For High-Net-Worth Individuals, the promise of preferential tax rates on qualified dividends can be a cornerstone of wealth management. However, in the complex tax environment of 2026, these rates are just one piece of a much larger, often challenging, puzzle. Understanding how federal, state, and specialized taxes like the Net Investment Income Tax (NIIT) affect your investment income is essential for preserving and growing your wealth. This guide provides clear, strategic insights to help you understand qualified dividend tax impacts for the upcoming tax year.

Executive Summary

- Preferential Rates: Qualified dividends are taxed at 0%, 15%, or 20% federal rates, depending on your taxable income.

- HNWI Complexity: For High-Net-Worth Individuals, these rates are often influenced by the 3.8% Net Investment Income Tax (NIIT), potential Alternative Minimum Tax (AMT), and varying state income taxes.

- NIIT Thresholds: The NIIT applies to investment income when Modified Adjusted Gross Income (MAGI) exceeds $250,000 for married filing jointly or $200,000 for single filers in 2026.

- Holding Period: Strict adherence to holding period rules is critical for dividends to qualify for lower rates.

- Strategic Planning: Effective HNWI tax planning involves asset location, MAGI management, and continuous monitoring of legislative changes.

Introduction: The 2026 Tax Landscape for HNWI Investment Income

Qualified dividends generally offer a significant tax advantage. They are often taxed at lower rates than ordinary income. However, for High-Net-Worth Individuals (HNWI), the 2026 tax landscape presents unique complexities. The NIIT, potential AMT, and state income taxes can significantly alter the effective tax burden. This guide aims to simplify that complexity. It gives HNWIs a clear understanding of their obligations and strategic planning opportunities for 2026. Proactive, holistic tax planning is crucial.

What Are Qualified Dividends? A Foundation for HNWI Planning

Understanding what makes a dividend qualified is the first step in effective HNWI tax planning. These dividends get preferential tax treatment, a key part of many investment strategies.

Defining Qualified Dividend Income (QDI)

The Internal Revenue Code (IRC) Section 1(h)(11) provides the legal basis for qualified dividend income. These dividends generally come from domestic corporations. They can also originate from certain qualified foreign corporations. A foreign corporation is qualified if its stock trades on an established U.S. securities market. Alternatively, it might be incorporated in a U.S. possession. It could also be eligible for benefits under a comprehensive income tax treaty with the United States. This treaty must include an exchange of information program. IRS Notice 2024-11 updates the list of countries with qualifying tax treaties. For instance, Chile was added, while Russia and Hungary were removed.

The Critical Holding Period Requirement

To be considered qualified, stock must meet a specific holding period. You must hold the stock for more than 60 days. This period falls within the 121-day window. This window begins 60 days before the ex-dividend date. For certain preferred shares, the requirement is stricter. The stock must be held for at least 91 days within a 181-day period. Failing this requirement means the dividends are taxed as ordinary income.

Exclusions: When Dividends Are NOT Qualified

Not all dividends qualify for preferential rates. For example, dividends from Real Estate Investment Trusts (REITs) are typically excluded. Master Limited Partnerships (MLPs) also generally pay non-qualified dividends. Dividends from tax-exempt organizations do not qualify. Furthermore, dividends from certain pass-through entities are often not qualified. Lastly, dividends on stock held for insufficient periods are also excluded from qualified status.

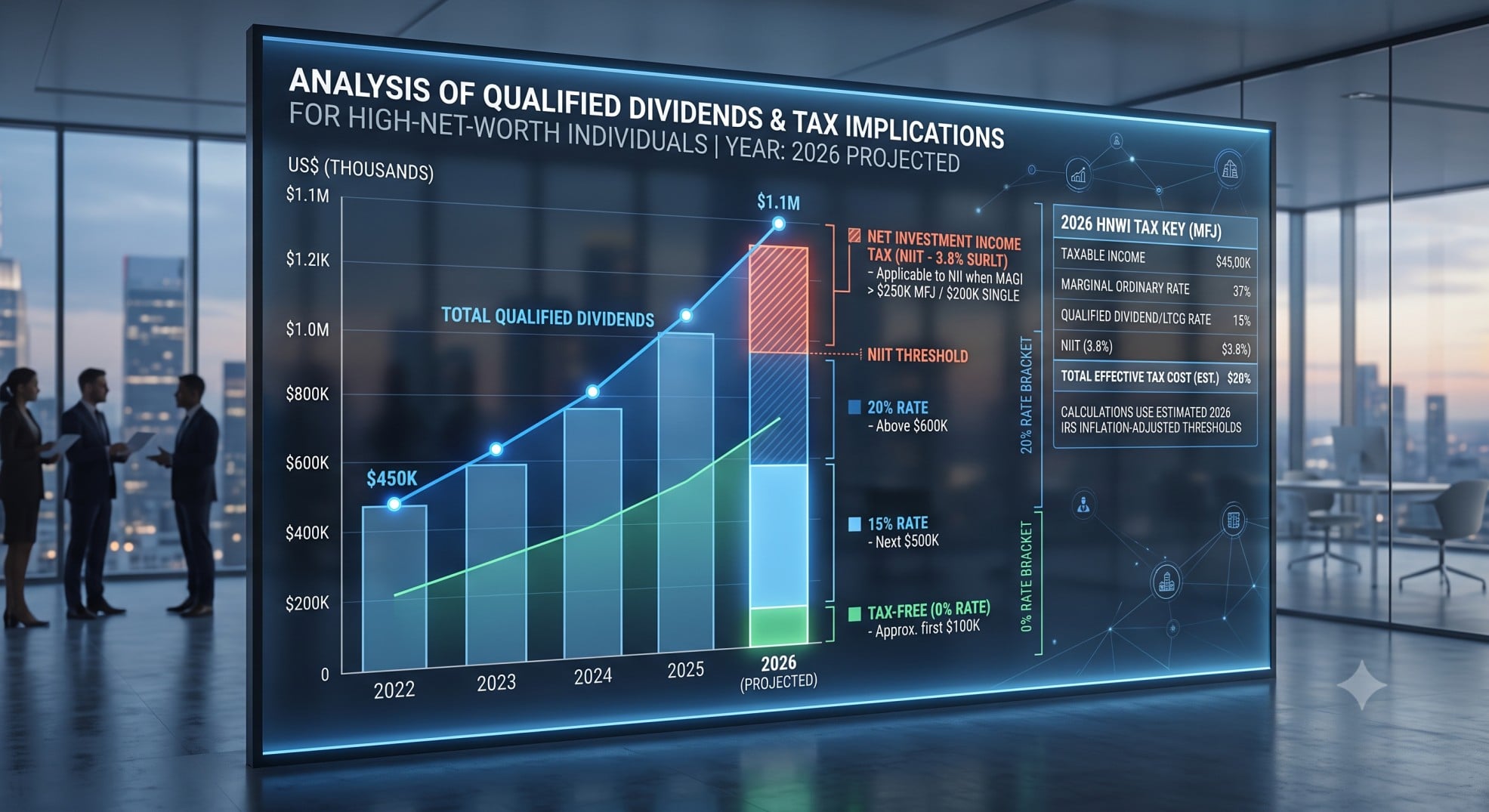

2026 Federal Tax Rates for Qualified Dividends: The Preferential Treatment

Qualified dividends are taxed at rates similar to long-term capital gains. These rates are much lower than ordinary income tax rates, making them attractive for investors.

Understanding the Long-Term Capital Gains Rates

Qualified dividends are taxed at 0%, 15%, or 20%. These rates depend on your overall taxable income and filing status. Reviewing your total income is essential to apply the correct rate.

Detailed 2026 Qualified Dividend Tax Rate Tables

The following tables, based on Revenue Procedure 2025-32, detail the 2026 qualified dividend tax impacts. These thresholds are critical for HNWI tax planning.

Single Filers (Taxable Income)

| Tax Rate | Taxable Income |

|---|---|

| 0% | Up to $49,450 |

| 15% | $49,451 to $545,500 |

| 20% | Over $545,500 |

Married Filing Jointly (Taxable Income)

| Tax Rate | Taxable Income |

|---|---|

| 0% | Up to $98,900 |

| 15% | $98,901 to $613,700 |

| 20% | Over $613,700 |

Head of Household (Taxable Income)

| Tax Rate | Taxable Income |

|---|---|

| 0% | Up to $66,200 |

| 15% | $66,201 to $579,600 |

| 20% | Over $579,600 |

Married Filing Separately (Taxable Income)

| Tax Rate | Taxable Income |

|---|---|

| 0% | Up to $49,450 |

| 15% | $49,451 to $306,850 |

| 20% | Over $306,850 |

Beyond the Preferential Rates: HNWI Tax Multipliers in 2026

While the preferential rates for qualified dividends are attractive, HNWIs face additional taxes. These can significantly increase the overall tax burden. Understanding these multipliers is important for effective HNWI tax planning.

The Net Investment Income Tax (NIIT): A 3.8% Surcharge

The Net Investment Income Tax (NIIT), outlined in IRC Section 1411, is a 3.8% surcharge. It applies to high-income taxpayers. This tax targets the lesser of your net investment income or the amount by which your Modified Adjusted Gross Income (MAGI) exceeds specific thresholds. For 2026, the NIIT thresholds are:

- $200,000 for single filers and heads of household.

- $250,000 for married couples filing jointly and qualifying surviving spouses.

- $125,000 for married individuals filing separately.

- For estates and trusts, the NIIT applies if Adjusted Gross Income (AGI) exceeds $16,000.

It is important to note that NIIT thresholds are statutory amounts. They are not adjusted for inflation. Thus, more individuals may fall into its scope over time. This 3.8% can push the effective rate on qualified dividend tax impacts to 23.8% (20% + 3.8%).

Alternative Minimum Tax (AMT) Considerations for HNWIs

The Alternative Minimum Tax (AMT) is a parallel tax system. It ensures high-income taxpayers pay at least a minimum amount of tax. Certain deductions, like state and local taxes, are added back for AMT. This can trigger AMT liability for HNWIs. While qualified dividends themselves are generally treated favorably under AMT, the overall increase in your federal tax bill due to AMT can indirectly affect your after-tax return on these investments.

The Impact of State Income Taxes

State income taxes represent a significant portion of the overall tax bill, especially in high-tax states like California. While state taxes are generally deductible federally, they are subject to the SALT cap. This cap limits the deduction to $10,000 per household. State tax treatment of qualified dividends varies. Some states tax them as ordinary income, while others offer preferential rates. Therefore, state taxes are a critical component of the total qualified dividend tax impacts.

Real-World Scenario: The Sterling Family’s 2026 Qualified Dividend Tax Impact

This case study illustrates the complex tax landscape for High-Net-Worth Individuals (HNWI) in 2026. It focuses on the impact of qualified dividends. We will examine a realistic scenario for a married couple residing in California. This demonstrates how various federal and state taxes interact.

Scenario Overview: The Sterling Family (2026)

Meet the Sterlings, a high-net-worth couple filing jointly in California. Their financial profile for 2026 includes substantial income from various sources and significant itemized deductions. This scenario highlights how preferential tax rates for qualified dividends can be influenced by other taxes applicable to HNWIs.

- Income Sources:

- Salary: $700,000

- Qualified Dividends: $500,000

- Other Investment Income (e.g., interest, short-term capital gains): $300,000

- Total Adjusted Gross Income (AGI): $1,500,000

- Itemized Deductions (before federal SALT cap):

- California State Income Tax Paid: $150,000

- Property Taxes: $20,000

- Mortgage Interest: $30,000

- Charitable Contributions: $50,000

Strategic Tax Planning for HNWIs: Optimizing Qualified Dividends in 2026

Proactive planning is essential for HNWIs to optimize the qualified dividend tax impacts. This involves careful asset placement, income management, and staying informed about legislative changes.

Asset Location Strategies

Smart asset location can significantly reduce your tax burden. Placing qualified dividend-paying stocks in taxable accounts is often advisable. Their preferential rates make them more tax-efficient there. Conversely, non-qualified dividends, high-yield bonds, and REITs are better suited for tax-advantaged accounts. These include IRAs or 401(k)s. In these accounts, their ordinary income is tax-deferred or tax-free.

Managing Modified Adjusted Gross Income (MAGI) to Mitigate NIIT

Controlling your Modified Adjusted Gross Income (MAGI) is crucial to stay below the Net Investment Income Tax (NIIT) thresholds. Several strategies can assist with this:

- Tax-Loss Harvesting: Utilize investment losses to offset capital gains. This can reduce overall taxable income and MAGI.

- Roth Conversions: Strategically time Roth conversions during lower-income years. This locks in tax-free growth. It also reduces future taxable income that could push MAGI above NIIT thresholds.

- Charitable Giving: Employ Qualified Charitable Distributions (QCDs) from IRAs for individuals over 70.5. Donating appreciated securities to Donor-Advised Funds (DAFs) can also reduce taxable income and MAGI.

- Timing of Income Recognition: Carefully plan the recognition of bonuses, capital gains, and other income streams. This avoids unnecessary “bracket creep” into higher tax tiers or NIIT applicability.

Strict Adherence to Holding Period Requirements

Meeting the holding period requirements is essential. This ensures your dividends qualify for the lower rates. Avoid short-term trading around ex-dividend dates if preferential tax treatment is your goal. The IRS closely scrutinizes these transactions.

Continuous Monitoring of Legislative Changes

While the Tax Cuts and Jobs Act (TCJA) provisions affecting individual income taxes were made permanent by the “One Big Beautiful Bill Act” (OBBBA) in July 2025, vigilance is still advised. Future legislative changes are always possible. Continuous monitoring of tax law developments is a critical aspect of HNWI tax planning. Stay informed through reliable sources like the IRS website or reputable financial news outlets such as The Wall Street Journal.

Conclusion: Proactive Planning is Your Best Defense

Preferential rates for qualified dividends offer a valuable tax advantage. For High-Net-Worth Individuals, however, this benefit is complex. The Net Investment Income Tax (NIIT), potential Alternative Minimum Tax (AMT), and state taxes significantly impact the effective rate. A holistic, integrated tax planning approach is essential. Proactive planning helps preserve and grow your wealth. We strongly recommend consulting with a qualified tax professional for personalized advice. They can tailor strategies to your specific financial situation.