Executive Summary :

- For 2025, partnerships must report partner capital accounts on Schedule K-1 Box L using the tax basis method.

- This method tracks contributions, distributions, and income/loss allocations based on tax principles.

- Box L excludes partnership liabilities, unlike a partner’s overall “outside basis.”

- New 2025 regulations under IRC Section 6011 identify certain related-party basis-shifting transactions as “transactions of interest” (TOIs).

- A $10 million threshold for basis increases triggers TOI reporting for related partners.

- Accurate capital account reporting is essential for loss limitations, distribution taxability, and sale of partnership interests.

- HNWI tax planning requires good record-keeping and expert tax advice to ensure compliance and improve tax positions.

As a High-Net-Worth Individual, your financial situation often includes sophisticated investments. These frequently involve significant partnership interests. For the 2025 tax year, understanding Schedule K-1 Box L—your capital account reporting—is not just a compliance checkbox. It is a key part of effective tax planning, loss limitation, and future wealth management. With new regulations and increased IRS focus, a clear understanding of these rules is more critical than ever. Are you fully prepared for the implications of your 2025 Schedule K-1?

Understanding Schedule K-1 Box L: The Foundation of Partnership Basis

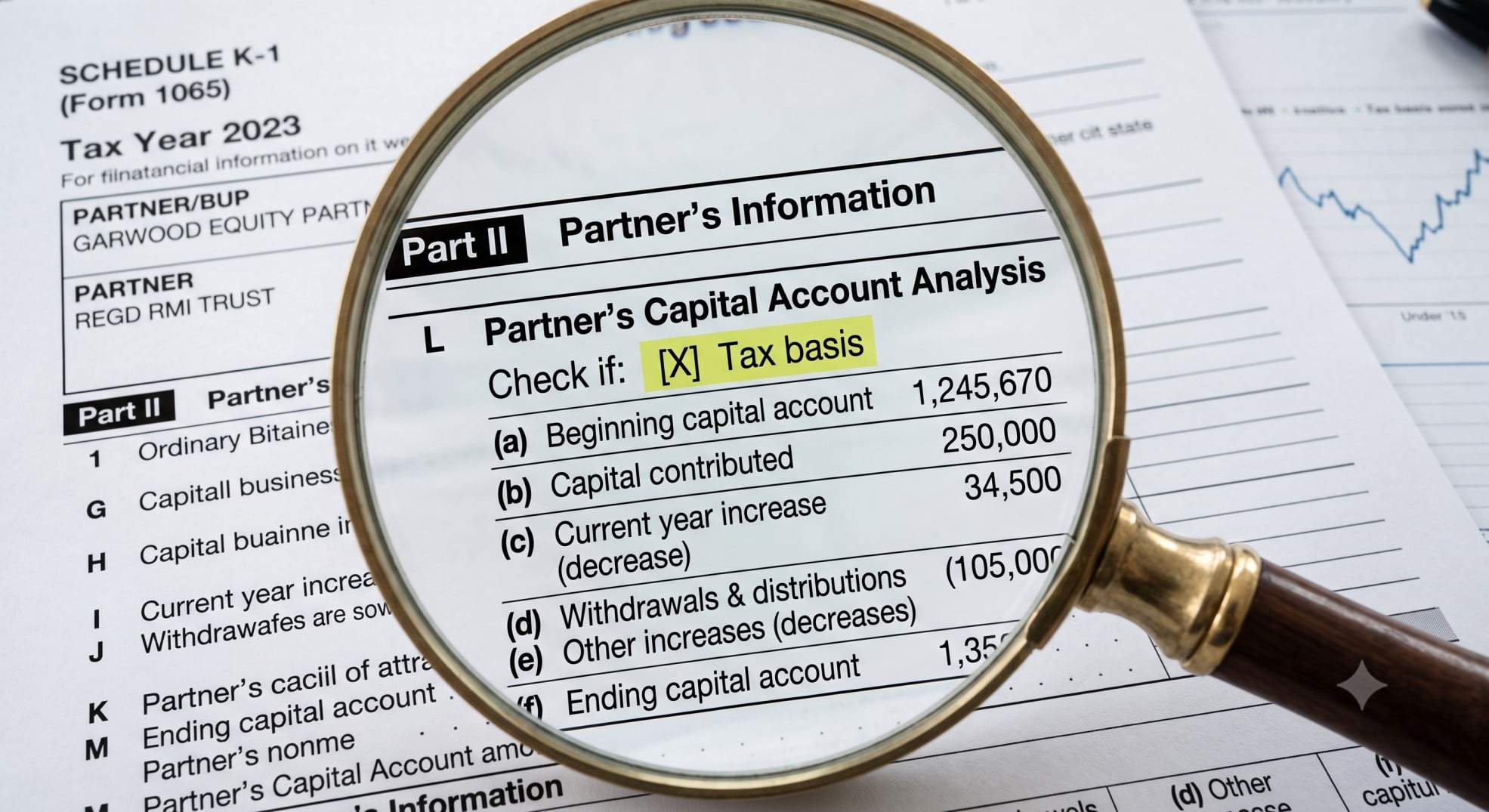

What is Schedule K-1 Box L?

Schedule K-1 Box L reports your capital account in a partnership. This account represents your equity stake in the partnership. It reflects your contributions, share of profits and losses, and distributions received. For partners, especially High-Net-Worth Individuals (HNWIs), this figure is vital. It helps determine the taxability of distributions and the gain or loss on selling a partnership interest.

The Mandatory Shift to Tax Basis Reporting (Effective 2020, Critical for 2025)

Historically, partnerships could use various methods to report capital accounts. These included GAAP or Section 704(b) book basis. However, for tax years beginning on or after January 1, 2020, the IRS mandated the tax basis method. This change significantly impacts HNWIs with complex partnership structures. It requires a consistent, tax-centric approach to capital account reporting. IRS Notice 2020-43 and subsequent guidance solidified this requirement. Therefore, 2025 continues this mandatory reporting.

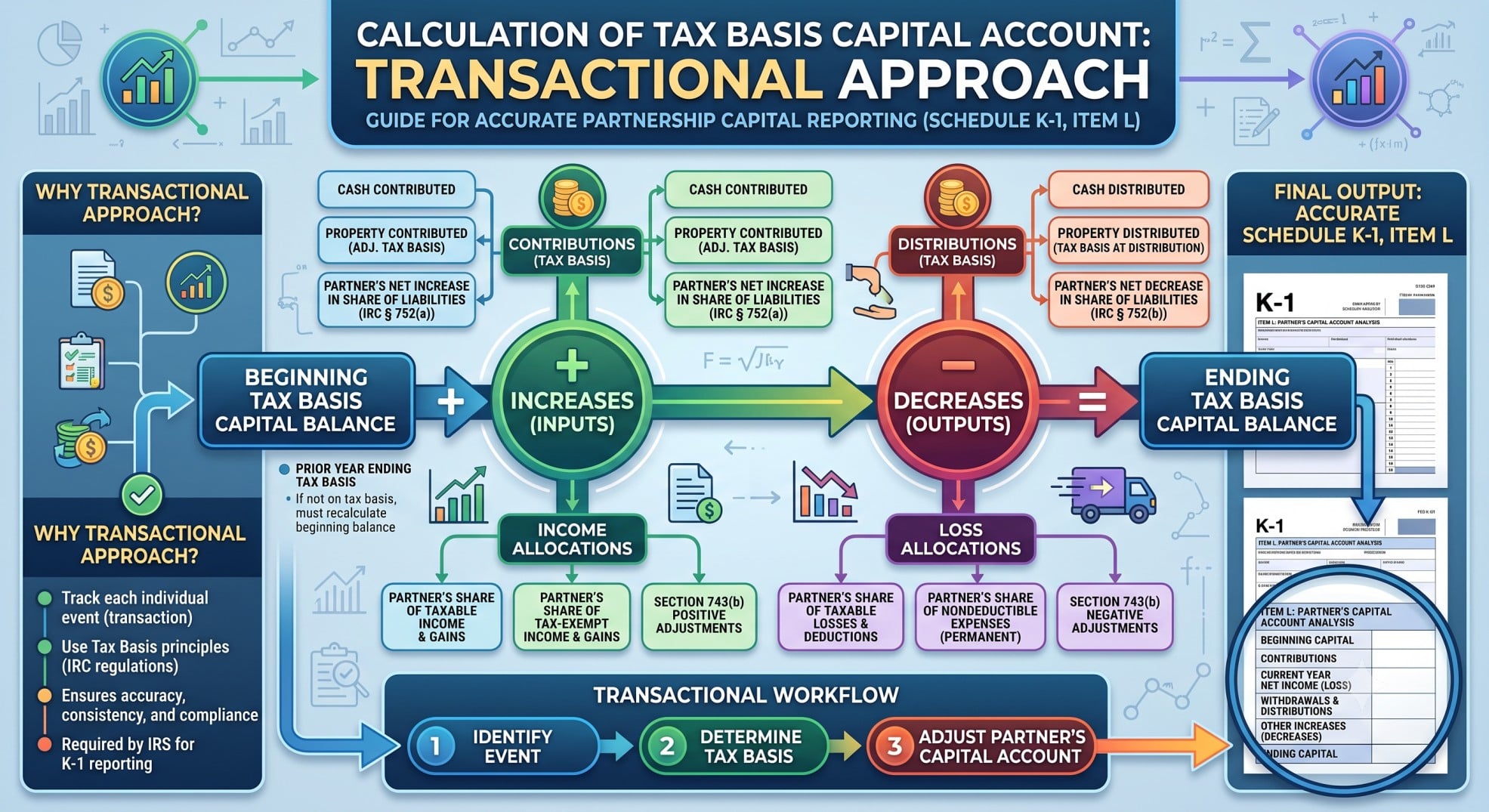

The Tax Basis Method: A Transactional Approach for 2025

How the Tax Basis Capital Account is Calculated

The tax basis method uses a transactional approach. It tracks specific financial events. Your capital account increases with money and the tax basis of property you contribute. It also increases with your allocated share of income or gain. Conversely, your capital account decreases with money and the tax basis of property distributed to you. It also decreases with your allocated share of losses or deductions. This method provides a precise, real-time reflection of your investment for HNWI tax planning.

Key Distinction: Box L Capital Account vs. Outside Basis

It is crucial to understand the difference between your Box L capital account and your “outside basis.” Your outside basis is your adjusted tax basis in your partnership interest. It includes your share of partnership liabilities under IRC Section 752. However, the Box L capital account specifically excludes these liabilities. HNWIs must track both figures. This dual tracking is essential for accurate tax planning, especially for loss limitations and distribution taxability.

Impact of Schedule K-1 Box L on HNWI Tax Planning

Loss Limitations and Basis

Your ability to deduct partnership losses depends on your basis. Both your Box L capital account and your outside basis limit deductible losses. The “at-risk” rules and passive activity loss rules also interact with your basis. Accurate capital account reporting is very important. It ensures you can claim eligible losses without exceeding your basis limitations.

Taxability of Distributions

Partnership distributions generally reduce your basis. However, distributions can become taxable if they exceed your outside basis. This is why accurate basis tracking is so important. It helps HNWIs avoid unexpected tax liabilities. Proper HNWI tax planning involves anticipating these scenarios.

Sale or Exchange of a Partnership Interest

When you sell or exchange a partnership interest, your basis determines your gain or loss. The relationship between your Box L capital account, outside basis, and rules like IRC Section 7704 (for publicly traded partnerships) is important. Understanding these elements ensures proper tax treatment when you dispose of an interest.

New Regulations for 2025: Basis-Shifting Transactions and “Transactions of Interest” (TOIs)

IRC Section 6011 and the January 2025 Final Regulations

The IRS has increased its focus on complex partnership structures. Final regulations issued in January 2025 under IRC Section 6011 define certain related-party basis-shifting transactions as “transactions of interest” (TOIs). These regulations aim to prevent misuse. They require specific disclosure from partnerships and partners. This is an important development for HNWIs.

The $10 Million Threshold for Basis Increases (2025)

For tax years from 2025, a specific reporting obligation exists. It applies to related-party basis-shifting transactions. If these transactions result in a basis increase exceeding $10 million, they trigger TOI reporting. This threshold applies to basis increases from which related partners benefit. Non-compliance carries severe consequences for HNWIs. Therefore, understanding this threshold is vital for HNWI tax planning.

IRS Focus Areas and Audit Risk for HNWIs

These new regulations are particularly relevant for HNWIs with multi-entity structures. The IRS is actively targeting transactions that lack economic substance. Non-disclosure of reportable transactions can lead to substantial penalties. Consequently, HNWIs face increased audit risk if they engage in such transactions without proper reporting. The IRS views accurate Schedule K-1 Box L reporting as essential.

Compliance and Strategic Planning for HNWIs in 2025

Proactive Data Management and Record-Keeping

Good systems are necessary for tracking tax basis capital accounts. This includes careful record-keeping of contributions, distributions, and income/loss allocations. For existing partnerships, reconstructing historical basis might be necessary. This proactive data management is fundamental for accurate capital account reporting.

The Role of Professional Tax Advisors

Given the complexity, HNWIs need experienced CPAs and tax attorneys. These professionals help reduce audit risk. They also improve tax positions within the framework of new rules. Their expertise ensures compliance and strategic benefits. Therefore, consult with qualified advisors for specific guidance.

Anticipating Future Regulatory Changes

The IRS continues its focus on partnership reporting. HNWIs should anticipate ongoing regulatory changes. Staying informed and proactive is key. This helps maintain compliance and adapt HNWI tax planning strategies effectively.

Conclusion: Proactive Planning is Key for 2025 and Beyond

Accurate Schedule K-1 Box L reporting is more than a compliance exercise for HNWIs. It is a fundamental part of sound financial management. The mandatory tax basis method and new TOI regulations for 2025 demand careful attention. Proactive data management and expert guidance are essential. Therefore, consult with qualified tax professionals. They can help you understand these complexities, reduce risks, and improve your HNWI tax planning strategy for 2025 and beyond.

Disclaimer:

This content is for informational purposes only. It does not constitute tax, legal, or financial advice. The information provided reflects current tax law and guidance for the 2025 tax year. Tax laws are complex and subject to change. High-Net-Worth Individuals should consult with a qualified tax professional or financial advisor for personalized advice tailored to their specific circumstances.