The 2025 tax year brings specific challenges and opportunities for Trust, Estate, and Beneficiary K-1s. More than just compliance, understanding the reporting rules and strategic implications is key. This guide offers strategies for accurate 2025 tax reporting and effective planning. Are you ready for the complexities of Distributable Net Income, the Net Investment Income Tax, and state and local taxes? This article provides the strategies you need to report correctly and plan effectively for the 2025 tax year.

Executive Summary

- Trusts and estates face highly compressed tax brackets in 2025, reaching the top 37% federal rate on income over $15,650.

- Accurate DNI calculation is essential; it limits the income distribution deduction for the trust and the amount taxable to beneficiaries.

- The 3.8% NIIT for trusts applies to undistributed net investment income exceeding $15,650.

- The Qualified Business Income (QBI) deduction (Section 199A) is now permanent, offering potential savings for trusts and beneficiaries.

- State and local taxes (SALT) significantly impact trust income and beneficiary K-1s, especially with the federal $10,000 individual deduction limit.

- The federal estate and gift tax exemption is $13.99 million per individual for 2025, increasing to $15 million in 2026 due to new legislation.

Introduction: Understanding 2025 Trust and Estate Taxation

Why 2025 K-1 Reporting Needs Careful Strategies

For corporate principals and fiduciaries, the stakes for Trust, Estate, and Beneficiary K-1s are high. Trusts and estates operate under highly compressed tax brackets, meaning they reach the highest federal income tax rates at much lower income levels than individuals. The interplay of federal and state tax rules also adds layers of complexity. Therefore, precise 2025 tax reporting is not just about compliance; it is about strategic wealth preservation.

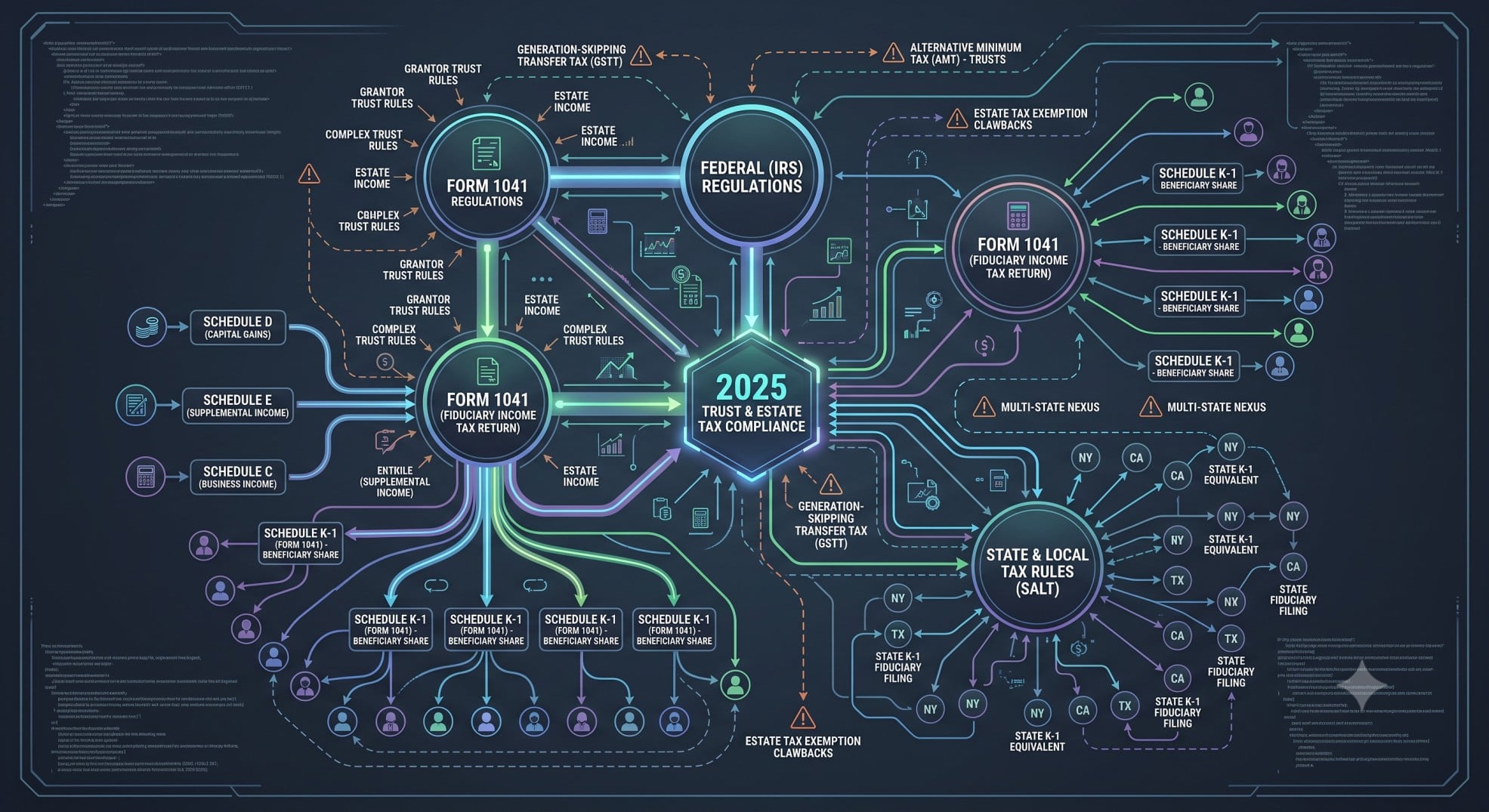

The Importance of Schedule K-1 (Form 1041)

Schedule K-1 (Form 1041) is a key communication tool. Fiduciaries use it to report a beneficiary’s share of income, deductions, credits, and other items from an estate or trust. Beneficiaries then use this information to complete their individual income tax returns (Form 1040 or 1040-SR). Accurate K-1 preparation is essential for both parties.

Key Principles: Understanding Trust and Estate Tax Law

Key Internal Revenue Code (IRC) Sections Governing Trusts and Estates

Subchapter J of the Internal Revenue Code (IRC) governs the taxation of trusts and estates. Several sections are particularly relevant for Trust, Estate, and Beneficiary K-1s:

- IRC 641: This section imposes income tax on the taxable income of estates and trusts.

- IRC 642: It addresses special rules for credits and deductions, including the deduction for distributions to beneficiaries and the treatment of excess deductions on termination (IRC 642(h)).

- IRC 651/652: These sections apply to simple trusts, which must distribute all income currently and do not distribute principal.

- IRC 661/662: These sections govern complex trusts and estates, which may accumulate income or distribute principal. They establish the Distributable Net Income (DNI) concept.

- IRC 671-679: These sections define Grantor Trusts. For tax purposes, the grantor (or another person) owns the trust assets. Grantor trusts typically do not file Form 1041 or issue K-1s for the grantor portion.

- IRC 199A: This section permits a Qualified Business Income (QBI) deduction for certain trusts and estates, which can pass through to beneficiaries.

- IRC 67(e) and 67(g): These sections relate to miscellaneous itemized deductions. While IRC 67(g) suspended most miscellaneous itemized deductions for individuals through 2025, IRC 67(e) allows trusts and estates to deduct certain administrative expenses.

Distributable Net Income (DNI): Central to K-1 Reporting

Distributable Net Income (DNI) is a central concept for K-1 reporting. It limits the income distribution deduction for the trust or estate. Furthermore, it caps the amount taxable to beneficiaries. DNI calculation involves starting with taxable income and making specific adjustments, such as adding back tax-exempt interest and capital gains allocated to principal. The character of income (ordinary, capital gains, tax-exempt) also remains important as it flows through to beneficiaries.

Essential IRS Forms and Publications for 2025

Accurate 2025 tax reporting relies on specific IRS forms and publications:

- Form 1041, U.S. Income Tax Return for Estates and Trusts: This is the primary return filed by the fiduciary of a domestic estate or trust.

- Schedule K-1 (Form 1041), Beneficiary’s Share of Income, Deductions, Credits, etc.: Fiduciaries issue this form to each beneficiary. It reports their share of the estate’s or trust’s financial items.

- Instructions for Form 1041 and Schedules A, B, G, J, and K-1 (2025): These instructions provide detailed guidance for preparing Form 1041 and its accompanying schedules.

- Instructions for Schedule K-1 (Form 1041) for a Beneficiary Filing Form 1040 or 1040-SR (2025): This publication specifically guides beneficiaries on reporting K-1 items on their personal returns.

- Publication 559, Survivors, Executors, and Administrators (2025): This publication offers comprehensive information for personal representatives of decedents’ estates, including filing requirements for Form 1041 and K-1s.

Strategies for Better 2025 K-1 Reporting

Strategic Income Distribution: Balancing Trust and Beneficiary Tax Rates

Trusts and estates face highly compressed income tax rates in 2025. For example, the top 37% federal rate applies to income over $15,650. Fiduciaries must carefully analyze whether to distribute income to beneficiaries or keep it within the trust. Distributing income can shift the tax burden to beneficiaries, who often have lower individual tax rates. This strategy requires careful consideration of each beneficiary’s tax situation.

Understanding the Net Investment Income Tax (NIIT) for Trusts and Beneficiaries

The 3.8% Net Investment Income Tax (NIIT) applies to the lesser of undistributed net investment income or the amount by which an estate’s or trust’s adjusted gross income (AGI) exceeds $15,650 in 2025. Certain trusts, such as grantor trusts, are exempt. Strategies to mitigate NIIT for trusts include making timely distributions to beneficiaries or structuring investment choices to reduce net investment income. This tax notably impacts overall trust profitability.

Qualified Business Income (QBI) Deduction (Section 199A) for Trusts and Estates

The Qualified Business Income (QBI) deduction, originally set to expire, has been made permanent by the “One Big Beautiful Bill Act” (OBBBA). This allows eligible individuals, and certain trusts and estates, to deduct up to 20% of their qualified business income. For 2025, income thresholds apply, and the deduction may be limited or phased out for specified service trades or businesses (SSTBs). The QBI deduction can pass to beneficiaries through K-1s, offering notable tax savings. However, passive QBI without related wages or property basis needs careful review.

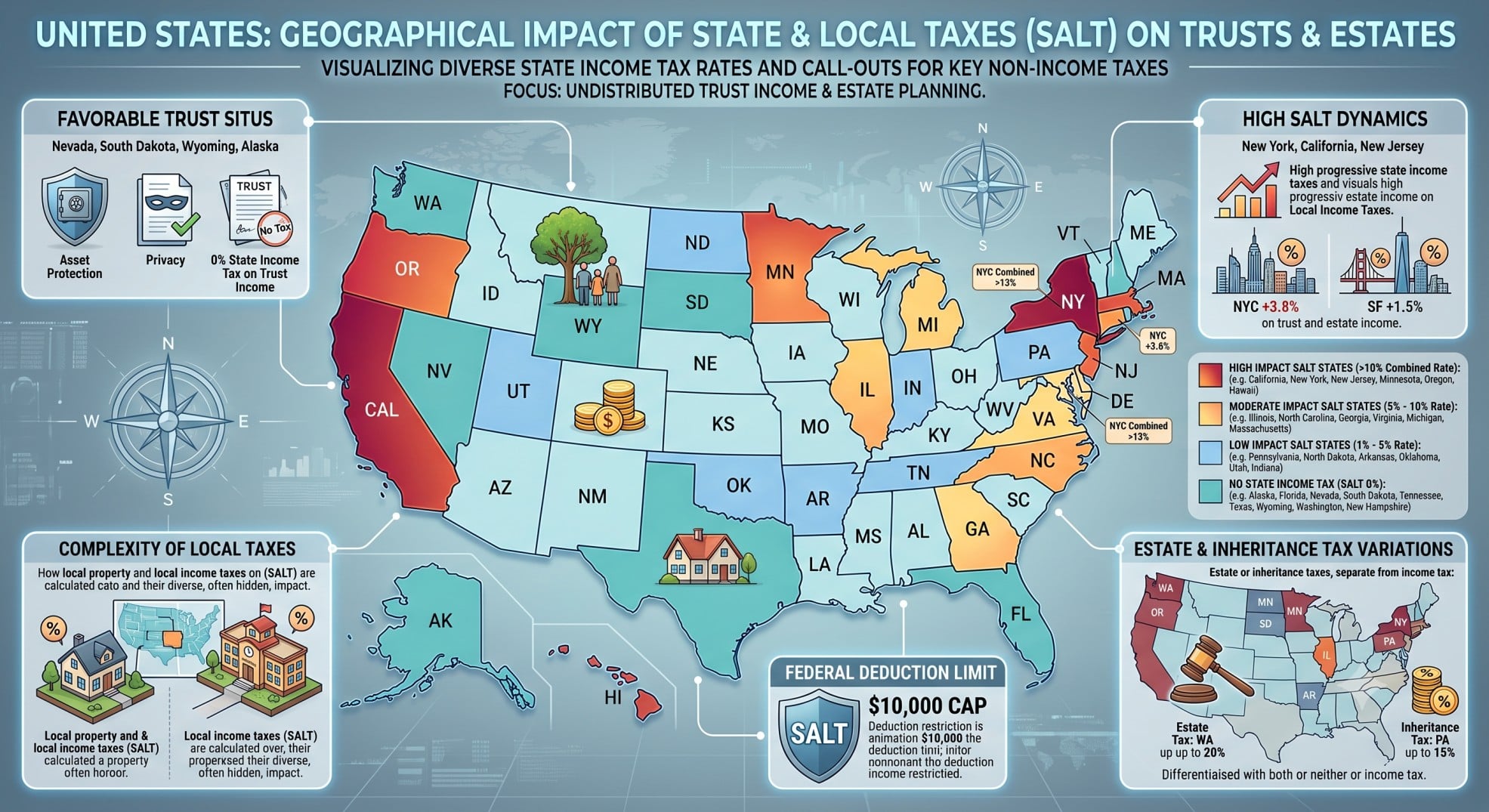

The Impact of State and Local Taxes (SALT) on Trust and Beneficiary K-1s

State and local taxes (SALT) significantly affect Trust, Estate, and Beneficiary K-1s. The federal $10,000 SALT deduction limitation for individuals remains in effect. State income taxes paid by the trust reduce its Distributable Net Income (DNI). However, state-specific rules vary widely. For instance, California has high state income tax rates and does not offer a state-level SALT cap workaround or QBI deduction. Some states allow Pass-Through Entity (PTE) taxes, which can provide a federal deduction workaround for the SALT cap if applicable to trusts or estates in those states. Therefore, fiduciaries must understand state-specific tax implications.

Alternative Minimum Tax (AMT) Considerations for High-Income Beneficiaries

K-1 income can trigger or increase the Alternative Minimum Tax (AMT) for high-income beneficiaries. Common AMT adjustments include state and local taxes. Fiduciaries should model potential AMT exposure for beneficiaries when planning distributions. Strategies to minimize AMT exposure often involve careful timing and characterization of income distributions. This needs early planning.

Excess Deductions on Termination (IRC 642(h)(2) and 67(g))

When an estate or trust terminates, any excess deductions can pass to beneficiaries. The Tax Cuts and Jobs Act (TCJA) suspended most miscellaneous itemized deductions subject to the 2% floor for individuals through 2025. However, Notice 2018-61 and Final Regulations (TD 9918) clarify that certain administrative expenses of trusts and estates are not subject to this suspension. These regulations confirm that each excess deduction retains its character when passed to beneficiaries. Beneficiaries can potentially deduct these expenses on their individual returns, subject to their own limitations.