Imagine a savings account that reduces your taxable income today. Furthermore, it grows entirely tax-free. Finally, you can withdraw funds tax-free for medical expenses, even decades later. This is not a dream; it is the power of the HSA Shoebox Strategy. This effective approach builds significant tax-free wealth. For 2026, understanding this strategy could turn your healthcare savings into a powerful retirement asset. This guide will explain how this strategy works, focusing on the 2026 tax year.

Key Takeaways for the HSA Shoebox Strategy

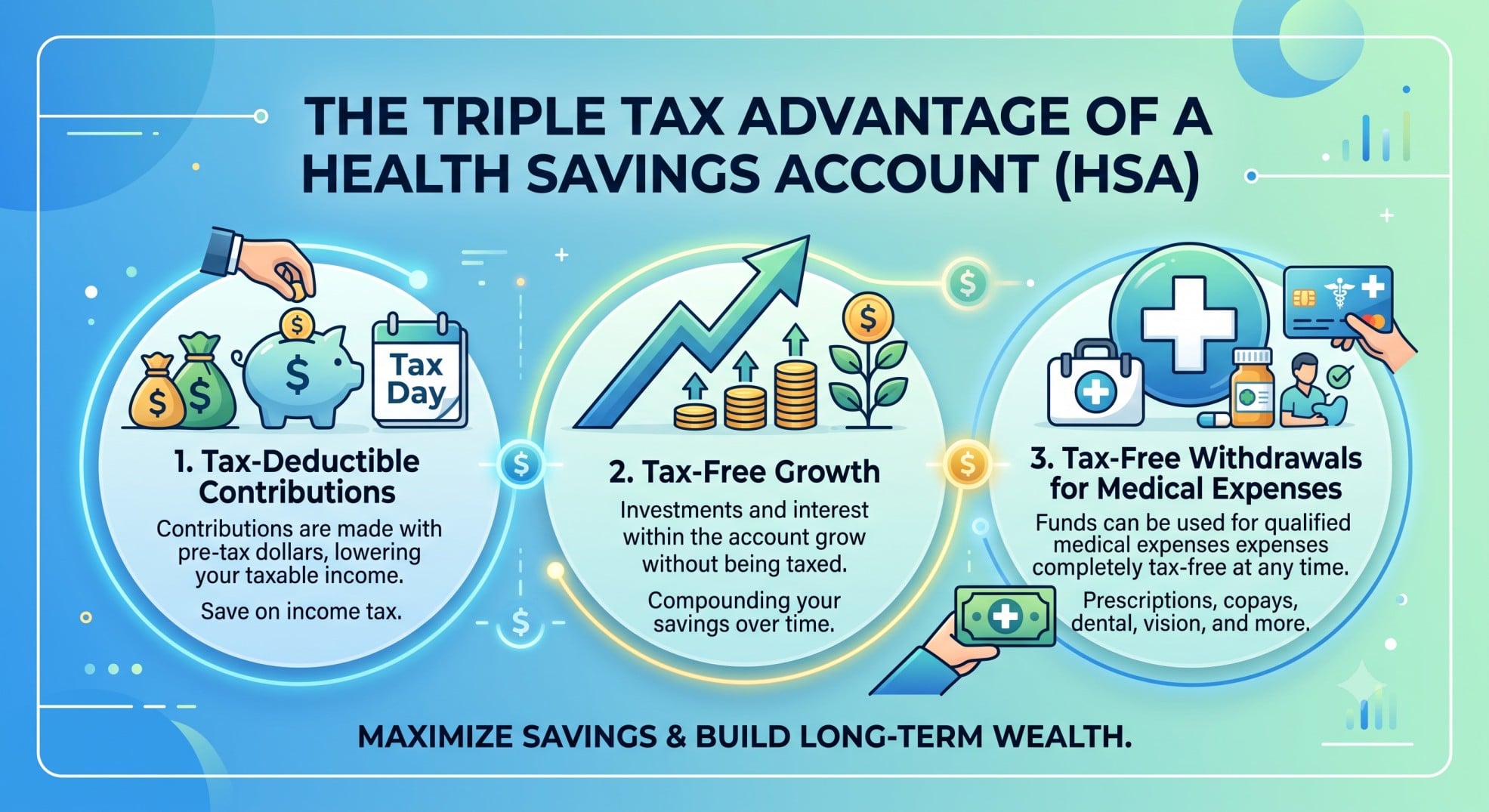

- The HSA Shoebox Strategy offers a “triple tax advantage”: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- For 2026, family HSA contributions can reach $8,750, plus an additional $1,000 for individuals over 55.

- Expanded eligibility for 2026 includes certain Bronze and Catastrophic plans, Direct Primary Care Service Arrangements, and permanent telehealth.

- Pay current medical expenses out-of-pocket, save all itemized receipts, and invest your HSA funds for long-term growth.

- Reimburse yourself tax-free from your HSA years or decades later. There is no time limit for reimbursement, provided the expense occurred after your HSA was established.

- Careful record-keeping is essential for this strategy.

What is an HSA and How the “Shoebox” Strategy Works

The Basics of a Health Savings Account (HSA)

A Health Savings Account (HSA) is a tax-advantaged savings account. It helps individuals save for future medical expenses. You must enroll in a High-Deductible Health Plan (HDHP) to be eligible for an HSA. Contributions to an HSA are tax-deductible. They reduce your Adjusted Gross Income (AGI). Funds in an HSA grow tax-free. You can withdraw them tax-free for qualified medical expenses. IRS Publication 969 provides comprehensive guidance on HSAs.

How the “Shoebox” Strategy Works

The HSA Shoebox Strategy is a long-term approach. It maximizes the tax benefits of an HSA. Here’s how it works:

- Contribute to your HSA: First, contribute the maximum allowable amount to your HSA each year. These contributions are tax-deductible.

- Pay out-of-pocket: Next, pay for your current qualified medical expenses with after-tax dollars. Do not use your HSA funds for these immediate costs.

- Save all receipts: Carefully save every itemized receipt for these out-of-pocket medical expenses. These receipts are your proof for future tax-free reimbursements.

- Invest your HSA funds: Then, invest your HSA balance for long-term growth. These funds grow tax-free, compounding over many years.

- Reimburse yourself later: Finally, years or even decades later, reimburse yourself from your HSA. You can withdraw funds tax-free for all the qualified medical expenses you paid out-of-pocket. There is no time limit for this reimbursement, provided the expense occurred after your HSA was established.

This strategy effectively turns your HSA into a powerful vehicle for retirement savings. It allows your money to grow untouched for decades.

2026 HSA Limits and Eligibility: What You Need to Know

Key 2026 Contribution Limits

The IRS sets annual limits for HSA contributions. These limits are adjusted for inflation. For the 2026 tax year, the limits are:

- Self-Only Coverage: You can contribute up to $4,400.

- Family Coverage: You can contribute up to $8,750.

- Catch-Up Contributions: Individuals aged 55 and older can contribute an additional $1,000. This is a significant benefit for older adults.

These limits are detailed in IRS Publication 969 and Revenue Procedure 2025-19.

High-Deductible Health Plan (HDHP) Requirements for 2026

To be eligible for an HSA, you must have an HDHP. These plans have specific deductible and out-of-pocket maximums. For 2026, an HDHP must meet these criteria:

- Minimum Annual Deductible:

- Self-Only: At least $1,700

- Family: At least $3,400

- Maximum Annual Out-of-Pocket Expenses: (excluding premiums)

- Self-Only: No more than $8,500

- Family: No more than $17,000

Expanded Eligibility for 2026 (The “One, Big, Beautiful Bill Act” – OBBBA)

The “One, Big, Beautiful Bill Act” (OBBBA), Public Law 119-21, brought important changes for 2026. These changes expand HSA eligibility. IRS Notice 2026-05 provides guidance on these updates.

- Bronze and Catastrophic Plans: Certain bronze and catastrophic health plans are now HSA-compatible. This applies even if they do not strictly meet traditional HDHP requirements.

- Direct Primary Care Service Arrangements (DPCSAs): You can now contribute to an HSA if you are enrolled in certain DPCSAs. You can also use HSA funds tax-free to pay periodic DPC fees.

- Permanent Telehealth Services: Telehealth and other remote care services can be received before meeting your HDHP deductible. This will not affect your HSA eligibility.

The Triple Tax Advantage: Why HSAs are a Retirement Powerhouse

Tax-Deductible Contributions

Contributions to your HSA are tax-deductible. This reduces your taxable income in the year you contribute. Therefore, you pay less in federal and, in most cases, state income taxes. This immediate tax deductions benefit is a key advantage of the HSA Shoebox Strategy.

Tax-Free Growth

Funds within your HSA grow tax-free. You do not pay capital gains or dividend taxes on your investments. This allows your money to compound more rapidly. Over decades, this tax-free growth can lead to substantial tax-free wealth. It makes HSAs excellent for retirement savings.

Tax-Free Withdrawals for Qualified Medical Expenses

The ultimate benefit is tax-free withdrawals. You pay no taxes on funds withdrawn for qualified medical expenses. This applies whether you use the funds immediately or reimburse yourself years later. Refer to IRS Publication 502 for a list of qualified medical expenses.

Post-Age 65 Flexibility

After age 65, your HSA becomes even more flexible. It functions much like a traditional IRA. You can withdraw funds for non-medical expenses. These withdrawals are subject to ordinary income tax. However, they are not subject to the 20% penalty that applies before age 65. This makes the HSA a flexible retirement savings tool.

Real-World Application: John and Jane Doe’s 2026 Strategy

John and Jane Doe, a married couple, both 40 years old, file jointly in California. They earn a combined W-2 income of $300,000. They also have $10,000 in taxable investment income, totaling $310,000 gross income. They plan to retire at age 65. They aim to maximize their tax deductions and build tax-free wealth.

Scenario Assumptions (2026 Estimates)

- HSA Contribution (Family Plan): $8,750 (for 2026)

- Annual Out-of-Pocket Medical Expenses: $5,000 (paid with after-tax dollars, receipts saved)

- HSA Investment Growth Rate: 7% annually

- Time Horizon: 25 years (until retirement at age 65)

Annual Tax Savings from HSA Contributions

By contributing the maximum family amount to their HSA, John and Jane reduce their taxable income. This leads to immediate tax savings.

- Federal Income Tax Savings: $2,100.00 (based on their marginal federal tax rate)

- California State Income Tax Savings: $901.25 (based on their marginal California state tax rate)

- Total Annual Tax Savings: $3,001.25

Their HSA contribution reduces their Modified Adjusted Gross Income (AGI). However, it does not reduce it enough to impact their Net Investment Income Tax (NIIT) liability on their $10,000 investment income.

Long-Term HSA Growth and Tax-Free Wealth

Over 25 years, John and Jane consistently contribute to their HSA. They pay for their $5,000 annual medical expenses out-of-pocket. They carefully save all receipts. The HSA funds are invested and grow tax-free.

- Total HSA Contributions Over 25 Years: $218,750 ($8,750 * 25 years)

- Total Value of HSA at Retirement (Age 65): $553,430.25 (Future value of an annuity: $8,750 annual contribution, 7% annual growth, 25 years)

- Total Out-of-Pocket Medical Expenses Paid (Receipts Saved): $125,000 ($5,000 * 25 years)

At retirement, John and Jane can withdraw up to $125,000 from their HSA. This withdrawal is completely tax-free. They are reimbursing themselves for past medical expenses. The remaining balance of $428,430.25 ($553,430.25 – $125,000) can continue to grow. It can be used for future medical expenses tax-free. Alternatively, it can be withdrawn as taxable income after age 65 for non-medical expenses.

Cumulative Tax Savings

The immediate tax deductions on their HSA contributions accumulate significantly.

- Total Tax Savings from HSA Contributions Over 25 Years: $75,031.25 ($3,001.25 annual savings * 25 years)

This figure represents direct tax savings. It is separate from the tax-free growth within the account.

Takeaway

The HSA Shoebox Strategy offers a powerful triple tax advantage. It is an exceptional tool for long-term wealth accumulation. This is especially true for taxpayers in high-tax states. By paying current medical expenses out-of-pocket and saving receipts, John and Jane Doe were able to:

- Save $3,001.25 annually in federal and state income taxes.

- Accumulate over $553,000 in a tax-free investment account.

- Create a tax-free reimbursement pool of $125,000 for past medical expenses. This pool can be accessed at any time.

This strategy transforms an HSA into a super-charged retirement savings vehicle. It provides both immediate tax benefits and substantial tax-free wealth for future medical needs or general retirement income.

Implementing the Shoebox Strategy: Practical Tips and Best Practices

Careful Record-Keeping is Essential

Saving all itemized receipts is critical for the HSA Shoebox Strategy. The IRS may ask for proof of qualified medical expenses. Digital storage solutions are often best. Scan and categorize your receipts. Keep track of the date, provider, service, amount, and patient for each expense. This diligence ensures your reimbursements remain tax-free.

Investing Your HSA Funds Wisely

Do not let your HSA funds sit in cash. Choose an HSA provider that offers good investment options. Consider low-cost index funds or exchange-traded funds (ETFs). These options align with long-term growth strategies. The goal is to maximize the tax-free compounding effect.

Understanding Qualified Medical Expenses

Only qualified medical expenses are eligible for tax-free withdrawals. Refer to IRS Publication 502 for a comprehensive list. Examples include doctor visits, prescription drugs, dental care, and vision care. Understanding these rules prevents non-qualified withdrawals.

When to Reimburse Yourself

You have flexibility in timing your reimbursements. Many individuals choose to reimburse themselves in retirement. This can provide a tax-free income stream. Others might use it for large, unexpected medical expenses. Remember, there is no time limit for reimbursement. The expense must have occurred after your HSA was established.

Potential Pitfalls and Considerations

The Importance of an HDHP

Maintaining an HDHP is essential for HSA eligibility. If your health plan no longer qualifies as an HDHP, you cannot contribute to your HSA. However, you can still use existing funds for qualified medical expenses.

Non-Qualified Withdrawals

Withdrawing funds for non-qualified expenses before age 65 incurs penalties. These withdrawals are subject to ordinary income tax. They also face a 20% penalty. After age 65, non-qualified withdrawals are only subject to ordinary income tax, like a traditional IRA.

Inflation and Medical Costs

Healthcare costs continue to rise. The tax-free growth of your HSA funds helps fight inflation. This strategy provides a valuable hedge against future medical expenses. It ensures your tax-free wealth maintains its value.

Conclusion: Your Path to Tax-Free Healthcare Wealth

The HSA Shoebox Strategy is a powerful financial planning tool. It offers a unique triple tax advantage. It can significantly boost your retirement savings. By understanding 2026 rules and careful record-keeping, you can build substantial tax-free wealth.

This content is for informational purposes only. It does not constitute tax, legal, or financial advice. Tax laws are complex and can change. Individual circumstances vary. Therefore, consult with a qualified tax professional or financial advisor before making any decisions.

Take control of your financial future. Explore how the HSA Shoebox Strategy can work for you. Proactive financial planning today creates a more secure tomorrow.