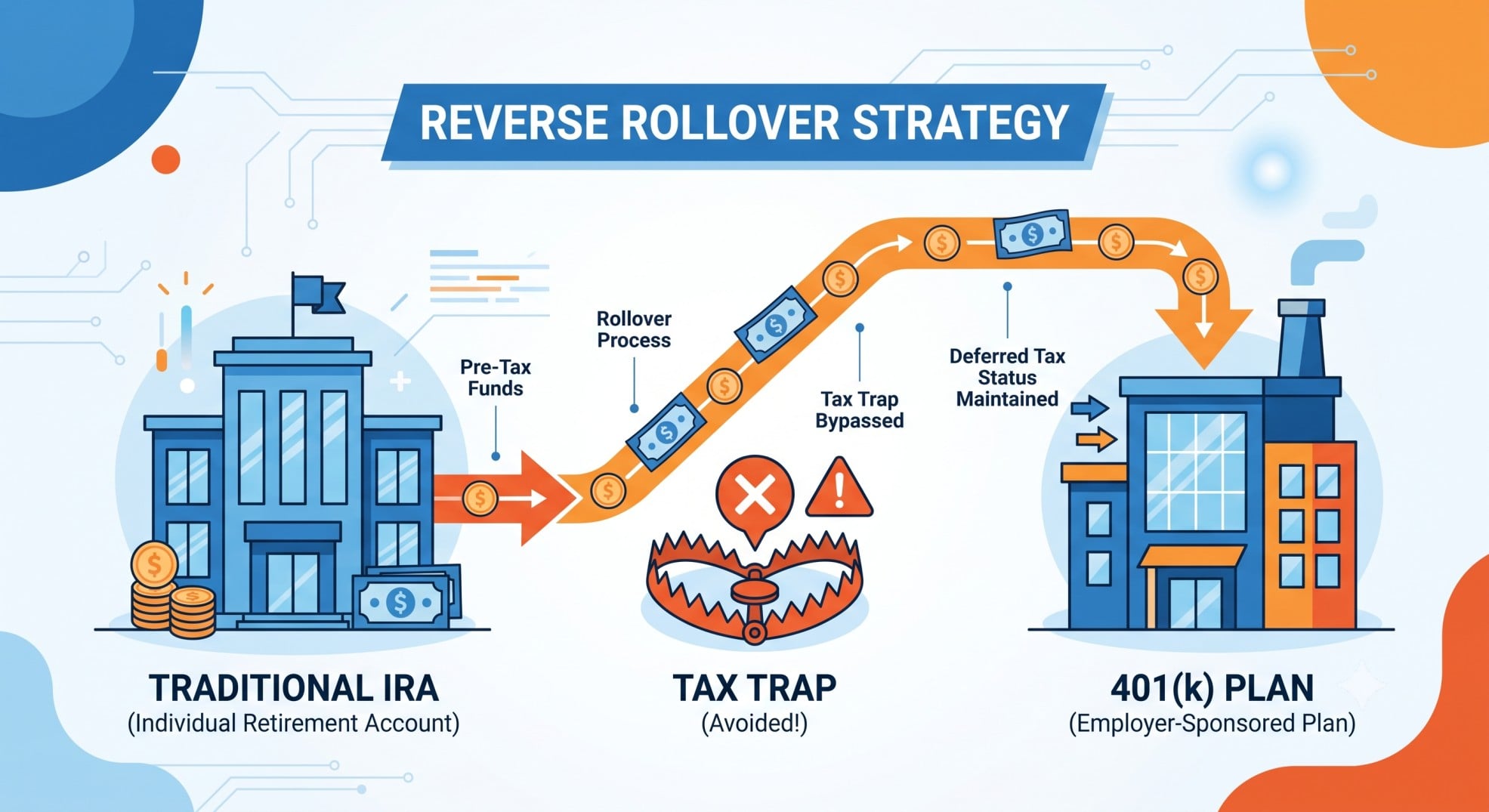

A reverse rollover is the cleanest way to avoid the backdoor roth tax trap. The IRS aggregation rules specifically exclude workplace retirement plans. Your 401(k), 403(b), and TSP balances do not count toward the pro rata calculation.

David earns $300,000 married filing jointly in 2026. He has a SEP IRA with $50,000 in pre-tax funds. He wants to do a backdoor Roth, but he knows the pro rata rule will penalize him.

He rolls the entire $50,000 SEP IRA balance into his current employer’s 401(k) plan in November 2026. By December 31, his SEP IRA balance is exactly zero. He then contributes $7,500 to a Traditional IRA and converts it.

Because his pre-tax money is safely hidden inside the 401(k), his pro rata calculation is 100% after-tax. He pays zero taxes on the conversion. You can roll over a traditional ira to a 401k for pro rata avoidance as long as your employer’s plan document allows inbound rollovers. Read our guide on 401(k) rollover rules.

How to Avoid the Pro Rata Rule in a Backdoor Roth

Taxpayers constantly ask how to avoid the pro rata rule in a backdoor roth without triggering an audit. The answer always comes down to timing and account location. You have three primary methods to clear your pre-tax balances.

The first method is the reverse rollover we just discussed. Understanding how to avoid the pro rata rule in a backdoor roth requires looking at your workplace retirement plans. Call your HR department and ask if your 401(k) accepts “inbound rollovers from a Traditional IRA.”

The second method is to bite the bullet and convert the entire pre-tax balance. If your pre-tax IRA balance is very small—say, $2,000—it might make sense to just convert the whole thing to Roth. You will pay the taxes on the $2,000 this year, but you will enjoy a clean slate for all future backdoor conversions.

The third method applies to business owners. If you have freelance income, you can open a Solo 401(k). You can then roll your pre-tax IRA funds into the Solo 401(k), effectively hiding them from the IRS pro rata calculation.

How to Empty a Traditional IRA for a Backdoor Roth

Moving money out of your IRA requires strict attention to detail. If you are wondering how to empty a traditional ira for a backdoor roth, you must initiate a direct trustee-to-trustee transfer.

Your current IRA custodian will send a check directly to your 401(k) provider. Do not take personal possession of the funds. If the check is made payable to you, the IRS considers it a distribution, and you have exactly 60 days to deposit it into the 401(k) before it becomes fully taxable.

Self-employed individuals have a distinct advantage here. By setting up a Solo 401(k) with a provider that allows inbound rollovers, you create your own safe haven for pre-tax IRA funds. Just ensure the Solo 401(k) is officially established before December 31 of the conversion year.

Backdoor Roth IRA Form 8606 Walkthrough

A proper backdoor roth ira form 8606 walkthrough shows exactly where the IRS tracks your non-deductible basis. This form is mandatory. If you fail to file it, the IRS will tax your conversion by default.

We highly recommend reviewing this backdoor roth ira form 8606 walkthrough before filing your return. The math is straightforward, but placing the numbers on the wrong lines will trigger an automated IRS notice.

| Form 8606 Line | What You Enter (2026 Example) | Explanation |

|---|---|---|

| Line 1 | $7,500 | Your total non-deductible contribution for the 2026 tax year. |

| Line 2 | $0 | Your total basis from prior years. If this is your first time, enter zero. |

| Line 3 | $7,500 | Add lines 1 and 2. This is your total after-tax basis. |

| Line 6 | $0 | The total value of all your Traditional, SEP, and SIMPLE IRAs on Dec 31, 2026. |

| Line 8 | $7,500 | The net amount you converted to a Roth IRA during the year. |

| Line 10 | 1.000 | Divide line 3 by line 9. This decimal represents your non-taxable percentage. |

| Line 16 | $0 | The taxable amount of your conversion. A clean backdoor Roth will show zero here. |

The IRS requires you to round the decimal on Line 10 to at least three places. If your pre-tax balances are zero, the math cleanly results in a 1.000 multiplier, meaning 100% of your conversion is tax-free. Read our full guide on IRS Form 8606 instructions.

The December 31st Rule and Spousal Exceptions

Timing matters immensely when dealing with the IRS. The pro rata rule does not care what your IRA balance was on the day you executed the conversion. It only cares what your balance is on December 31 of the year the conversion takes place.

Sarah executes a flawless backdoor Roth conversion in February 2026. At the time, she has zero dollars in any other IRAs. She assumes she is completely safe from the pro rata rule.

In August 2026, she leaves her corporate job and rolls her $92,500 401(k) into a Traditional IRA for better investment options. On December 31, 2026, her Traditional IRA balance sits at $92,500.

Because the IRS looks at the end-of-year balance, Sarah just accidentally triggered the pro rata rule retroactively. Her $7,500 conversion from February will now be heavily taxed because she introduced pre-tax money into the IRA ecosystem before the year closed.

Spouses, however, get a massive break here. IRAs are Individual Retirement Accounts. The IRS calculates the pro rata rule per person, not per couple. If John has a $100,000 pre-tax IRA, but his wife Jane has zero pre-tax IRA balances, Jane can execute a backdoor Roth conversion completely tax-free. John’s balances do not affect Jane’s math.

The Ultimate Backdoor Roth IRA Pro Rata Rule Guide Checklist

Before you move a single dollar, you must verify your accounts. A single mistake can cost you thousands in unexpected taxes. Use this backdoor roth ira pro rata rule guide checklist to ensure compliance.

First, confirm your MAGI exceeds the direct contribution limits. Second, verify that your Traditional, SEP, and SIMPLE IRA balances will be exactly zero on December 31. Third, ensure you have the cash to make the non-deductible contribution.

Fourth, execute the conversion immediately after the funds settle to avoid taxable interest. Finally, give your CPA a heads-up so they know to file Form 8606 during tax season. Find a qualified tax professional here.

Frequently Asked Questions About the Pro Rata Rule

What is the pro rata rule for a traditional ira to roth conversion?

The pro rata rule is an IRS regulation that prevents taxpayers from isolating after-tax dollars during a Roth conversion. If you have a mix of pre-tax and after-tax money across any of your Traditional, SEP, or SIMPLE IRAs, the IRS taxes your conversion proportionally based on the total combined balance.

How do I calculate the taxable portion of my conversion?

You calculate the taxable portion by dividing your total non-deductible (after-tax) contributions by the total value of all your non-Roth IRAs combined. This gives you a percentage. Multiply that percentage by your conversion amount to find the tax-free portion. The rest is taxable.

Does my spouse’s IRA affect my pro rata calculation?

No. IRAs are individual accounts. The IRS calculates the pro rata rule based solely on your own Social Security Number. Your spouse can have a massive pre-tax Traditional IRA, and it will not impact your ability to execute a clean backdoor Roth conversion.

Do inherited IRAs count toward the pro rata rule?

No. Inherited IRAs are treated as entirely separate entities under IRS rules. They are not aggregated with your personal Traditional, SEP, or SIMPLE IRAs when calculating your conversion taxes.

Does a 401(k) or 403(b) count toward the pro rata rule?

No. Workplace retirement plans, including 401(k)s, 403(b)s, and the Thrift Savings Plan (TSP), are explicitly excluded from the IRS aggregation rules. This exclusion is what makes the reverse rollover strategy possible.

What is the best method for how to avoid the pro rata rule in a backdoor roth?

The most effective method is the reverse rollover. By transferring all your pre-tax IRA funds into a current employer’s 401(k) or a Solo 401(k) before December 31, you legally clear your IRA balances and ensure your conversion is 100% tax-free.

What happens if I forget to file Form 8606?

If you fail to file Form 8606, the IRS has no record of your non-deductible basis. They will assume the entire conversion consisted of pre-tax funds and will send you a CP2000 notice demanding taxes and potential penalties on the full converted amount.

Can I undo a Roth conversion if I get hit with the pro rata tax?

No. The Tax Cuts and Jobs Act (TCJA) permanently banned the recharacterization (undoing) of Roth conversions. Once you convert the funds, the transaction is final, and you are locked into whatever tax liability the pro rata rule generates.

Where can I find a reliable backdoor roth ira form 8606 walkthrough?

You can use the step-by-step table provided earlier in this guide, or consult the official IRS instructions for Form 8606. Always ensure you are using the form designated for the specific tax year in which the conversion occurred.

How do I avoid the backdoor roth tax trap if I have a SEP IRA?

SEP IRAs are subject to the pro rata rule. To avoid the tax trap, you must roll the SEP IRA balance into a workplace 401(k) or a Solo 401(k) before December 31 of the year you perform the backdoor Roth conversion.

Bookmark this backdoor roth ira pro rata rule guide for your end-of-year tax planning. By understanding the math, utilizing reverse rollovers, and filing Form 8606 correctly, you can secure decades of tax-free growth without triggering an IRS audit.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.