For millions of Americans, student loans are a significant financial reality. As we approach July 2026, a series of significant student loan changes 2026 are set to reshape how student loans work. These updates impact everything from how your forgiven debt is taxed to the very structure of federal repayment plans. Are you prepared for the “tax bomb” on forgiven loans? Do you understand the new borrowing limits or the future of income-driven repayment? This comprehensive guide explains clearly, offering clear, actionable strategies to help you understand these critical updates and protect your financial future.

Executive Summary

- Most student loan forgiveness becomes federally taxable again starting January 1, 2026.

- New federal loans disbursed on or after July 1, 2026, will have new repayment options and borrowing limits.

- Existing Income-Driven Repayment (IDR) plans like SAVE, PAYE, and ICR will phase out for current borrowers by July 1, 2028.

- Public Service Loan Forgiveness (PSLF) remains federally tax-free.

- The student loan interest deduction continues to offer a valuable tax benefit.

- Proactive planning is essential to reduce potential tax bills and adapt to new repayment structures.

I. Understanding 2026 Student Loan Changes

A. The Dual Impact of 2026: Taxability and Repayment Overhaul

The year 2026 marks an important change for millions of Americans with student loans. First, the federal tax exemption for most student loan forgiveness expires. This means that forgiven loan amounts will generally be considered taxable income again. Second, new legislation, known as the “Working Families Tax Cuts Act” (or “One Big Beautiful Bill Act”), brings significant changes to federal loan programs. These student loan changes 2026 will reshape available repayment plans and borrowing limits.

B. Why 2026 is a Critical Year for Borrowers and Taxpayers

This combination of expiring tax relief and new loan rules makes 2026 a critical year. Borrowers must understand these updates to avoid unexpected tax bills, often called a “tax bomb,” and to choose the best repayment path. Proactive planning is not just advisable; it is essential. This guide provides actionable strategies to reduce risks and improve financial results.

II. The Return of the “Tax Bomb”: Understanding Forgiveness Taxability in 2026

A. The Expiration of the Temporary Tax Exemption

The American Rescue Plan Act of 2021 (ARPA) provided a temporary federal tax exemption for most student loan forgiveness. This provision covered discharges between December 31, 2020, and January 1, 2026. However, this exemption expired on December 31, 2025. Therefore, any student loan forgiveness processed on or after January 1, 2026, is generally considered taxable income at the federal level. This change primarily impacts borrowers whose loans are forgiven under Income-Driven Repayment (IDR) plans.

B. What Forgiveness is Now Taxable?

Most notably, forgiveness received through Income-Driven Repayment (IDR) plans will generally be taxable. If your lender forgives $600 or more, they are typically required to issue Form 1099-C, Cancellation of Debt. You must report this amount on your federal income tax return. This can significantly increase your taxable income for the year the debt is forgiven.

C. Exceptions to Taxability: What Remains Tax-Free?

While many forms of forgiveness are now taxable, some important exceptions remain:

- Public Service Loan Forgiveness (PSLF): Forgiveness received under PSLF remains explicitly tax-free under IRC Section 108(f)(1). This is a significant benefit for individuals working in public service.

- Insolvency Exclusion: If you are insolvent at the time your debt is forgiven, you may be able to exclude the discharged amount from your income. Insolvency means your total liabilities exceed the fair market value of your assets. You claim this exclusion using IRS Form 982, Reduction of Tax Attributes Due to Discharge of Indebtedness, under IRC Section 108.

- Specific Discharges: Certain administrative discharges, such as those for closed schools or defense to repayment, remain tax-free. These are outlined in guidance like Revenue Procedure 2020-11 and 2015-57.

D. Proactive Strategies to Reduce the “Tax Bomb”

Facing a potential tax bill on forgiven debt requires careful planning. Consider these strategies:

- Financial Modeling: Estimate your potential tax liability in the year your loans are expected to be forgiven. This helps you prepare for the financial impact.

- Income Reduction Strategies: In the year of forgiveness, consider maximizing contributions to pre-tax accounts like a 401(k) or Health Savings Account (HSA). This can reduce your Adjusted Gross Income (AGI), which in turn lowers your taxable income.

- Deduction Optimization: Look for ways to increase your tax deductions. This might include accelerating charitable contributions or other eligible expenses.

- Savings and Estimated Payments: Set aside funds specifically for the anticipated tax bill. Alternatively, you can make estimated tax payments throughout the year of forgiveness to avoid penalties.

- Filing Status Review: Married couples should review their filing status. Sometimes, filing separately can offer advantages, though this requires careful analysis of all tax implications.

- Assessing Insolvency: Determine if you qualify for the insolvency exclusion. Consult a tax professional to evaluate your assets and liabilities.

III. A New Era for Federal Student Loans: Repayment Plans and Borrowing Limits (Effective July 1, 2026)

A. The “Working Families Tax Cuts Act” Overview

The “Working Families Tax Cuts Act” (or “One Big Beautiful Bill Act”) introduces significant changes to federal student loan programs. These updates, effective July 1, 2026, aim to streamline options and adjust borrowing limits. Understanding these student loan changes 2026 is vital for both current and future borrowers.

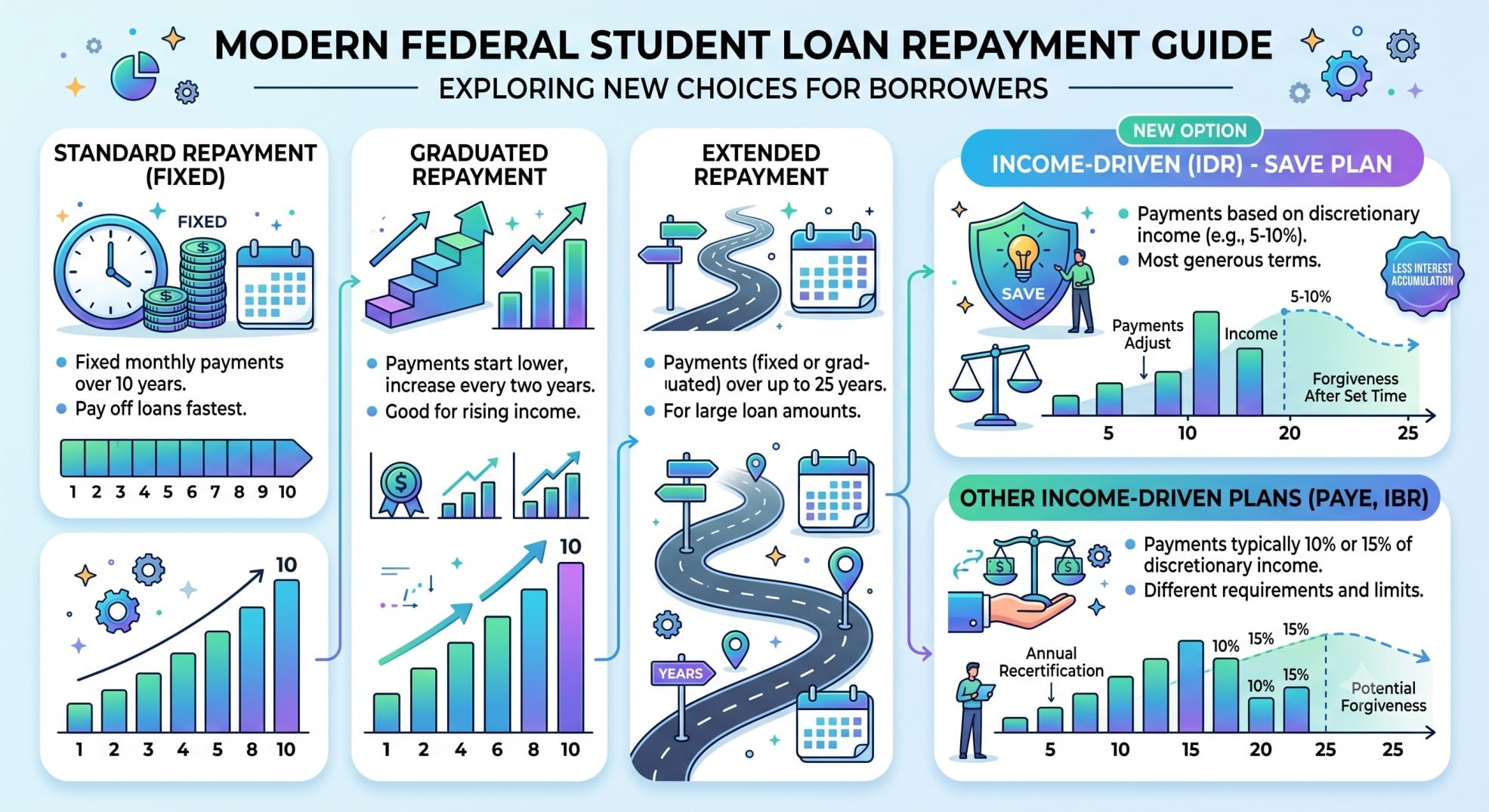

B. Repayment Plan Overhaul for New Loans (Disbursed On or After July 1, 2026)

For new federal loans disbursed on or after July 1, 2026, the existing Income-Driven Repayment (IDR) plans are eliminated. This includes SAVE, PAYE, and ICR. New borrowers will have two primary repayment plans:

- Revised Standard Repayment Plan: This plan will likely offer a fixed monthly payment over a set period.

- Repayment Assistance Plan (RAP): This new plan will offer payment assistance. Importantly, RAP is eligible for Public Service Loan Forgiveness (PSLF).

C. Impact on Existing Borrowers (Loans Disbursed Before July 1, 2026)

Existing borrowers, those with loans disbursed before July 1, 2026, face a different timeline:

- You can continue on your current plans (Standard, Graduated, Extended, IBR). You also have the option to switch to the new Repayment Assistance Plan (RAP).

- Critical Update: Your current SAVE, PAYE, and ICR plans will be phased out by July 1, 2028. This means you will need to transition to an alternative plan, such as the new RAP, before that date.

D. Significant Changes to Loan Limits and Eligibility

The new legislation also introduces important adjustments to borrowing limits:

- Graduate PLUS Loans: These loans are eliminated for new borrowers starting July 1, 2026.

- New Borrowing Caps:

- For graduate degrees, annual limits are $20,500, with a lifetime cap of $100,000.

- For professional degrees, annual limits are $50,000, with a lifetime cap of $200,000.

- Parent PLUS Updates:

- Annual limits are capped at $20,000 per student.

- A lifetime limit of $65,000 per dependent student applies.

- Parent PLUS loans issued on or after July 1, 2026, are not eligible for the new Repayment Assistance Plan (RAP). This impacts their pathway to PSLF.

- Combined Lifetime Borrowing Cap: A total combined lifetime borrowing cap of $257,500 is now in place, excluding Parent PLUS loans.

IV. Student Loan Interest Deduction in 2026

A. IRC Section 221: The “Above-the-Line” Deduction

The student loan interest deduction remains a valuable tax benefit under IRC Section 221. This is an “above-the-line” deduction, meaning it reduces your taxable income regardless of whether you take the standard deduction or itemize. It directly lowers your Adjusted Gross Income (AGI), which can impact eligibility for other tax credits and tax deductions.

B. Key Figures for 2026

For the 2026 tax year, the maximum student loan interest deduction is $2,500. However, this deduction is subject to Modified Adjusted Gross Income (AGI) phase-outs:

- Single Filers: The deduction begins to phase out for those with a MAGI between $75,000 and $90,000. It is eliminated for single filers with a MAGI of $90,000 or more.

- Married Filing Jointly: The deduction begins to phase out for those with a MAGI between $155,000 and $185,000. It is eliminated for joint filers with a MAGI of $185,000 or more.

- Married Filing Separately: Taxpayers filing separately are not eligible for this deduction.

Please note that while these are current estimates for 2026, the IRS may update precise figures. Always consult the latest IRS guidance for the most accurate information, particularly IRS Publication 970, Tax Benefits for Education.

V. Real-World Scenario: Navigating the 2026 Changes

Maria’s Student Loan Journey Through the 2026 Changes

Maria, a 38-year-old single taxpayer, is a social worker earning $65,000 annually. She has $80,000 in federal student loans, all disbursed before July 1, 2026. She is currently enrolled in the SAVE plan, having made consistent payments for 8 years. Her loans are projected to be forgiven under an IDR plan in 2031.

The Impact of 2026 and Beyond:

- Taxability of Forgiveness:

- Pre-2026: Had Maria’s loans been forgiven before January 1, 2026, the amount would have been federally tax-free due to the ARPA exemption.

- Post-2026: Since her forgiveness is projected for 2031, any amount forgiven will generally be considered taxable income at the federal level. If she has $20,000 forgiven, this would be added to her income, potentially pushing her into a higher tax bracket and resulting in a significant tax bill.

- Action: Maria needs to start financial modeling to estimate her potential tax liability in 2031. She should begin saving proactively or explore strategies like increasing 401(k) contributions in the year of forgiveness to reduce her Adjusted Gross Income (AGI). She should also assess her insolvency status closer to the forgiveness date.

- Repayment Plan Changes:

- July 1, 2026: For Maria, as an existing borrower, her current SAVE plan continues. The elimination of IDR plans applies to new loans disbursed on or after this date.

- By July 1, 2028: Her current SAVE plan, along with PAYE and ICR, will be phased out for existing borrowers. Maria will need to transition to an alternative plan. She could switch to the new Repayment Assistance Plan (RAP) or a revised Standard Repayment Plan.

- Action: Maria must monitor communications from her loan servicer and the Department of Education. She should use tools like the EDCAP Calculator to compare potential monthly payments and total costs under RAP versus other available repayment plans well before the 2028 phase-out.

- Student Loan Interest Deduction:

- Maria pays $1,500 in student loan interest annually. With her $65,000 income, her Modified Adjusted Gross Income (AGI) is below the 2026 phase-out threshold for single filers.

- Benefit: She can continue to claim the full $1,500 in tax deductions for student loan interest, reducing her taxable income.

- Action: Maria should ensure she receives Form 1098-E from her loan servicer and accurately claims this “above-the-line” deduction on her tax return.

Summary for Maria: While Maria’s SAVE plan isn’t ending immediately in July 2026, she faces a critical future decision regarding her repayment plan by July 1, 2028, and a significant potential tax liability upon forgiveness in 2031. Proactive planning and understanding these staggered student loan changes 2026 are essential for her financial well-being.

VI. Next Steps for Taxpayers & Borrowers

The upcoming student loan changes 2026 require proactive action. Here are concrete steps you can take:

- Verify Your Details: Log into your Federal Student Aid account at StudentAid.gov. Confirm your loan types, balances, and current repayment plans.

- Evaluate Alternatives: Use online calculators, like those offered by EDCAP, to compare potential monthly payments and total costs under different repayment plans, including the new RAP.

- Beware of Consolidation Risks: Consolidating your loans can sometimes reset your progress toward forgiveness under IDR or PSLF. Understand these implications before making any consolidation decisions.

- Consult a Professional: Tax laws and student loan regulations are complex. Seek personalized advice from a qualified tax professional or financial advisor. They can help you understand your specific situation and optimize your tax deductions.

VII. Conclusion: Taking Control of Your Financial Future

The year 2026 brings significant student loan changes 2026 that will affect millions of borrowers. From the return of federal taxability for most forgiveness to a complete overhaul of federal repayment plans, these updates require your attention. Understanding these shifts and planning proactively can help you reduce risks and make informed decisions about your financial future. Do not wait; take control with knowledge and seek expert guidance to navigate these important changes successfully.

Disclaimer: This information provides general guidance and should not be considered personalized tax or financial advice. Individual circumstances vary, and you should consult with a qualified tax professional or financial advisor for guidance tailored to your specific situation. Tax laws and regulations are subject to change. While this document reflects the most current information available as of June 27, 2026, future legislative or regulatory actions could alter these provisions. Always refer to official IRS publications and the Department of Education’s student aid website for the most definitive and up-to-date information.