Table of Contents

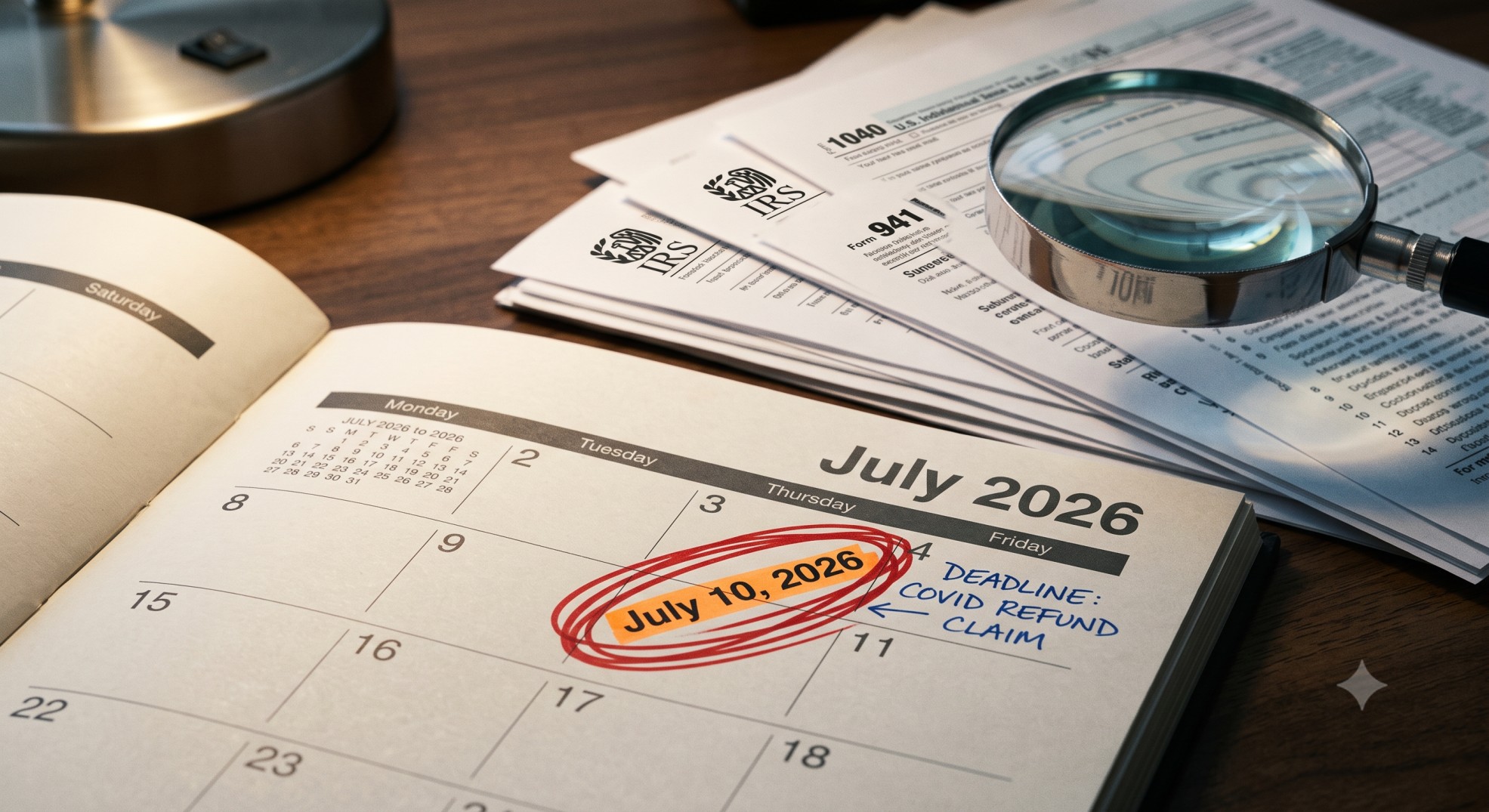

A quiet deadline is sitting on the calendar for July 10, 2026 — and it could put real money back in your pocket. Far off as that date sounds, it matters a great deal if you paid penalties or interest to the IRS during the pandemic years.

Missing it means losing a shot at a refund you may not even know you’re entitled to. A “protective claim” filed now can keep that door open. This article walks through five practical tips so you understand what these tax deadlines 2026 mean for you and how potential IRS COVID refunds actually work.

⚡ Executive Summary: What You Need to Know

- July 10, 2026 is a firm deadline. File a protective claim by this date to preserve potential refunds for COVID-era penalties and interest.

- The Kwong case triggered this window. A court ruled many COVID-era penalties were improperly assessed. The IRS is appealing.

- A protective claim locks in your rights. It keeps your refund option alive if the Kwong ruling ultimately stands.

- Form 843 is the correct paperwork. Use it specifically to claim these penalties and interest.

- This has nothing to do with ERC. The deadline is entirely separate from Employee Retention Credit claims.

- A tax professional should review your case. Tax law here is nuanced, and personalized advice matters.

Tip 1: Understand the Reason Behind the July 10, 2026 Deadline

The Kwong Case and Its Impact

Kwong v. United States (179 Fed. Cl. 382) is the court decision driving this entire situation. The ruling interpreted Internal Revenue Code Section 7508A(d) and found that federal tax filing and payment deadlines were automatically postponed during the COVID-19 disaster period, which ran from January 20, 2020, through July 10, 2023.

Penalties and interest the IRS assessed for supposedly late filings or payments during that window may now qualify for a refund. That’s the direct result of this case.

An appeal from the IRS is currently underway, so nothing is settled yet. Filing a protective claim now protects your right to a refund if the ruling survives that appeal. Keep in mind this deadline covers penalties and interest only — it has no bearing on new Employee Retention Credit (ERC) claims.

The Statute of Limitations and Your Refund Rights

Three years is the general window for claiming a tax refund, counted from the date you filed your original return. Two years from the date you paid the tax works as an alternative measure, whichever lands later. IRC Section 6511(a) sets this baseline rule.

The Kwong ruling effectively pushes that window out for certain COVID-era penalties and interest by treating the due date for affected returns as July 10, 2023. That’s the math behind why July 10, 2026 becomes the three-year cutoff for many of these claims — and why these tax deadlines 2026 deserve your attention now rather than later.

Tip 2: Who Should Consider Filing a Protective Claim

Eligibility Criteria

You may qualify for these IRS COVID refunds if you paid certain penalties and related interest during the disaster window. Failure-to-file penalties, failure-to-pay penalties, and estimated tax penalties tied to tax years 2019 through 2022 are the ones in scope.

Your original filing or payment deadline also needs to fall within the COVID-era disaster period — January 20, 2020, through July 10, 2023. If that description fits your situation, a protective claim is worth serious consideration.

Distinguishing This From ERC Claims

This distinction trips people up constantly, so it’s worth repeating. The July 10, 2026 deadline has nothing to do with filing new Employee Retention Credit claims — those deadlines have already closed.

ERC audits and litigation remain active in their own right, but the Kwong-related protective claim deadline stands apart. It’s strictly about penalties and interest.

Tip 3: How to File a Protective Claim Using Form 843

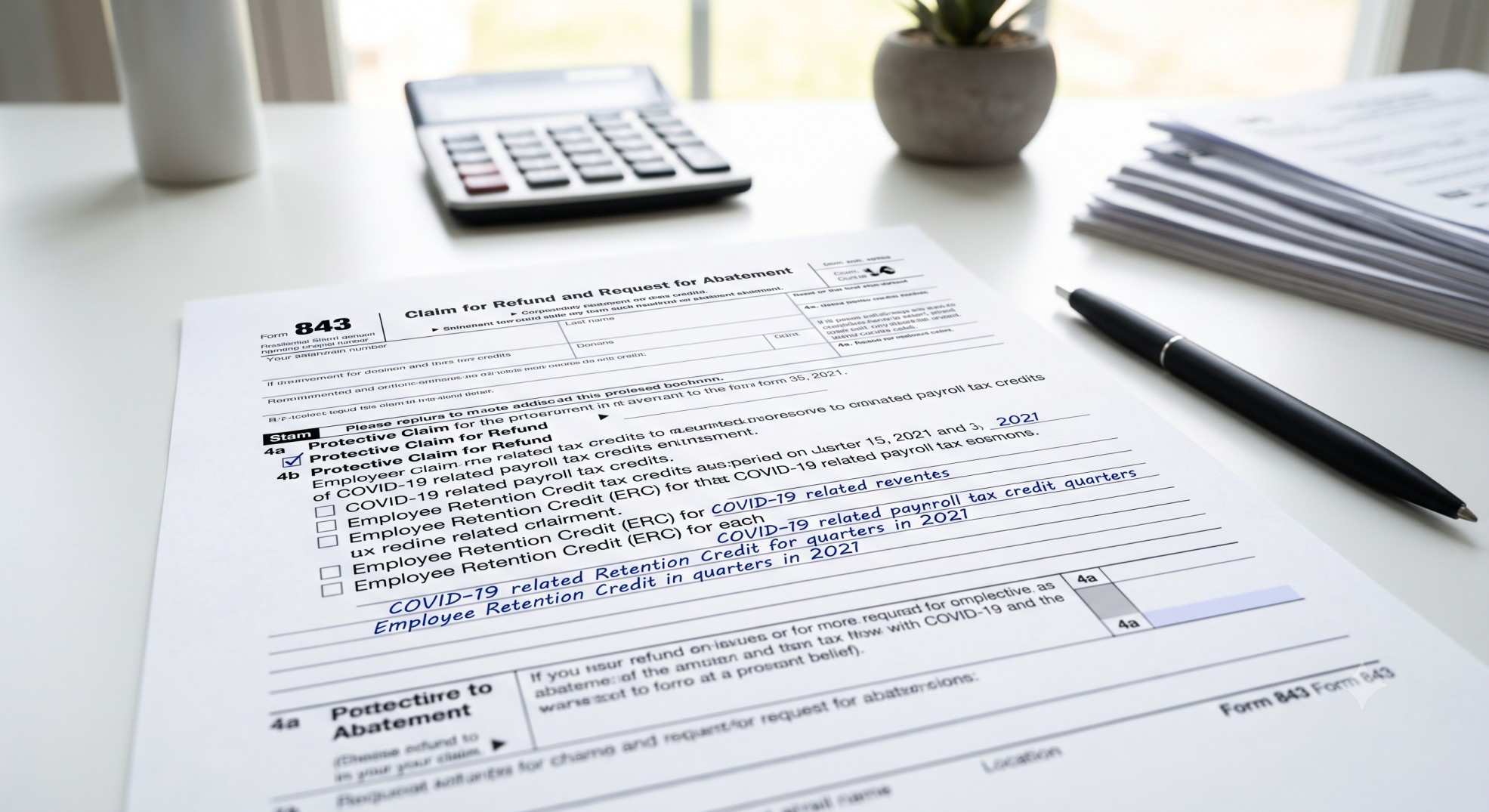

The Correct Form: Form 843, Claim for Refund and Request for Abatement

Form 843, Claim for Refund and Request for Abatement, is the document you need for this claim. The IRS designed this form specifically for requesting refunds or abatements of certain taxes, penalties, or interest.

Individuals with an IRS Online Account may have the option to submit Form 843 electronically for Kwong-related claims. Businesses, however, typically must file on paper. Checking the latest IRS guidance before you submit is always a smart move, since procedures can shift.

Key Information to Include

“Protective Refund Claim Pursuant to Kwong Case” should appear clearly at the top of your form. Identify the specific penalties, interest, and tax periods involved, and cite IRC Section 7508A(d) along with the Kwong case as your legal basis.

An exact dollar amount isn’t required at this stage. Instead, explain that your claim is contingent on the final resolution of the Kwong appeal — that language tells the IRS you’re preserving your rights, not demanding immediate payment.

Filing Best Practices

Copies of everything you submit belong in your permanent records — the completed Form 843 and any supporting statements included. Sending your claim via certified mail with a return receipt gives you documented proof of timely filing.

Proof matters enormously here, especially with a hard cutoff like July 10 sitting among these tax deadlines 2026.

Tip 4: The Millers’ Dilemma — A Real-World Example

The July 10, 2026 deadline for certain IRS COVID-related refund claims might seem irrelevant to your everyday tax planning.

It isn’t. This is a narrow window to preserve a potential refund tied to a prior tax year — and the Millers’ story shows exactly why a protective claim can matter even when the final refund figure is still unknown.

Meet the Taxpayers: The Millers

John and Sarah Miller file jointly in California and run diverse income streams, including a small consulting business. Their 2026 return is straightforward on the surface, but a complex issue from a prior COVID-impacted year — 2020 or 2021 — is still unresolved in the background and could lead to a significant federal refund.

Their 2026 Financial Snapshot

For the 2026 tax year, the Millers’ financial picture looks like this:

- W-2 Income: $500,000

- Interest Income: $5,000

- Qualified Dividends: $20,000

- Long-Term Capital Gains: $30,000

- Net Self-Employment Income (from consulting): $150,000

- Mortgage Interest Paid: $25,000

- Charitable Contributions: $10,000

- Property Tax Paid: $15,000

- California State Income Tax Paid: $60,000

The Math Behind Their 2026 Taxes

Using estimated 2026 tax parameters (based on 2024 figures adjusted for inflation), here’s how the Millers’ tax liability breaks down:

- Gross Income: $705,000.00

- Self-Employment Tax: $24,691.06 (includes Social Security, Medicare, and Additional Medicare Tax)

- Self-Employment Tax Deduction: $12,345.53 (one-half of SE tax)

- Adjusted Gross Income (AGI): $692,654.47

- Total Federal Itemized Deductions: $45,000.00 (includes mortgage interest, charitable contributions, and the $10,000 federal SALT cap)

- QBI Deduction: $0.00 (fully phased out due to high taxable income and no W-2 wages/qualified property for the consulting business)

- Federal Taxable Income: $647,654.47

- Federal Ordinary Income Tax: $150,454.56

- Federal Long-Term Capital Gains/Qualified Dividends Tax: $10,000.00 (all taxed at 20% due to high ordinary income)

- Net Investment Income Tax (NIIT): $2,090.00 (3.8% on $55,000 of investment income, as AGI exceeds $250,000 threshold)

- Alternative Minimum Tax (AMT): $0.00 (their regular tax liability is higher than their tentative minimum tax)

- Total Federal Income Tax: $187,185.62 (Federal Ordinary + LTCG/QDiv + NIIT + Total SE Tax)

- California State Taxable Income: $582,654.47 (after deducting CA itemized deductions, which are not subject to the federal SALT cap)

- California State Income Tax: $47,352.10

- Total Tax Liability (Federal + State): $234,537.72

Why a Protective Claim Matters: The COVID Connection

An unresolved issue from 2020 sits quietly behind the Millers’ otherwise clean 2026 numbers. Years earlier, they invested in a partnership that received significant COVID-era relief funds, and the final tax treatment of those funds at the partnership level is still under IRS review. Ongoing litigation could reclassify certain income or deductions from that year.

A favorable outcome could mean a corrected K-1 for 2020, one that significantly reduces their share of the partnership’s taxable income for that year. Lower 2020 AGI would follow, and potentially a substantial federal tax refund alongside it.

Standard rules would normally close that door already. The typical statute of limitations for amending a return runs three years from the filing date, meaning a 2020 return filed in April 2021 would generally expire in April 2024. But the July 10, 2026 deadline creates a special extended window for certain COVID-related claims, tied to specific IRS guidance and litigation.

Filing a protective claim before July 10, 2026 is how the Millers keep that refund possibility alive. Specifically, that means Form 843, Claim for Refund and Request for Abatement, with an explanation referencing the Kwong case. The filing formally notifies the IRS of their intent to claim a refund once the underlying partnership issue resolves, effectively keeping the statute of limitations open for that specific claim.

Takeaway

Financial stability doesn’t protect anyone from complex, unresolved tax issues left over from prior years — the Millers’ situation proves that. Delayed K-1s, uncertain taxability of relief funds, or ongoing litigation tied to the pandemic all point toward the same solution: a protective claim as your safeguard.

Filing one ensures that once the uncertainty clears, you still retain the right to claim whatever refund you’re owed, rather than watching the statute of limitations quietly close that door. A tax professional can help determine whether this applies to your specific situation.

Tip 5: Don’t Wait — Consult a Tax Professional

The Complexity of Tax Law

Straightforward is not a word that applies here. The legal landscape around the Kwong case continues to evolve while the IRS appeal plays out, which means the final outcome remains uncertain and relief is not automatic.

Proactive steps are required from you to preserve your rights in the meantime. That reality alone makes expert guidance worth seeking out.

Personalized Guidance Is Key

A qualified tax advisor — a CPA or tax attorney — should review your specific circumstances before you decide anything. Every taxpayer’s situation looks different, and a professional can help determine whether filing a protective claim makes sense for you.

Correct filing before the July 10, 2026 deadline is just as important as deciding to file at all, and a professional can make sure both boxes get checked.

Final Thoughts on the July 10, 2026 Deadline

Fast approaching is the best way to describe where this deadline stands right now. Filing a protective claim guarantees nothing, but it functions as an essential safeguard that preserves your right to a refund if the Kwong decision holds up on appeal.

Reviewing your tax situation from 2019 through 2022 costs you little time and could save you real money. Professional advice sought today beats regret discovered after July 10, 2026 has passed — don’t let these tax deadlines 2026 catch you off guard.

Consider downloading a “Determining Your Need for a Protective Claim” checklist for further assistance. This kind of resource can help you organize your information before speaking with a professional.

Official IRS.gov publications should always be your reference point for the most current instructions and guidance, since procedures around this claim can change as the appeal progresses.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.