Two investment strategies keep coming up whenever high-net-worth investors talk about after-tax returns: direct indexing and traditional index funds. Both promise broad market exposure, but the tax consequences for your 2026 portfolio couldn’t be more different. This guide breaks down why direct indexing for high net worth investors can deliver meaningful annual tax savings, largely through enhanced tax loss harvesting of individual stocks.

⚡ Executive Summary: Direct Indexing vs. Index Funds for 2026

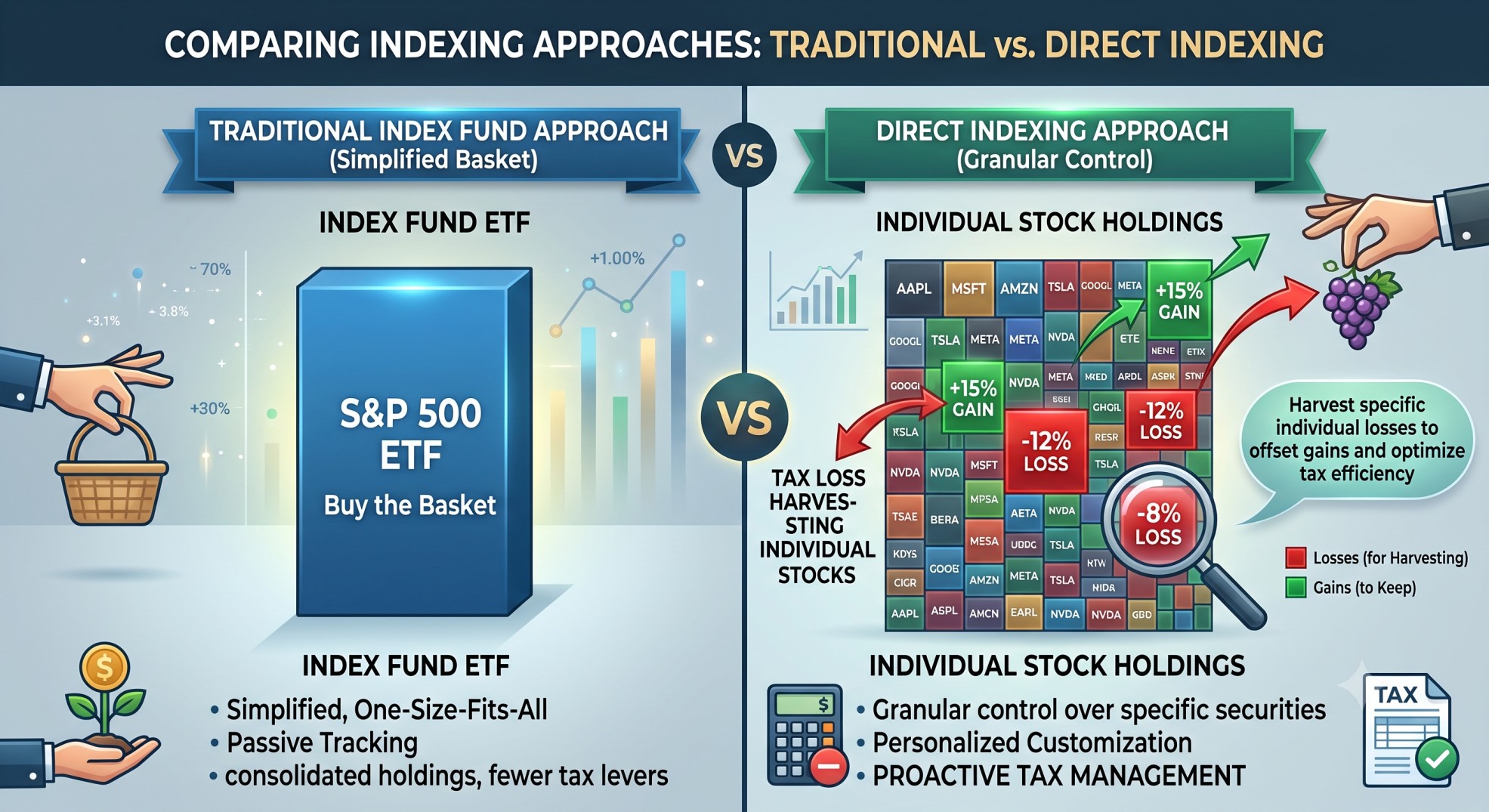

- Direct indexing means owning the individual stocks inside an index directly, rather than buying fund shares, which opens the door to detailed tax management.

- Traditional index funds deliver broad market exposure but limit your ability to harvest losses on individual positions.

- For the 2026 tax year, direct indexing offers superior tax efficiency, largely through enhanced tax loss harvesting.

- The strategy can generate “tax alpha” — added return that comes purely from offsetting capital gains and up to $3,000 of ordinary income each year.

- Customization options, including ESG screening and the ability to exclude specific companies, stand out as a distinct benefit of direct indexing.

- The Wash Sale Rule under IRC Section 1091 governs how losses can be claimed and requires careful monitoring.

- High-net-worth individuals should work with tax and financial advisors before implementing either strategy.

Table of Contents

- Why Investment Choice Matters for Tax-Smart High-Net-Worth Investors

- Traditional Index Funds: The Familiar, Tax-Limited Approach

- Direct Indexing: A Tailored, Tax-Efficient Alternative

- Key Tax Rules That Shape Your 2026 Investment Strategy

- A 2026 Tax Scenario: Comparing Real Dollar Savings for a High-Net-Worth Couple

- Beyond Tax Savings: Customization and Portfolio Control

- Trade-Offs to Weigh Before Choosing Direct Indexing

- Making the Right Call for Your Portfolio

Why Investment Choice Matters for Tax-Smart High-Net-Worth Investors

High-net-worth individuals face a specific challenge: stretching after-tax returns as far as possible. Your investment choices directly shape your tax liability, which makes understanding these two strategies essential. This article compares direct indexing and traditional index funds side by side. Both target broad market exposure, yet the tax outcomes for your 2026 portfolio diverge sharply. Below, you’ll see how one approach can meaningfully boost your after-tax wealth.

Traditional Index Funds: The Familiar, Tax-Limited Approach

Traditional index funds are pooled investment vehicles — think Exchange-Traded Funds (ETFs) or mutual funds — that track a specific market index like the S&P 500. Investors buy shares of the fund itself, and the fund holds an entire basket of underlying stocks. These vehicles offer diversification, low costs, and simplicity, giving you broad market exposure without the work of picking individual stocks.

Tax limitations come with that simplicity, and they matter for high-net-worth investors. Tax loss harvesting opportunities exist only at the fund level, not the stock level. Capital gains distributions from the fund can also trigger taxes even when you haven’t sold a single share. On top of that, you have no control over which individual stocks the fund holds.

Direct Indexing: A Tailored, Tax-Efficient Alternative

Direct indexing means owning the individual stocks that make up a chosen index, rather than buying shares of a fund that holds them. This approach builds a managed portfolio of hundreds or even thousands of individual securities in your name. High-net-worth investors gain several real advantages from this structure.

Enhanced tax loss harvesting of individual stocks stands out as the primary benefit. Selling individual underperforming stocks lets you realize losses that offset capital gains elsewhere in your portfolio. Those losses can also offset up to $3,000 of ordinary income each year, and any amount you don’t use carries forward indefinitely. This capability separates direct indexing for high net worth portfolios from anything a pooled fund can offer.

Extensive customization comes standard with direct indexing too. You can apply ESG (Environmental, Social, Governance) screens, exclude specific industries, or avoid particular companies altogether. This flexibility proves especially useful for managing concentrated stock positions — say, shares accumulated through an employer. That level of control gives direct indexing a real edge over standard custom indexing vs ETF options. Taken together, these features create what’s known as “direct indexing tax alpha” — the extra return generated purely through tax efficiency.

Key Tax Rules That Shape Your 2026 Investment Strategy

Capital gains and losses sit at the center of investment planning for the 2026 tax year. Long-Term Capital Gains (LTCG) rates are projected to remain at 0%, 15%, and 20%, depending on your taxable income bracket. Short-Term Capital Gains (STCG), by contrast, get taxed at ordinary income rates — potentially as high as 37% for high-net-worth investors. Capital loss deductions stay capped at $3,000 against ordinary income each year, though unused losses carry forward indefinitely under IRC Section 1211 and IRC Section 1212. IRS Publication 550, “Investment Income and Expenses,” and IRS Publication 544, “Sales and Other Dispositions of Assets,” cover these rules in full detail.

What Is the Wash Sale Rule Under IRC Section 1091?

The Wash Sale Rule blocks you from claiming a tax loss if you buy a “substantially identical” security within 30 days before or after the sale that generated the loss — a 61-day window in total. This rule sits at the center of any direct indexing strategy. Missing it means losing the tax loss harvesting benefit you were counting on.

Treasury Regulation § 1.1091-1 spells out exactly what counts as “substantially identical” securities. Advanced platforms and software become essential here, since managing hundreds of individual positions manually while avoiding wash sales is nearly impossible to do by hand.

Does the Net Investment Income Tax Apply to Direct Indexing or Index Funds?

Yes — the Net Investment Income Tax (NIIT) applies a 3.8% surtax on investment income once your Adjusted Gross Income (AGI) crosses certain thresholds, and it can hit either strategy. For 2026, that threshold sits around $250,000 for married couples filing jointly. Both direct indexing and traditional index funds can trigger NIIT liability, but direct indexing’s ability to reduce your taxable investment income can lower what you ultimately owe.

Alternative Minimum Tax (AMT) and State Income Taxes: Additional Layers to Watch

The Alternative Minimum Tax remains a real factor for high-net-worth investors, since investment income feeds directly into your AMT calculation. State income taxes compound the effect — high-tax states like California can push your overall burden significantly higher. Reducing your overall taxable income through direct indexing helps soften both of these impacts.

A 2026 Tax Scenario: Comparing Real Dollar Savings for a High-Net-Worth Couple

Numbers tell this story better than theory does. Consider a married couple filing jointly in California, sitting on substantial income and a sizable investment portfolio for the 2026 tax year.

The Profile: A High-Net-Worth California Couple

| Filing Status | Married Filing Jointly (MFJ) |

| Adjusted Gross Income (AGI) from Salary/Business | $1,000,000 |

| Investment Portfolio Value | $10,000,000 |

| Annual Long-Term Capital Gains (LTCG) Realized | $500,000 (5% of portfolio) |

| Other Itemized Deductions | $10,000 |

| Property Taxes Paid (California) | $15,000 (fully deductible for state, capped for federal) |

Key 2026 Tax Parameters Used in This Example

| Federal Income Tax Brackets (MFJ) | Up to 37% |

| Long-Term Capital Gains (LTCG) Rates (MFJ) | 0%, 15%, 20% |

| Net Investment Income Tax (NIIT) | 3.8% on the lesser of Net Investment Income or AGI exceeding $250,000 (MFJ) |

| Alternative Minimum Tax (AMT) | Exemption phase-out for high earners, rates of 26% and 28%. State and Local Taxes (SALT) are added back for AMT calculation. |

| California State Income Tax (MFJ) | Progressive rates up to 13.3% (including 1% mental health surcharge for income over $1,000,000) |

| Federal SALT Deduction Cap | $10,000 |

Scenario 1: Investing Through a Traditional Index Fund

In this scenario, the couple invests in a traditional S&P 500 index fund. The fund distributes $500,000 in long-term capital gains annually, and that entire amount is taxable.

| Total AGI | $1,000,000 (ordinary) + $500,000 (LTCG) = $1,500,000 |

| California State Taxable Income | $1,500,000 (AGI) – $10,000 (other itemized deductions) = $1,490,000 |

| California State Income Tax | $168,000 |

| Federal Itemized Deductions | $10,000 (SALT cap) + $10,000 (other itemized) = $20,000 |

| Federal Ordinary Taxable Income | $1,000,000 – $20,000 = $980,000 |

| Federal Long-Term Capital Gains Taxable Income | $500,000 |

| Federal Ordinary Income Tax | $290,000 |

| Federal LTCG Tax | $100,000 |

| Net Investment Income Tax (NIIT) | ($1,500,000 AGI – $250,000 threshold) x 3.8% = $47,500 |

| Regular Federal Tax Liability | $290,000 + $100,000 + $47,500 = $437,500 |

| AMT Liability | $0 (Regular tax is higher, so no additional AMT owed; Tentative Minimum Tax approximately $390,000 against AMT taxable income of $1,435,500) |

| Total Federal Tax | $437,500 |

| Total California State Tax | $168,000 |

| Total Tax Liability | $605,500 |

Scenario 2: Direct Indexing With Active Tax Loss Harvesting

With direct indexing, the couple holds individual stocks that mirror the S&P 500 instead of fund shares. This structure allows for proactive tax loss harvesting throughout the year. Assume they harvest $100,000 in losses annually, which first offset capital gains before any remainder — up to $3,000 — offsets ordinary income.

| Harvested Losses | $100,000 |

| Offset Capital Gains | $500,000 (initial LTCG) – $100,000 (harvested losses) = $400,000 |

| Ordinary Income Offset | $0 (all losses used against capital gains) |

| Total AGI | $1,000,000 (ordinary) + $400,000 (net LTCG) = $1,400,000 |

| California State Taxable Income | $1,400,000 (AGI) – $10,000 (other itemized deductions) = $1,390,000 |

| California State Income Tax | $156,000 |

| Federal Itemized Deductions | $10,000 (SALT cap) + $10,000 (other itemized) = $20,000 |

| Federal Ordinary Taxable Income | $1,000,000 – $20,000 = $980,000 |

| Federal Long-Term Capital Gains Taxable Income | $400,000 |

| Federal Ordinary Income Tax | $290,000 |

| Federal LTCG Tax | $80,000 |

| Net Investment Income Tax (NIIT) | ($1,400,000 AGI – $250,000 threshold) x 3.8% = $43,700 |

| Regular Federal Tax Liability | $290,000 + $80,000 + $43,700 = $413,700 |

| AMT Liability | $0 (Regular tax is higher, so no additional AMT owed; Tentative Minimum Tax approximately $350,000 against AMT taxable income of $1,309,500) |

| Total Federal Tax | $413,700 |

| Total California State Tax | $156,000 |

| Total Tax Liability | $569,700 |

The Bottom Line: Annual Tax Savings

Direct indexing saved this couple $35,800 in a single tax year compared to the traditional index fund approach.

That gap comes entirely from harvesting $100,000 in losses to offset capital gains — no change in market exposure, just smarter tax management.

The advantage grows even larger in high-tax states like California and for investors already facing the Net Investment Income Tax.

This scenario shows how direct indexing can produce substantial annual tax savings by strategically offsetting capital gains. Market exposure stays nearly identical to a traditional index fund in both cases — the difference comes entirely from managing individual stock lots for tax purposes. That gap becomes even more pronounced in high-tax states like California and for investors already facing higher federal brackets and the Net Investment Income Tax.

Beyond Tax Savings: Customization and Portfolio Control

Tax advantages tell only part of the story with direct indexing. This strategy also gives you substantial customization, letting you tailor a portfolio around your personal values and financial goals. Applying Environmental, Social, and Governance (ESG) screens or excluding specific industries and companies becomes possible in a way that pooled funds simply don’t allow.

Concentrated stock positions — often left over from a previous employer — become much easier to manage with this level of control. Direct indexing also lets you align your investments with philanthropic goals. This customization sets direct indexing for high net worth investors apart from a standard custom indexing vs ETF approach.

Trade-Offs to Weigh Before Choosing Direct Indexing

Direct indexing isn’t free of downsides despite its benefits. The strategy demands advanced technology and active management to avoid wash sales and stay compliant with tax rules. Costs still tend to run higher than traditional ETFs, even though they’ve come down over the years — though the potential tax alpha often justifies those management fees.

Minimum investment amounts also run higher than what traditional index funds require, which is part of why this strategy suits high-net-worth individuals specifically. Market volatility drives how much tax loss harvesting opportunity actually exists in any given year, so results will vary. Working with experienced advisors remains essential for proper implementation and for capturing the full benefit of this approach.

Making the Right Call for Your Portfolio

Significant advantages await high-net-worth individuals who choose direct indexing over traditional index funds. Enhanced tax alpha and greater customization set this strategy apart, while traditional index funds — despite their simplicity — offer far fewer opportunities for advanced tax planning.

Detailed tax loss harvesting of individual stocks makes direct indexing a genuinely powerful tool, especially given the 2026 tax environment described above. Grasping how direct indexing works for high net worth portfolios matters more than ever under these conditions. Consulting a qualified tax advisor and financial planner remains the best next step, since they can help determine which strategy actually fits your specific financial situation.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.