As you enjoy your golden years, understanding your tax options can lead to significant savings. For 2026, new rules and timeless strategies offer unique opportunities for individuals over 65 to boost their tax refunds. This guide will help you understand how to maximize refund for 2026. We will explore how you can keep more of your hard-earned money through smart tax planning for older adults.

Executive Summary

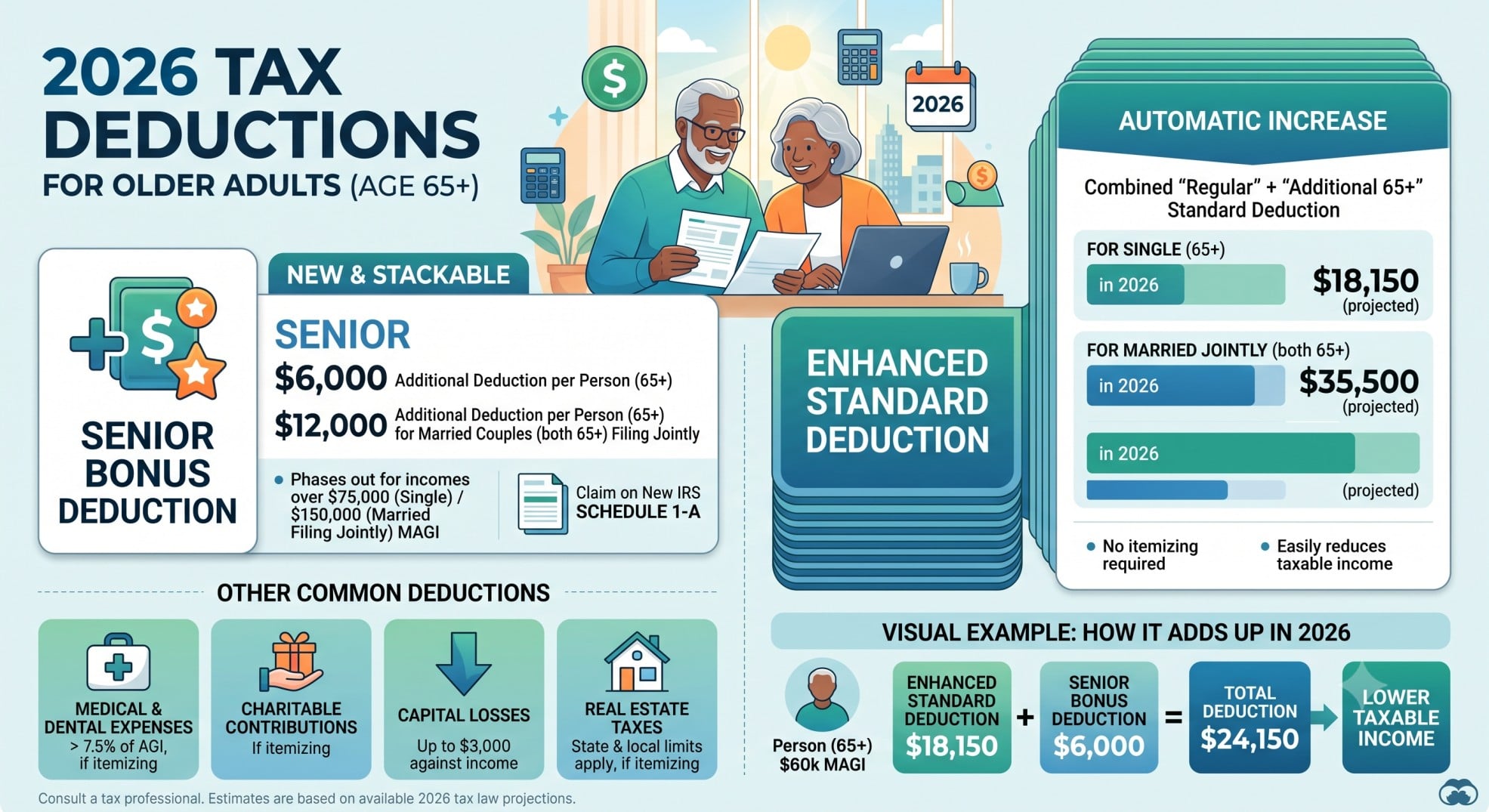

- The standard deduction for individuals over 65 is enhanced for 2026.

- A new temporary “senior bonus deduction” can further reduce taxable income.

- Qualified Charitable Distributions (QCDs) reduce taxable income and satisfy RMDs.

- Managing your Adjusted Gross Income (AGI) can lower your tax bill.

- Proactive tax planning is key to significant savings.

Understanding Your Foundation: Key Deductions for Older Adults in 2026

Knowing your available deductions is the first step to reducing your tax liability. Understanding these options is important for individuals over 65.

The Enhanced Standard Deduction

For 2026, the standard deduction amounts are as follows: Married couples filing jointly can claim $32,200. Single filers can claim $16,100. Heads of household can claim $24,150. Individuals over 65 or who are blind receive an additional standard deduction. This amount is $1,650 per qualifying individual for married couples filing jointly or separately. It is $2,050 for single filers and heads of household. For instance, a single filer who is both 65 and blind gets an extra $4,100.

A new temporary “senior bonus deduction” is also available for 2026. This adds $6,000 for individuals aged 65 and older. It adds $12,000 for married couples filing jointly if both are 65 or older. However, this bonus deduction phases out for higher earners. It begins for single filers with modified AGI over $75,000. It also phases out for married couples with modified AGI over $150,000. Always compare your total itemized deductions against your standard deduction. Choose the option that gives you the largest tax benefit to maximize refund.

Medical Expense Deduction

You can deduct unreimbursed medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI). This threshold was made permanent. IRS Publication 502 details eligible expenses. These can include doctor visits, prescription medications, and even certain long-term care services. Qualified long-term care insurance premiums can also be treated as medical expenses. These are subject to age-based limits and the 7.5% AGI threshold. A new rule for 2026 allows penalty-free withdrawals of up to $2,600 annually from certain retirement plans. These withdrawals can pay for long-term care insurance premiums, avoiding the 10% early-withdrawal penalty.

Non-Itemizer Charitable Deduction

Starting in 2026, individuals who do not itemize can still deduct cash donations. This new deduction allows up to $1,000 for single filers. It allows up to $2,000 for joint filers. These donations must go to qualified charities. However, they exclude donor-advised funds and private foundations. This offers a new way to get a tax break for your generosity.

Smart Strategies for Managing Retirement Income

Effective tax planning for older adults involves carefully managing your retirement income. This helps reduce your overall tax burden. Understanding these strategies is important.

Qualified Charitable Distributions (QCDs): A Powerful Tool

Qualified Charitable Distributions (QCDs) are a powerful tool for individuals aged 70½ or older. A QCD is a direct transfer of funds from your IRA to an eligible charity. These distributions count towards satisfying your RMDs. They are also excluded from your taxable income. The indexed annual limit for QCDs is $111,000 per taxpayer for 2026. Using QCDs can significantly reduce your Adjusted Gross Income (AGI). A lower AGI can impact many other tax calculations. For example, it can reduce Medicare premiums and the Net Investment Income Tax (NIIT).

Navigating Required Minimum Distributions (RMDs)

Required Minimum Distributions (RMDs) are mandatory withdrawals from most tax-deferred retirement accounts. These include traditional IRAs and 401(k)s. The SECURE 2.0 Act raised the RMD starting age. It is now 73 for individuals born between 1951 and 1959. It is 75 for those born in 1960 or later. Making timely withdrawals is important to avoid penalties. Consider Roth conversions as a long-term strategy. These can reduce future RMDs. This can also help manage your taxable income in retirement.

Understanding Social Security Benefit Taxation

A portion of your Social Security benefits may be taxable. This depends on your “combined income.” Combined income includes your AGI, tax-exempt interest, and one-half of your Social Security benefits. For married couples filing jointly, benefits become partially taxable when combined income exceeds $32,000. Up to 85% can be taxable above $44,000. Managing your AGI, perhaps with QCDs, can reduce the taxable portion of your Social Security benefits. This is a key aspect of tax planning for older adults.

Real-World Impact: John and Mary’s 2026 Tax Planning Case Study

Let’s look at a real-world example. This case study demonstrates how strategic tax planning can lead to significant savings. John and Mary, both 70, are a married couple in California. They are retired and want to improve their 2026 tax situation.

Case Study: John and Mary’s 2026 Tax Planning

John and Mary, both 70 years old, are a married couple living in California. They are retired and looking for ways to improve their tax situation for 2026. Their financial profile includes a mix of retirement and investment income, along with significant medical and charitable expenses.

Their Financial Snapshot (Before Planning):

- Social Security Benefits: $60,000

- Pension Income: $80,000

- IRA Distributions (Required Minimum Distributions – RMDs): $50,000

- Investment Income: $70,000 (comprising $20,000 in qualified dividends/long-term capital gains and $50,000 in ordinary interest/short-term capital gains)

- Unreimbursed Medical Expenses: $25,000

- Property Taxes: $12,000

- Cash Charitable Contributions: $10,000

Scenario 1: Without Strategic Tax Planning

In this scenario, John and Mary take their IRA distributions as taxable income. They also make their charitable contributions in cash.

Key Calculations:

- Adjusted Gross Income (AGI): $251,000.00

- Federal Standard Deduction (MFJ, both 65+): $35,500.00 (They use the standard deduction as it’s higher than their itemized deductions of $26,175.00. The senior bonus deduction is phased out due to their AGI.)

- Federal Taxable Income: $215,500.00

- Total Federal Income Tax: $35,510.80

- Net Investment Income Tax (NIIT): $38.00 (triggered because their AGI slightly exceeds the $250,000 threshold for MFJ).

- California State Income Tax: $13,525.83 (Calculated based on their CA AGI of $251,000.00 and CA itemized deductions of $28,175.00.)

- Alternative Minimum Tax (AMT): $0.00

- Total Tax Liability: $49,074.63

Scenario 2: Implementing a Qualified Charitable Distribution (QCD) Strategy

John and Mary learn about Qualified Charitable Distributions. Since they are over 70.5 years old and taking RMDs, they decide to make their $10,000 charitable contribution directly from their IRA to a qualified charity. This reduces their taxable IRA distribution.

Key Calculations:

- IRA Distributions (Taxable): $40,000.00 (Reduced by $10,000 QCD)

- Adjusted Gross Income (AGI): $241,000.00 (Reduced by $10,000 due to the QCD)

- Federal Standard Deduction (MFJ, both 65+): $35,500.00 (Still higher than their new itemized deductions of $16,925.00. The senior bonus deduction is still phased out due to their AGI.)

- Federal Taxable Income: $205,500.00

- Total Federal Income Tax: $33,310.80

- Net Investment Income Tax (NIIT): $0.00 (Their AGI is now below the $250,000 threshold, eliminating the NIIT).

- California State Income Tax: $13,452.28 (Calculated based on their reduced CA AGI of $241,000.00 and CA itemized deductions of $18,925.00).

- Alternative Minimum Tax (AMT): $0.00

- Total Tax Liability: $46,763.08

The Power of Strategic Planning: Key Takeaways

By implementing a Qualified Charitable Distribution strategy, John and Mary significantly reduced their overall tax burden.

- Total Tax Savings: $2,311.55

- Federal Tax Savings: $2,200.00

- NIIT Savings: $38.00

- California State Tax Savings: $73.55

This case study highlights how a simple strategy like a QCD can lead to substantial tax savings for individuals over 65. By reducing their Adjusted Gross Income (AGI), they not only lowered their federal income tax but also avoided the Net Investment Income Tax. This also lowered the AGI threshold for medical expense deductions, making it easier to deduct more. Therefore, it led to a higher refund. Older adults should always explore options that reduce AGI. It impacts many tax calculations and thresholds. This is a clear example of how to maximize refund for 2026.

Proactive Planning for a Secure Financial Future

Tax planning is not a one-time event. It requires ongoing attention. Regularly review your financial situation and tax strategies. This ensures you are always using available benefits. For instance, new rules may emerge. Your personal circumstances may also change. Consulting with a qualified tax professional is highly recommended. They can provide personalized advice. This helps you understand the complexities of tax law. This is especially true for individuals over 65.

Conclusion

Understanding and using available tax strategies is very important. For 2026, individuals over 65 have several opportunities to reduce their tax burden and maximize refund. From enhanced standard deductions to strategic use of QCDs and careful management of RMDs, proactive tax planning can make a real difference. Take control of your financial future. Stay informed. Seek expert guidance. You can keep more of your hard-earned money.

For more detailed information, please refer to official sources like the IRS website.