As we approach the 2026 tax year, understanding the federal income tax brackets is essential for effective financial planning. Recent legislative changes have made many individual tax provisions more stable. However, annual inflation adjustments mean the exact thresholds have shifted. This guide breaks down everything general taxpayers need to know about the 2026 federal tax brackets, standard deductions, and other key tax figures. It helps you prepare to manage your tax situation effectively.

Key 2026 Tax Updates

- The seven federal tax brackets (10% to 37%) remain, but income thresholds have increased due to inflation.

- The Standard Deduction amounts are higher for all filing statuses in 2026.

- A new temporary “bonus” deduction is available for older adults.

- The State and Local Tax (SALT) deduction cap has increased to $40,400.

- Many individual tax provisions, including the Qualified Business Income (QBI) deduction, are now permanent.

Understanding How Federal Tax Brackets Work

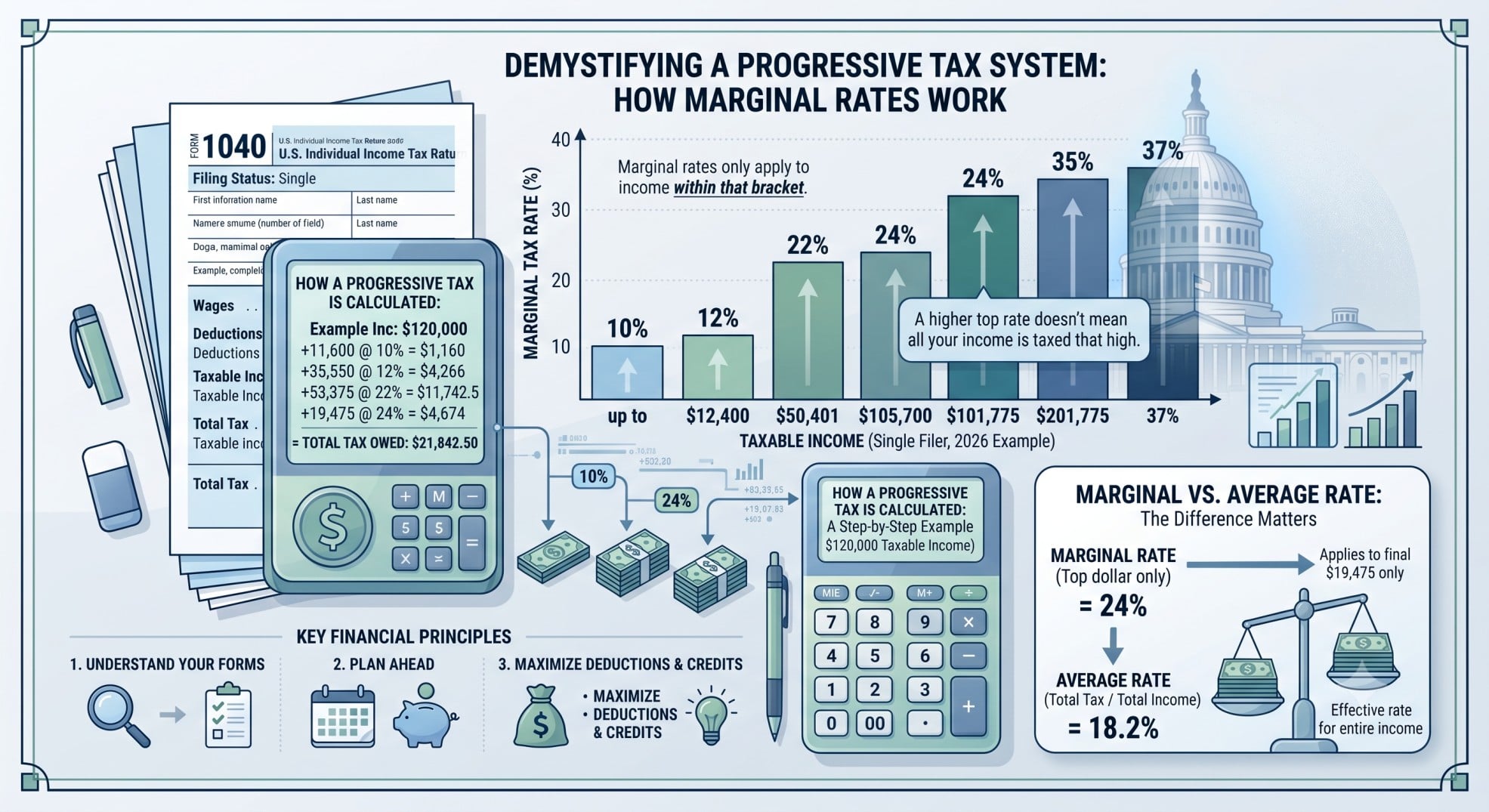

The United States uses a progressive tax system. This means different portions of your income are taxed at different rates. Therefore, not all your income is taxed at your highest bracket.

Marginal Tax Rates Explained

A tax bracket refers to a range of income taxed at a specific rate. This rate is called the marginal tax rate. For example, the first portion of your taxable income might be taxed at 10%. The next portion could be taxed at 12%. This system ensures that higher earners pay a larger percentage of their income in taxes.

Consider this: if the 10% bracket covers income up to $12,400, and the 12% bracket covers income up to $50,400, only the income within each range is taxed at that specific rate. Your total tax bill is the sum of taxes from each bracket.

Taxable Income vs. Gross Income

Your journey to calculating federal tax brackets for 2026 begins with your gross income. This is your total income from all sources before any deductions. Then, certain adjustments reduce your gross income to arrive at your Adjusted Gross Income (AGI). Furthermore, you subtract either the Standard Deduction or your itemized deductions from your AGI. This final figure is your taxable income. Only your taxable income is subject to the federal tax brackets.

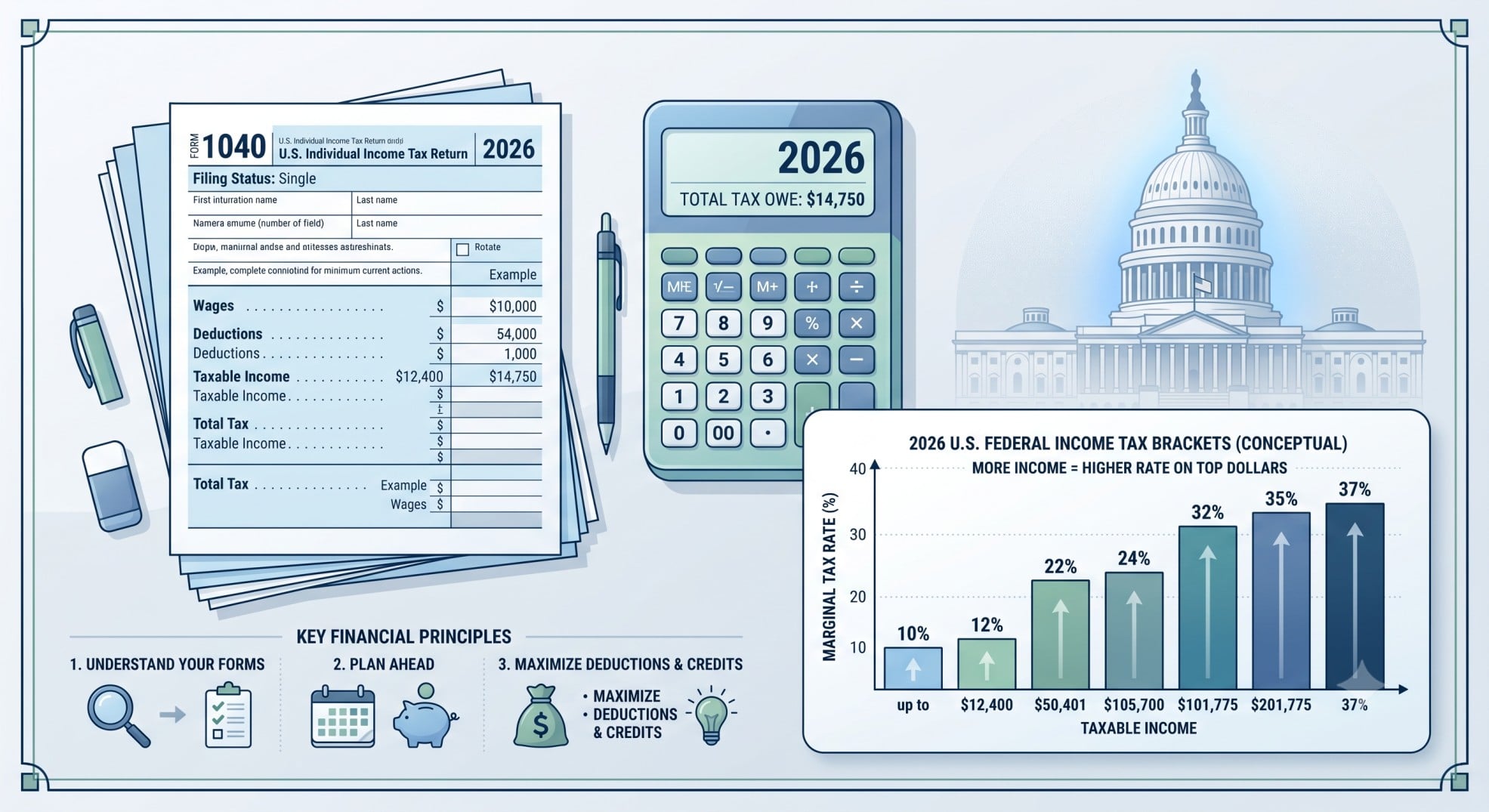

2026 Federal Income Tax Brackets and Rates

The 2026 federal tax brackets feature seven rates, ranging from 10% to 37%. These income thresholds are adjusted annually for inflation. This prevents taxpayers from moving into higher brackets simply due to rising costs of living. The “One Big Beautiful Bill Act (OBBBA)” passed in July 2025 made many of these provisions permanent. Therefore, taxpayers can expect stability in the overall structure.

Detailed Tax Rate Schedules for Each Filing Status

Here are the official 2026 federal tax brackets, as released by the IRS in Revenue Procedure 2025-32:

| Tax Rate | Single Filers (Taxable Income) | Married Filing Jointly (Taxable Income) | Head of Household (Taxable Income) | Married Filing Separately (Taxable Income) |

|---|---|---|---|---|

| 10% | $0 to $12,400 | $0 to $24,800 | $0 to $17,700 | $0 to $12,400 |

| 12% | $12,401 to $50,400 | $24,801 to $100,800 | $17,701 to $67,450 | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 | $100,801 to $211,400 | $67,451 to $105,700 | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 | $211,401 to $403,550 | $105,701 to $201,775 | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 | $403,551 to $512,450 | $201,776 to $256,225 | $201,776 to $256,225 |

| 35% | $256,226 to $640,600 | $512,451 to $768,700 | $256,226 to $640,600 | $256,226 to $384,350 |

| 37% | Over $640,600 | Over $768,700 | Over $640,600 | Over $384,350 |

Key Deductions for 2026

Deductions reduce your taxable income. This directly impacts how much you pay in taxes. Understanding these key deductions is vital for effective tax planning.

Standard Deduction Amounts

Most taxpayers claim the Standard Deduction. This reduces your taxable income without needing to itemize. The standard deduction 2026 amounts have increased due to inflation. Here are the figures:

| Filing Status | 2026 Standard Deduction |

|---|---|

| Single | $16,100 |

| Married Filing Jointly | $32,200 |

| Head of Household | $24,150 |

| Married Filing Separately | $16,100 |

Additional Standard Deduction for Older Adults and the Blind

Older adults or individuals who are blind can claim an additional Standard Deduction amount. For 2026, this amount is $1,650 per qualifying individual for married filers. It is $2,050 per qualifying individual for single or head of household filers. This provides further tax relief for these groups.

Personal Exemptions (Still $0 for 2026)

For 2026, personal exemptions remain at $0. The OBBBA made this provision permanent. It continues a change first introduced by the Tax Cuts and Jobs Act (TCJA).

State and Local Tax (SALT) Deduction Cap

The OBBBA increased the cap on the itemized deduction for state and local taxes. For 2026, this cap is $40,400. It is $20,200 for married individuals filing separately. This cap may gradually reduce if your modified Adjusted Gross Income (MAGI) exceeds $505,000. However, it will not fall below $10,000 ($5,000 for married individuals filing separately).

New Temporary “Bonus” Deduction for Older Adults

The OBBBA introduced a temporary additional deduction for older adults. This deduction is up to $6,000 per person. For married couples where both qualify, this could be up to $12,000. This deduction is available whether you itemize or take the Standard Deduction. It begins to phase out for single filers with MAGI over $75,000. For married couples filing jointly, it phases out with MAGI over $150,000. This deduction runs through the 2028 tax year.

Other Important Tax Considerations for 2026

Capital Gains Tax Rates

Your investments can generate capital gains. These are taxed differently depending on how long you held the asset. Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rates. However, long-term capital gains (assets held for more than one year) receive preferential rates. The capital gains tax rates for 2026 are 0%, 15%, and 20%.

| Rate | Single Filers (Taxable Income) | Married Filing Jointly (Taxable Income) | Head of Household (Taxable Income) |

|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $66,300 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 | $66,301 to $580,300 |

| 20% | Over $545,500 | Over $613,700 | Over $580,300 |

Net Investment Income Tax (NIIT)

An additional 3.8% Net Investment Income Tax (NIIT) may apply to certain investment income. This tax affects high-income households. The income thresholds for NIIT are $200,000 for single filers, $250,000 for married couples filing jointly, and $125,000 for married individuals filing separately.

Alternative Minimum Tax (AMT)

The Alternative Minimum Tax (AMT) ensures that high-income earners pay a minimum amount of tax. It operates alongside the regular income tax system. For 2026, the AMT exemption amounts are $90,100 for single filers, $140,200 for married couples filing jointly, and $70,100 for married individuals filing separately. These exemptions begin to phase out at higher income levels: for single filers at $500,000, for married couples filing jointly at $1,000,000, and for married individuals filing separately at $500,000. The AMT exemption phases out at 25 cents for every dollar of Alternative Minimum Taxable Income (AMTI) above these thresholds. The OBBBA’s changes to the AMT return the phaseout thresholds to 2018 levels and accelerate the phaseout rate from 25 percent previously.

Qualified Business Income (QBI) Deduction (§199A)

The 20% deduction for qualified business income from pass-through businesses was made permanent by the OBBBA. For 2026, limits on this deduction begin to phase in for taxpayers with income above $201,775 (single) or $403,500 (married filing jointly).

Real-World Scenario: Applying the 2026 Tax Brackets

Let’s consider Maria, a single filer, and David and Sarah, a married couple filing jointly. This illustrates how the 2026 federal tax brackets apply to real situations.

Maria’s Situation (Single Filer):

- Gross Income: $70,000

- Standard Deduction: Maria takes the 2026 Standard Deduction for a single filer, which is $16,100.

- Taxable Income Calculation:

- $70,000 (Gross Income) – $16,100 (Standard Deduction) = $53,900 (Taxable Income)

Now, let’s apply the 2026 federal tax brackets for single filers to Maria’s taxable income of $53,900:

- 10% Bracket: The first $12,400 is taxed at 10%.

- $12,400 * 0.10 = $1,240

- 12% Bracket: The income between $12,401 and $50,400 is taxed at 12%.

- ($50,400 – $12,400) = $38,000

- $38,000 * 0.12 = $4,560

- 22% Bracket: The income between $50,401 and $105,700 is taxed at 22%. Maria’s remaining taxable income falls into this bracket.

- ($53,900 – $50,400) = $3,500

- $3,500 * 0.22 = $770

Maria’s Total Federal Income Tax Liability:

- $1,240 (from 10% bracket) + $4,560 (from 12% bracket) + $770 (from 22% bracket) = $6,570

David and Sarah’s Situation (Married Filing Jointly):

- Combined Gross Income: $150,000

- Standard Deduction: David and Sarah take the 2026 Standard Deduction for married filing jointly, which is $32,200.

- Taxable Income Calculation:

- $150,000 (Gross Income) – $32,200 (Standard Deduction) = $117,800 (Taxable Income)

Now, let’s apply the 2026 federal tax brackets for married filing jointly to their taxable income of $117,800:

- 10% Bracket: The first $24,800 is taxed at 10%.

- $24,800 * 0.10 = $2,480

- 12% Bracket: The income between $24,801 and $100,800 is taxed at 12%.

- ($100,800 – $24,800) = $76,000

- $76,000 * 0.12 = $9,120

- 22% Bracket: The income between $100,801 and $211,400 is taxed at 22%. Their remaining taxable income falls into this bracket.

- ($117,800 – $100,800) = $17,000

- $17,000 * 0.22 = $3,740

David and Sarah’s Total Federal Income Tax Liability:

- $2,480 (from 10% bracket) + $9,120 (from 12% bracket) + $3,740 (from 22% bracket) = $15,340

This scenario demonstrates how the progressive tax system works. Different portions of taxable income are taxed at different marginal rates. The Standard Deduction also significantly impacts the final tax liability.

Key Takeaways for 2026 Tax Planning

The 2026 tax year brings stability to many individual tax provisions. This is largely due to the OBBBA. However, inflation adjustments mean higher income thresholds for the federal tax brackets and deductions. The increased standard deduction 2026 amounts will benefit many taxpayers. Furthermore, new deductions for older adults offer additional relief.

Proactive tax planning is essential. Review your income, deductions, and potential capital gains tax implications. Consider adjusting your withholdings to avoid surprises. For personalized advice, always consult a qualified tax professional.

Conclusion

Understanding the 2026 federal tax brackets and related provisions is a cornerstone of sound financial health. The information provided here aims to equip general taxpayers with the knowledge needed for the upcoming tax season. Staying informed about these changes allows you to make better financial decisions. For the most current official guidance, always refer to the IRS website. Stay tuned for more updates, and consider consulting a tax advisor for your specific situation.

Citations

- IRS Revenue Procedure 2025-32

- Internal Revenue Code (IRC) Sections 1, 55, 63, 1222

- “One Big Beautiful Bill Act (OBBBA)” (July 2025)

- Tax Cuts and Jobs Act (TCJA) of 2017

- Tax Foundation analysis of 2026 tax parameters