You’ve probably searched for “LLC tax rate” and come up empty-handed on a straight answer. Here’s why: there isn’t one single rate that applies to every LLC.

Your tax bill depends on how your business is structured, how much you earn, what you can deduct, and even which state you call home. For 2026, new legislative adjustments and inflation-indexed thresholds make this even more relevant to your bottom line. This guide breaks down exactly how your LLC’s profits turn into a tax bill from the IRS and your state, so you can plan ahead with confidence. Along the way, we’ll cover LLC vs S-Corp tax benefits and the specific single-member LLC tax requirements you need to know.

Table of Contents

- The Myth of the “LLC Tax Rate”: How Entity Classification Actually Works

- Key Federal Taxes Affecting Your LLC in 2026

- State-Specific Tax Considerations (Using California as an Example)

- Real-World Scenario: Sarah’s Marketing LLC — 2026 Tax Outlook

- Strategic Tax Planning for Your LLC: Beyond the Basics

- Essential Compliance and Deadlines for LLC Owners in 2026

- Don’t Go It Alone: The Value of a Tax Professional

- Frequently Asked Questions

⚡ Executive Summary: LLC Tax Rate 2026

- No single “LLC tax rate” exists. Your liability depends entirely on how your LLC is classified for tax purposes.

- Most LLCs are taxed as a sole proprietorship (single-member) or a partnership (multi-member), with income passing through to the owners’ personal returns.

- Electing S-Corp status can offer real LLC vs S-Corp tax benefits, especially around self-employment tax savings, but it adds administrative work.

- Key federal taxes include income tax, self-employment tax, and potentially the Net Investment Income Tax (NIIT).

- The Qualified Business Income (QBI) deduction can substantially reduce your federal taxable income.

- State taxes vary widely; some states levy their own income tax plus annual LLC fees.

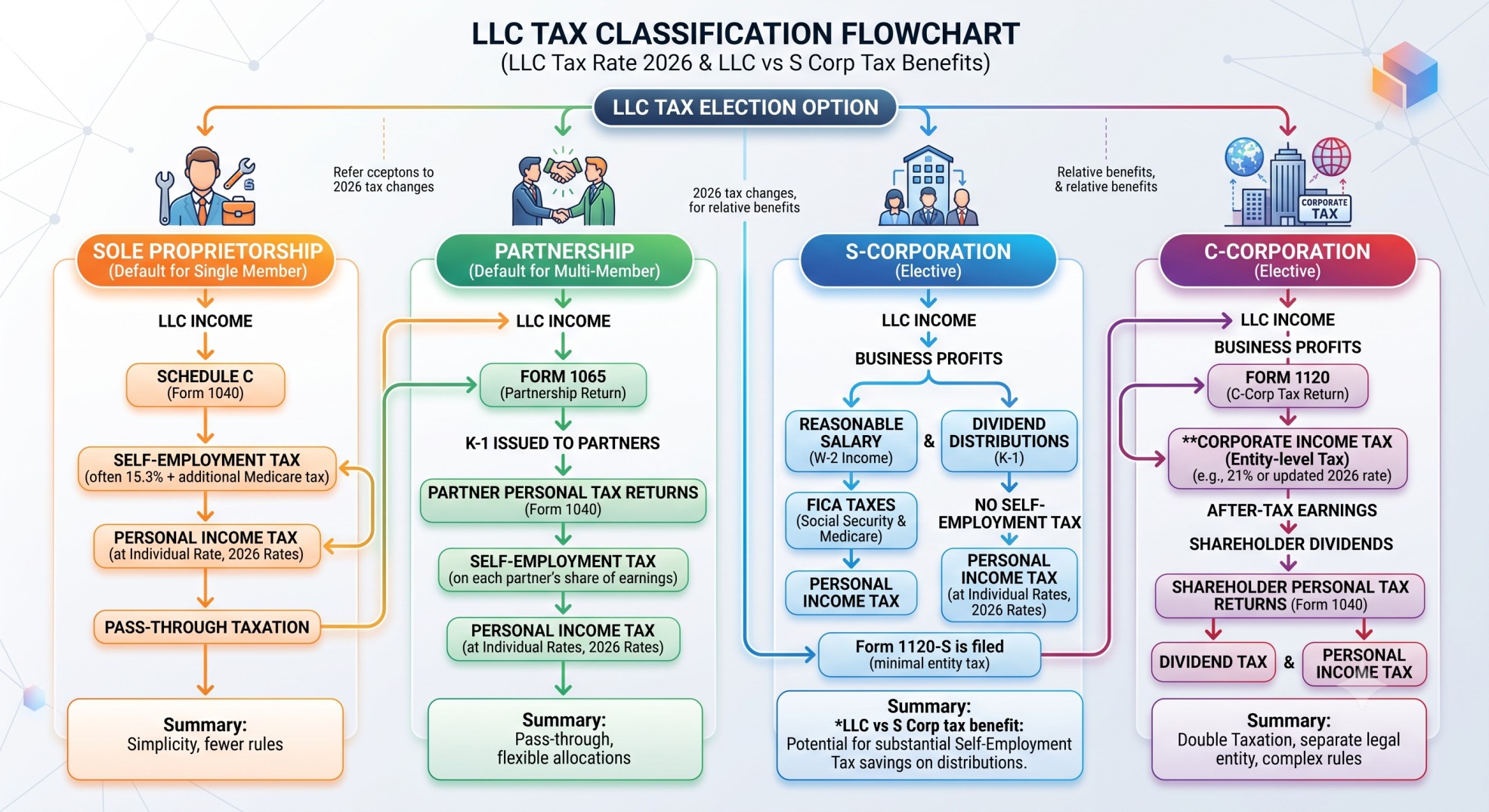

The Myth of the “LLC Tax Rate”: How Entity Classification Actually Works

An “LLC tax rate” doesn’t exist as a fixed number. The Internal Revenue Service doesn’t even recognize an LLC as a distinct tax entity in the first place.

Your LLC gets taxed based on whichever classification you choose or default into. That flexibility is actually one of the biggest perks of setting up an LLC in the first place.

Default Tax Classifications for LLCs

The IRS assigns your LLC a default tax classification the moment you form it, unless you file paperwork to elect something different. This default determines exactly how your business income gets reported.

- Single-Member LLCs (Disregarded Entity / Sole Proprietorship): A one-owner LLC is typically treated as a disregarded entity. Your LLC’s income and expenses land directly on your personal tax return, usually via Schedule C (Form 1040). You’ll pay federal income tax and self-employment taxes on your net business earnings — a setup central to single-member LLC tax requirements.

- Multi-Member LLCs (Partnership): Two or more owners generally means partnership taxation. The LLC files an informational return (Form 1065), but the business itself doesn’t pay federal income tax. Each owner instead receives a Schedule K-1 reporting their share of income or loss, then reports that on their personal return and pays income and self-employment taxes accordingly.

Electing Corporate Tax Status

Your LLC can also choose to be taxed as a corporation. This decision opens up meaningful LLC vs S-Corp tax benefits, though it comes with added complexity.

- S Corporation Election (Form 2553): Many profitable LLCs elect S-Corp status because profits and losses pass through to owners without triggering corporate tax rates. The standout benefit is a potential reduction in self-employment taxes. Owners pay themselves a “reasonable salary” subject to payroll taxes, while remaining profits distributed as dividends generally skip self-employment tax entirely.

- C Corporation Election (Form 8832): Your LLC can elect C-Corp taxation too, though it’s rare among small businesses because of “double taxation.” The corporation pays corporate income tax on profits, and shareholders then pay individual income tax on any dividends received. The federal corporate tax rate for 2026 remains a flat 21%.

Key Federal Taxes Affecting Your LLC in 2026

Several distinct federal taxes shape your total bill as an LLC owner. Each one plays a direct role in your overall tax planning.

Federal Income Tax

Business income from most LLCs flows straight through to the owner’s personal tax return. That means your profits get taxed at your individual income tax rates, not a separate business rate.

- How income flows through: Disregarded entities, partnerships, and S-Corps all report business income on your personal Form 1040. It combines with other income sources, like W-2 wages or investment income.

- 2026 Federal Income Tax Brackets (MFJ, Single): Federal income tax rates for 2026 range from 10% to 37%. The top marginal rate of 37% kicks in above $640,600 for single filers and $768,600 for married couples filing jointly. Your specific tax bracket depends on your total taxable income.

- Standard Deduction for 2026: The standard deduction sits at $32,200 for married couples filing jointly, $16,100 for single filers, and $24,150 for heads of households. This amount directly reduces your taxable income.

Self-Employment Tax (SE Tax)

Sole proprietorships and partnerships trigger self-employment tax obligations for LLC owners. This is often the single biggest surprise for new business owners.

- Who pays it and why: Self-employment tax funds Social Security and Medicare. Since you’re self-employed, you cover both the employer and employee portions yourself.

- 2026 SE Tax Rate and Wage Base Limits: The self-employment tax rate for 2026 stays at 15.3% — 12.4% for Social Security and 2.9% for Medicare. Social Security applies to net self-employment income up to $184,500 for 2026. Medicare applies to all net self-employment income with no wage cap at all.

- Deductibility of Half of SE Tax: You get to deduct one-half of your self-employment taxes paid from gross income when calculating your Adjusted Gross Income (AGI).

Qualified Business Income (QBI) Deduction (Section 199A)

The Qualified Business Income (QBI) Deduction stands out as one of the most valuable breaks available to pass-through business owners.

- What it is and how it works: Eligible owners of pass-through entities can deduct up to 20% of their QBI. You claim it on your personal tax return, and it directly reduces your taxable income.

- 2026 Income Thresholds and Phase-Outs: Limitations begin phasing in at $201,775 for single filers and $403,500 for married couples filing jointly. Deduction limits fully phase in at $276,775 for unmarried individuals and $553,500 for married couples filing jointly.

- Impact of the One Big Beautiful Bill Act (OBBBA): Passed in July 2025, the OBBBA made the QBI deduction permanent. It also expanded the phase-in ranges for wage and investment limits and introduced a new minimum QBI deduction of $400 for active business owners with at least $1,000 in QBI.

Net Investment Income Tax (NIIT)

High-income taxpayers may face an additional layer of tax on investment earnings.

- When it applies (3.8% tax): The Net Investment Income Tax (NIIT) adds a 3.8% tax on certain investment income.

- 2026 Income Thresholds: It kicks in once your Adjusted Gross Income (AGI) exceeds $200,000 for single filers or $250,000 for married couples filing jointly.

State-Specific Tax Considerations (Using California as an Example)

Federal taxes only tell half the story. State tax rules can shift your overall tax planning significantly.

State Income Tax for LLC Owners

States write their own tax rules, and those rules often diverge sharply from federal law. That creates extra layers to account for in your tax planning.

- How state rules differ from federal: California, for example, doesn’t allow the federal QBI deduction at all. State standard deductions also vary widely — California’s estimated standard deduction for married couples filing jointly in 2026 is $12,170.

- California’s progressive tax rates: California runs a progressive income tax system, meaning higher earners pay a larger percentage of income in state taxes. Those rates can add up fast for profitable LLC owners.

Other State-Level LLC Fees and Taxes

States often layer additional fees on top of income tax for LLCs specifically.

- Annual LLC fees: Many states charge a flat annual fee just for operating as an LLC. California charges an annual LLC fee of $800 for most LLCs.

Real-World Scenario: Sarah’s Marketing LLC — 2026 Tax Outlook

Numbers make abstract tax rules concrete. This case study walks through how federal income tax, self-employment tax, the QBI deduction, NIIT, and state taxes all interact for one small business owner.

Case Study: Sarah’s Marketing LLC — 2026 Tax Outlook

Sarah runs a successful freelance marketing consultancy as a single-member LLC in California.

Her LLC is treated as a disregarded entity, so business income and expenses land on Schedule C of her personal Form 1040.

She’s married filing jointly, her spouse earns W-2 income, and they have two dependent children. Here’s the projected math for 2026.

Key Financials (Projected for 2026):

- Filing Status: Married Filing Jointly (MFJ) with 2 dependent children

- Location: California

- Sarah’s LLC Gross Revenue: $350,000

- LLC Business Expenses: $50,000

- Spouse’s W-2 Income: $80,000

- Investment Income (Dividends/Interest): $15,000

- Self-Employed Health Insurance Premiums: $12,000

- Traditional IRA Contributions (Sarah & Spouse): $14,000 ($7,000 each)

Tax Calculation Breakdown for 2026:

- Net Business Income (QBI): $300,000.00 ($350,000 Gross Revenue – $50,000 Business Expenses)

- Total Self-Employment Tax: $30,912.45 (Calculated on $277,050 net earnings from SE, $184,500 SS wage base)

- Deductible Portion of SE Tax: $15,456.23 (Half of the self-employment tax is deductible)

- Gross Income: $395,000 ($300,000 Net Business + $80,000 W-2 + $15,000 Investment)

- Total Adjustments to Income: $41,456.23 ($15,456.23 Deductible SE Tax + $12,000 SE Health Insurance + $14,000 IRA)

- Adjusted Gross Income (AGI): $353,543.77 ($395,000 Gross Income – $41,456.23 Adjustments)

- Qualified Business Income (QBI) Deduction: $60,000.00 (20% of $300,000 Net Business Income)

- Federal Taxable Income (before Standard Deduction): $293,543.77 ($353,543.77 AGI – $60,000 QBI)

- Standard Deduction (MFJ 2026): $32,200

- Federal Taxable Income: $261,343.77 ($293,543.77 – $32,200)

- Gross Federal Income Tax (MFJ 2026 Brackets): $49,522.50

- Child Tax Credit: $4,000.00 ($2,000 per child for 2 children)

- Net Federal Income Tax: $45,522.50 ($49,522.50 – $4,000)

- Net Investment Income Tax (NIIT): $570.00 ($15,000 * 0.038, as AGI exceeds threshold)

- California State Taxable Income: $401,373.77 (Federal AGI + QBI add back – CA Standard Deduction)

- California State Income Tax (Estimated MFJ 2026 Brackets): $29,594.06

- Total Estimated Tax Liability: $106,599.01 ($30,912.45 SE Tax + $45,522.50 Net Federal Income Tax + $570.00 NIIT + $29,594.06 CA State Income Tax)

- Total Estimated Income: $395,000 ($300,000 Net Business Income + $80,000 W-2 Income + $15,000 Investment Income)

- Effective Tax Rate: 26.99% ($106,599.01 / $395,000 * 100%)

Takeaway for Small Business Owners:

Sarah’s numbers reveal several critical lessons for LLC owners.

- Self-Employment Tax is Significant: As an LLC taxed as a sole proprietorship, Sarah owes both the employer and employee portions of Social Security and Medicare taxes. That 15.3% tax on net business earnings makes up a substantial chunk of her overall burden.

- QBI Deduction is a Powerful Tool: The Section 199A deduction meaningfully reduced her federal taxable income. Knowing its limitations and phase-outs matters for effective tax planning.

- High-Income States Add Complexity: Living in a high-tax state like California sends a large share of income toward state taxes. That adds another layer to any planning strategy.

- AGI Matters for Other Taxes: Your Adjusted Gross Income (AGI) determines eligibility for deductions and credits, and it can trigger additional taxes like NIIT.

- Consider S-Corp Election: For LLCs with substantial profits, electing S-Corp taxation can be strategic. The owner pays a “reasonable salary” subject to payroll taxes, while remaining profits get distributed as owner distributions generally free from self-employment tax. This could lower Sarah’s overall self-employment tax burden, though it brings additional administrative costs and requires careful analysis with a tax professional.

Strategic Tax Planning for Your LLC: Beyond the Basics

Smart tax planning can meaningfully lower your effective LLC tax rate for 2026. It comes down to deliberate decisions about structure and expenses.

When to Consider an S-Corp Election

The S-Corp election has become a go-to strategy for profitable LLCs seeking real tax savings.

- Benefits (SE tax savings): The main draw is potential savings on self-employment taxes. Taking a reasonable salary while distributing remaining profits separately can shrink your overall tax burden.

- Drawbacks (administrative burden, reasonable salary rules): S-Corps demand more paperwork, including payroll processing and extra tax filings. The IRS also scrutinizes “reasonable salary” figures closely, requiring owners to pay themselves fairly for the work they actually do.

Maximizing Deductions and Credits

Every legitimate deduction or credit chips away at your taxable income or tax bill directly.

- Common business expenses: Track every business expense meticulously — office supplies, software, marketing costs, travel, and professional development all count.

- Retirement contributions (IRA, Solo 401(k)): Contributing to a Solo 401(k) or SEP IRA can generate substantial tax deductions for small business owners.

Importance of Estimated Tax Payments

LLC owners carry the responsibility of paying taxes throughout the year, not just at filing time.

- Avoiding penalties: The IRS expects income and self-employment taxes paid as you earn, not in one lump sum. Falling short on quarterly estimated payments triggers penalties.

- Setting aside funds: A solid rule of thumb: set aside 25-35% of your net business income in a separate savings account to cover upcoming tax obligations.

Essential Compliance and Deadlines for LLC Owners in 2026

Filing the right forms on time forms the backbone of managing your LLC tax rate for 2026.

Key Forms to File

- Schedule C (Form 1040): For single-member LLC tax requirements, this form reports income and expenses when your LLC is taxed as a sole proprietorship.

- Form 1065: Multi-member LLCs taxed as partnerships file this informational return.

- Form 1120-S: LLCs that elected S-Corp status file this corporate income tax return.

- Form 1040: All individual income, including pass-through LLC income, gets reported here.

Important Dates to Remember

- Quarterly estimated tax payment deadlines: These typically fall on April 15, June 15, September 15, and January 15 of the following year. A weekend or holiday landing on one of these dates pushes the deadline to the next business day.

Don’t Go It Alone: The Value of a Tax Professional

Working through your LLC tax rate for 2026 gets complicated fast, and the tax code keeps shifting under your feet.

A qualified tax professional brings real value here. They help you choose the optimal entity classification, catch every eligible deduction, keep you compliant with federal and state law, and build a solid tax planning strategy. That expertise often pays for itself by saving money and preventing costly mistakes.

Frequently Asked Questions

What is the difference between an LLC and a sole proprietorship for tax purposes?

A single-member LLC is typically treated as a sole proprietorship for tax purposes, with income and expenses reported on Schedule C of Form 1040. The real difference lies in liability protection: an LLC shields your personal assets, while a sole proprietorship offers no such protection.

Can an LLC pay no taxes?

No, an LLC cannot avoid taxes entirely. The LLC itself may skip federal income tax if it’s structured as a pass-through entity, but its income always gets taxed at the owner level. Owners owe federal income tax, self-employment taxes, and potentially state taxes on their share of profits. Effective tax planning aims to minimize liability, not eliminate it.

How does an S-Corp election save on self-employment taxes?

An S-Corp election lets you pay yourself a “reasonable salary,” which is subject to self-employment taxes, while remaining profits get distributed as dividends generally free from that tax. This structure can produce real savings compared to an LLC taxed as a sole proprietorship or partnership, where all net earnings face self-employment tax. It’s a central piece of the LLC vs S-Corp tax benefits conversation.

What records should an LLC owner keep for tax purposes?

LLC owners should maintain detailed records of income, expenses, bank statements, receipts, invoices, payroll records where applicable, and asset purchases. Strong record-keeping backs up your deductions and proves invaluable if you ever face an audit.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.