Table of Contents

- What Is the “IRS COVID Refund Loophole” for General Taxpayers?

- Step-by-Step: How to File a Protective Claim for Refund (Form 843)

- Real-World Scenario: Maria’s Penalty Refund Opportunity

- Distinguishing From the Employee Retention Credit (ERC)

- The Unsettled Legal Situation: What to Expect

- General Tax Planning for 2026: Beyond the Refund Loophole

- Consult a Tax Professional: Understanding the Complexity

Did you pay IRS penalties or interest between January 20, 2020, and July 10, 2023? A recent federal court decision, Kwong v. United States, opened a narrow, time-sensitive window for general taxpayers to reclaim those funds.

This opportunity centers on what’s now being called the IRS COVID refund loophole, and it demands action. You have until the critical July 10, 2026 deadline to protect your claim, or you risk losing the chance forever. This guide walks you through the opportunity, what it means for your wallet, and how to file a protective claim using Form 843 to lock in your rights. This information is current as of July 8, 2026.

⚡ Executive Summary: Key Takeaways for General Taxpayers

- A federal court decision, Kwong v. United States, may let taxpayers reclaim certain penalties and interest paid during the COVID-19 pandemic.

- This applies to penalties and interest assessed for tax obligations originally due between January 20, 2020, and July 10, 2023.

- You must file a protective claim using Form 843 by July 10, 2026.

- The IRS is appealing the Kwong decision, so refunds aren’t guaranteed, but filing protects your right to one.

- This opportunity is completely separate from the Employee Retention Credit (ERC).

- A qualified tax professional can help you confirm eligibility and prepare your claim correctly.

Many general taxpayers hit financial roadblocks during the COVID-19 pandemic. Some ended up with penalties or interest charges from the IRS during that stretch. The Kwong v. United States ruling has now created a unique, time-limited opening. It suggests that certain tax deadlines during the pandemic were effectively pushed back, which means the penalties and interest assessed during that window might be refundable.

Nothing new is being credited here. Instead, you’re being given a shot at reclaiming money you already handed over. The July 10, 2026 deadline is closing in fast, and missing it means forfeiting your right to a potential refund permanently. This guide breaks down the IRS COVID refund loophole and lays out exactly what you need to do next.

What Is the “IRS COVID Refund Loophole” for General Taxpayers?

The term “IRS COVID refund loophole” describes a specific legal interpretation that allows taxpayers to seek refunds for certain penalties and interest assessed by the IRS during the pandemic. This opportunity comes from a federal court decision, not from new legislation.

Understanding the Kwong Decision and IRC Section 7508A(d)

The Kwong v. United States decision, handed down in late 2025, sits at the center of this opportunity. The ruling treated the COVID-19 period as a federally declared disaster under Internal Revenue Code (IRC) Section 7508A(d), a provision that allows the IRS to postpone certain tax deadlines during disasters.

The court found that certain deadlines were effectively postponed to July 10, 2023. That means the IRS arguably shouldn’t have assessed penalties or interest for obligations due during this window. This decision directly impacts the three-year statute of limitations for refunds.

The Critical July 10, 2026, Deadline Explained

The July 10, 2026 deadline marks exactly three years from July 10, 2023, the date the Kwong decision treated as the postponed due date for many COVID-era tax obligations. Under IRC Section 6511, taxpayers generally get three years from the date a return was filed, or two years from the date the tax was paid, whichever is later, to claim a refund.

This particular deadline applies to protective claims, the filings that preserve your right to a refund. Act before this date, or the opportunity disappears.

Who Is Eligible? Identifying Affected Penalties and Interest

This opportunity reaches a broad swath of taxpayers, including individuals, businesses, estates, and trusts. It covers penalties and interest for obligations originally due between January 20, 2020, and July 10, 2023.

Late filing penalties under IRC Section 6651(a)(1) fall under this umbrella. Late payment penalties under IRC Section 6651(a)(2) do too. Penalties for failure to make estimated tax payments under IRC Section 6654 also qualify. Comb through your records carefully to spot any of these assessments.

Step-by-Step: How to File a Protective Claim for Refund (Form 843)

Filing a protective claim matters. It’s the single action that preserves your right to a refund. Here’s how to submit Form 843.

Review Your Records: Identifying Penalties and Interest

Start by gathering every relevant tax document you have. Check your IRS transcripts, notices such as CP14, CP16, and CP210, along with your tax software records. Look specifically for penalties or interest assessed between January 20, 2020, and July 10, 2023. These are the amounts potentially refundable under the IRS COVID refund loophole.

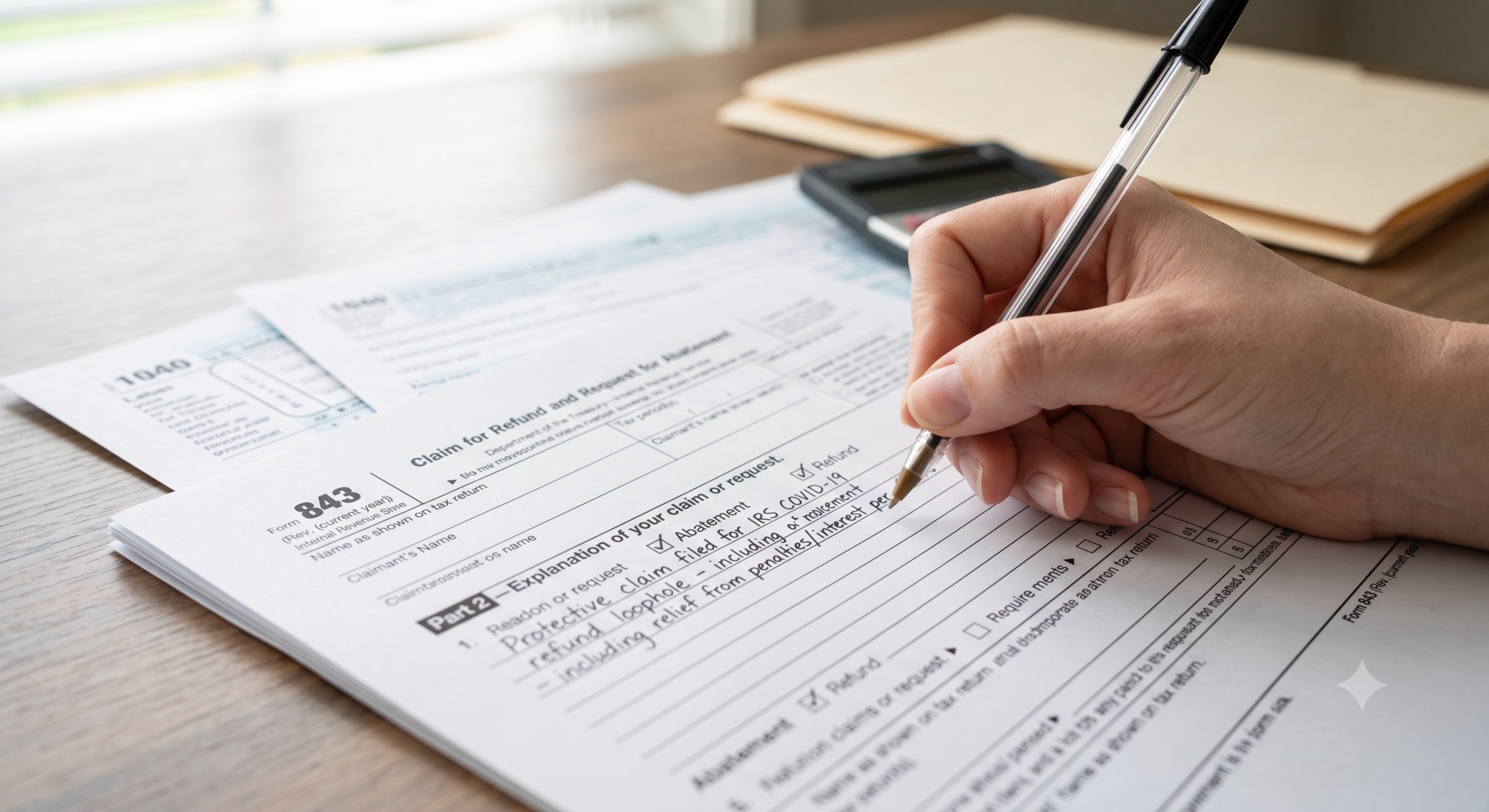

Completing Form 843, Claim for Refund and Request for Abatement

Use Form 843, Claim for Refund and Request for Abatement, and fill it out completely. Box 7, labeled “Explanation,” deserves special attention here.

Reference the Kwong decision directly in that box. State that the penalties and interest were assessed for a period covered by the ruling, and cite IRC Section 7508A(d). Note that the IRS recently rolled out an online option for eligible individuals, letting you submit Form 843 electronically through your IRS Online Account for fully paid interest and penalties.

What to Include With Your Claim

Attach copies of every supporting document you can find. This includes IRS notices, proof of penalty and interest payments, and any related correspondence. Solid documentation strengthens your claim considerably.

Where to Mail Your Form 843

Mailing addresses for Form 843 vary depending on your location. Always check IRS.gov for the most current instructions to make sure your claim lands with the correct department.

The Importance of a Protective Claim

A protective claim is crucial precisely because the Kwong decision is still under appeal.

Refunds aren’t guaranteed, and the process may take time. But a protective claim keeps you eligible if the decision holds up on appeal. Skipping the July 10, 2026 deadline closes that door for good.

Real-World Scenario: Maria’s Penalty Refund Opportunity

Maria, a self-employed graphic designer, files her taxes as an individual. A family emergency in 2021 kept her from filing her 2020 federal income tax return (Form 1040) by the extended deadline of October 15, 2021. She eventually filed on December 1, 2021.

Because of the late filing, the IRS assessed a late filing penalty under IRC Section 6651(a)(1), plus interest on the underpayment of tax running from April 15, 2021, until the payment date. Maria paid these amounts in January 2022.

Financial Breakdown

- Original Tax Due (2020): $12,000

- Late Filing Penalty: $600 (assessed for late filing)

- Interest on Underpayment: $150

- Total Penalties & Interest Paid: $750

How the Kwong Decision Applies to Maria

The Kwong v. United States decision determined that the COVID-19 period, January 20, 2020, to July 10, 2023, qualified as a federally declared disaster. Certain tax deadlines during this stretch were effectively postponed to July 10, 2023.

Maria’s 2020 tax return had an original due date of April 15, 2021, which falls squarely within this disaster period. The Kwong ruling suggests the IRS shouldn’t have assessed penalties or interest for obligations due during this time, since the effective due date was postponed.

Maria’s Opportunity

Maria paid $750 in penalties and interest in January 2022 for her 2020 tax year, a payment that landed after January 20, 2020, and before July 10, 2023. That timing makes her a prime candidate for this IRS COVID refund loophole.

To preserve her right to reclaim that $750, Maria needs to file Form 843 by July 10, 2026. On the form, she’d explain that the penalties and interest were assessed for a period covered by the Kwong decision, which deemed the COVID-19 period a disaster under IRC Section 7508A(d) and effectively postponed her tax deadlines.

Outcome

Filing Form 843 by the deadline protects Maria’s claim. If the Kwong decision survives its appeal, she could receive a refund of the $750 she paid. Miss the July 10, 2026 deadline, though, and she loses this opportunity permanently, no matter how the appeal turns out.

Distinguishing From the Employee Retention Credit (ERC)

This IRS COVID refund loophole for penalties and interest has nothing to do with the Employee Retention Credit. Both relate to the pandemic, but they’re entirely separate programs with their own rules and deadlines.

Why This Isn’t the ERC

The ERC was a refundable tax credit designed for businesses, meant to encourage them to keep employees on payroll during the pandemic. This penalty and interest opportunity addresses specific IRS assessments instead and doesn’t involve employer credits at all. Keep the two straight.

Key Differences and ERC Deadlines (Mostly Closed)

New ERC claims are largely closed at this point. The deadline for most claims was January 31, 2024, while some 2021 claims had a deadline of April 15, 2025.

The “One Big Beautiful Bill Act” (OBBBA), signed on July 4, 2025, extended the IRS’s audit period for ERC claims to six years under IRC Section 3134(l). The IRS also imposed a moratorium on processing new ERC claims back in September 2023 (IR-2023-169, IR-2023-171), and it offered withdrawal options along with voluntary disclosure programs, such as Notice 2023-21 and Announcement 2024-30, both now closed. A revised Form 941-X came out in April 2026.

ERC Litigation and Enforcement: A Word of Caution

IRS enforcement against fraudulent ERC claims continues aggressively. As of February 2025, IRS Criminal Investigation had opened more than 2,039 cases tied to COVID-19 relief fraud.

Taxpayers whose ERC claims get disallowed face a strict two-year deadline to resolve the matter administratively or file suit. The IRS also introduced Form 907, which lets certain taxpayers request an extension of that two-year window.

The Unsettled Legal Situation: What to Expect

The legal ground beneath the Kwong decision remains shaky. Understanding this context matters for any general taxpayer weighing whether to file.

The Government’s Appeal of Kwong

The U.S. government, including the Treasury Department and the IRS, is appealing the Kwong decision, arguing the ruling misreads the relevant statute.

This appeal adds a layer of uncertainty, which makes filing protective claims by the July 10, 2026 deadline even more essential. It’s the one move that safeguards your potential refund no matter which way the appeal goes.

The Role of the National Taxpayer Advocate

The National Taxpayer Advocate (NTA), an independent voice within the IRS, has consistently advised taxpayers to file protective claims. That guidance underscores why acting now matters: it keeps your rights intact regardless of how the appeal resolves.

Potential Outcomes and Timelines

The legal process for the Kwong appeal could stretch on for years. Should the government lose, the IRS will likely process valid claims. Should the government win, claims will likely be denied. That uncertainty is exactly why a protective claim makes sense for any general taxpayer in this position.

General Tax Planning for 2026: Beyond the Refund Loophole

The IRS COVID refund loophole is time-sensitive, but broader tax planning 2026 considerations deserve your attention too. Tax law never stops shifting, so planning ahead pays off.

Impact of TCJA Sunsetting Provisions on 2026 Taxes

Many individual tax provisions from the Tax Cuts and Jobs Act (TCJA) are set to expire after 2025, and that will significantly reshape tax planning 2026. Standard Deduction thresholds, for instance, may drop, which means more taxpayers might start considering Itemized Deductions instead. Other expiring provisions could also affect your overall tax liability, so check IRS Standard Deduction Guidelines for current figures.

| Filing Status | 2025 Standard Deduction (Estimated) | 2026 Standard Deduction (Post-TCJA Sunset, Estimated) |

|---|---|---|

| Single | $14,600 | $7,300 |

| Married Filing Separately | $14,600 | $7,300 |

| Married Filing Jointly | $29,200 | $14,600 |

| Head of Household | $21,900 | $10,950 |

Note: These are estimated figures based on current law and inflation projections. Actual amounts may vary.

Proactive Steps for 2026 Tax Season

Review your withholding and estimated payments now to avoid unpleasant surprises later. Factor in the potential tax law changes ahead, and adjust your tax planning 2026 strategy accordingly as you prepare for the upcoming season.

Consult a Tax Professional: Understanding the Complexity

Tax law shifts constantly, and the situation surrounding the IRS COVID refund loophole is especially tangled given the unsettled legal questions involved. Getting expert advice is strongly worth it here.

A qualified tax professional can assess your specific situation, help determine your eligibility, and assist with preparing and filing Form 843 accurately. That kind of guidance goes a long way toward making sure your claim holds up.

Don’t Miss Your Chance: Act by July 10, 2026

The opportunity to reclaim COVID-era penalties and interest is real, but it’s also brief. The July 10, 2026 deadline is firm, and missing it means losing your chance for good.

File a protective Form 843 now to preserve your rights. Don’t delay this, since acting today is what puts you in position to benefit from the IRS COVID refund loophole.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.