You’ve spent decades building your nest egg, and now you’re staring down a stretch of years that could shape your tax bill for the rest of your life. The window before Required Minimum Distributions (RMDs) and Social Security kick in gives you a rare chance to reshape how much you’ll eventually owe the IRS. Financial planners call this window the Bridge Years strategy, and for 2026 it deserves a closer look.

This guide walks through how a Roth conversion in 2026 can work in your favor once you’re over 65. You’ll find concrete numbers, a real-world example, and the details that actually matter for retirement tax planning, not just abstract theory.

⚡ Executive Summary: The Bridge Years Strategy in 2026

- The Bridge Years strategy converts pre-tax retirement funds into a Roth IRA during early retirement, before RMDs and Social Security begin.

- This stretch of lower income often lets you convert funds at reduced tax rates compared with later retirement years.

- Benefits include smaller future RMDs, a source of tax-free income, and possible savings on Medicare premiums.

- Specific 2026 dollar figures and thresholds determine exactly how much you can convert without jumping into a higher bracket.

- A qualified tax professional should review your numbers before you commit to any conversion plan.

Table of Contents

- Understanding Your Retirement Tax Advantage

- How the Bridge Years Strategy Actually Works

- Key 2026 Figures You Need for Roth Conversions

- Essential 2026 Tax Figures for Retirees Over 65

- Real-World Case Study: Eleanor’s Bridge Year in California

- Critical Considerations Before You Convert in 2026

- Regulatory Landscape and What’s Ahead for 2026

- Conclusion: Take Control of Your Retirement Tax Future

Understanding Your Retirement Tax Advantage

What Exactly Are the “Bridge Years”?

The Bridge Years are the stretch between early retirement and the start of Required Minimum Distributions (RMDs) and Social Security payments. Income typically drops during this period, which opens a rare window for deliberate tax planning.

Most retirees watch their taxable income fall once they leave full-time work behind. That temporary dip becomes a chance to manage tax liabilities before they pile up in later decades. Grasping this window is central to the whole Bridge Years strategy.

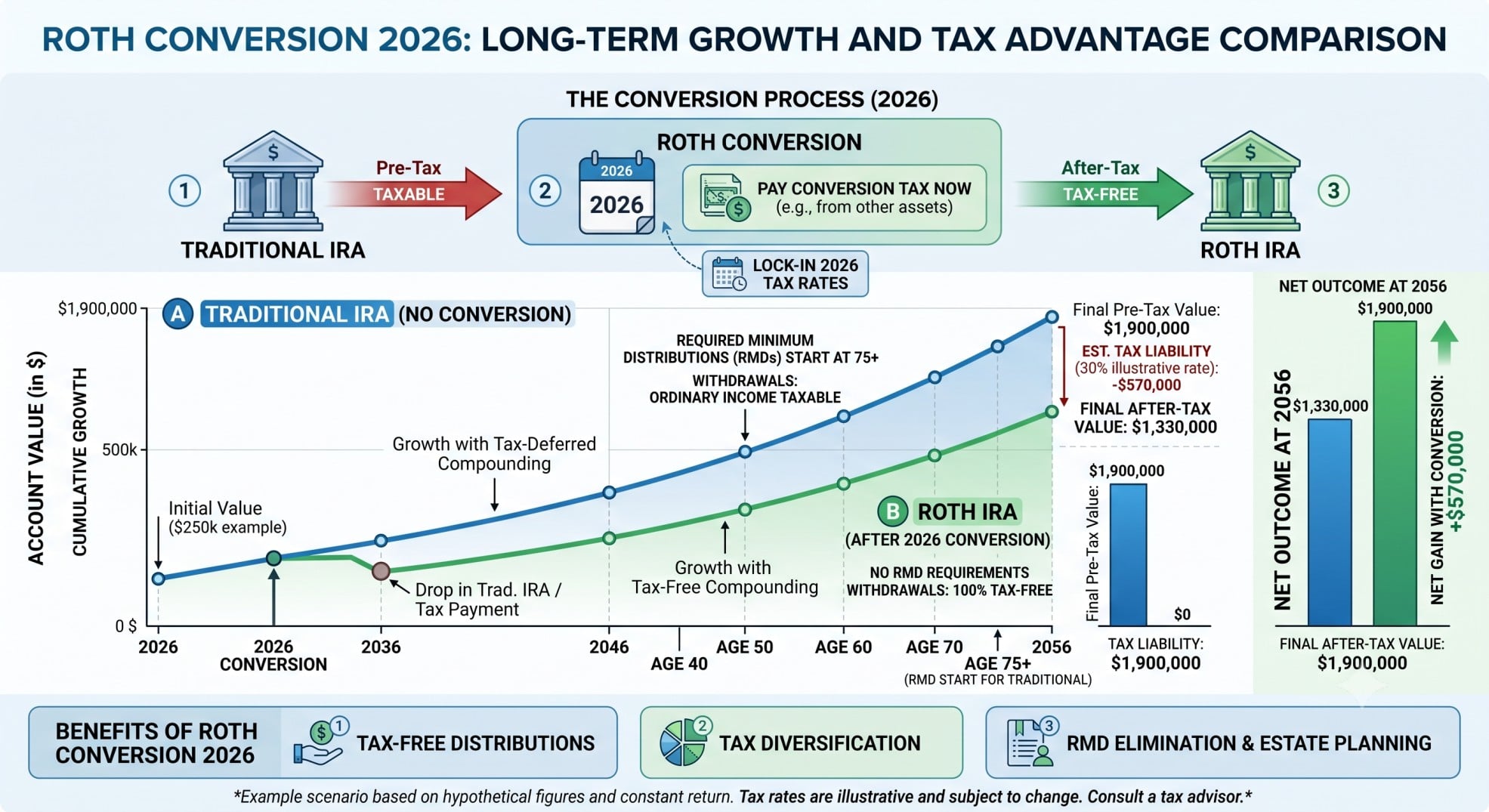

Why Strategic Roth Conversions Matter

A Roth conversion moves money from a pre-tax account, such as a Traditional IRA or 401(k), into a Roth IRA. You’ll owe tax on the converted amount in the year you convert it. Every qualified withdrawal after that, though, comes out completely tax-free.

Retirees over 65 have solid reasons to consider this move in 2026. Paying tax now, while your rate is likely lower than it will be later, can translate into real long-term savings. It also hands you more control over how your income streams look once you’re fully retired.

How the Bridge Years Strategy Actually Works

The Core Idea: Filling Up Lower Tax Brackets

The U.S. tax system taxes income in layers rather than at one flat rate. Lower income during the Bridge Years pushes you into lower tax brackets, and that’s exactly where a Roth conversion does the most good.

Every dollar you convert adds to your taxable income for that year. Calculate the conversion amount carefully, and you can stay just under the next bracket threshold. That approach lets you pay tax on the converted funds at your current, lower marginal rate instead of a steeper one down the road.

Six Reasons a Bridge Years Roth Conversion Pays Off

- Smaller Future RMDs: Converting funds shrinks the balance in your Traditional IRA. That directly lowers your future RMDs, which begin at age 73 or 75, meaning less taxable income later in life.

- Tax-Free Income in Retirement: Qualified withdrawals from a Roth IRA are entirely tax-free. That gives you a reliable income source that never adds to your tax bill.

- Possible Relief from Medicare IRMAA: Your Medicare IRMAA premiums are based on your Modified Adjusted Gross Income (MAGI) from two years prior. Lowering future taxable income through Roth conversions can help you sidestep higher Medicare Part B and D premiums.

- Lower Social Security Taxation: Less taxable income from RMDs can also shrink the portion of your Social Security benefits subject to federal income tax.

- Tax Diversification: Holding both pre-tax (Traditional IRA) and post-tax (Roth IRA) accounts gives you flexibility. You can pick which account to draw from based on where tax rates stand in the future.

- Estate Planning Advantages: Roth IRAs carry no RMDs for the original owner. Beneficiaries also receive tax-free withdrawals, which makes these accounts a strong tool for passing on wealth.

Key 2026 Figures You Need for Roth Conversions

Knowing the exact limits and thresholds for 2026 matters for effective retirement tax planning. These figures get adjusted for inflation every year.

Roth IRA Contribution Limits

- For individuals under age 50: $7,500.

- For individuals age 50 and older (catch-up contribution): $8,600 ($7,500 + $1,100 catch-up).

Roth IRA Income Phase-out Limits (Modified Adjusted Gross Income – MAGI)

- Single filers and Heads of Household: Phase-out begins at $153,000 and ends at $168,000.

- Married Filing Jointly: Phase-out begins at $242,000 and ends at $252,000.

Traditional IRA Contribution Limits

- Same as Roth IRA limits: $7,500 ($8,600 if 50 or older).

Traditional IRA Deduction Phase-out Limits (if covered by a workplace retirement plan)

- Single filers: Phase-out begins at $81,000 and ends at $91,000 MAGI.

- Married Filing Jointly (contributing spouse covered): Phase-out begins at $129,000 and ends at $149,000 MAGI.

401(k), 403(b), and 457(b) Contribution Limits

- Elective deferral limit: $24,500.

- Catch-up contribution (age 50 and older): $8,000.

- “Super catch-up” contribution (ages 60-63): $11,250.

- Note: For employees with FICA wages over $150,000 in the prior year, catch-up contributions in 2026 must be made as Roth (after-tax) contributions.

Essential 2026 Tax Figures for Retirees Over 65

These figures shape the broader tax environment that surrounds the Bridge Years strategy.

Required Minimum Distribution (RMD) Age

- For individuals born between 1951 and 1959: RMDs begin at age 73.

- For individuals born in 1960 or later: RMDs begin at age 75.

- You can delay your first RMD until April 1 of the year following the year you reach your RMD age. Doing so, however, means taking two RMDs in that subsequent year.

RMD Penalties

Missing a timely RMD triggers a penalty of 25% of the amount not withdrawn. That penalty drops to 10% if you correct it within two years.

Roth 401(k) RMDs

RMDs no longer apply to Roth 401(k) and Roth 403(b) plans. This change aligns them with Roth IRAs, effective January 1, 2024.

Standard Deduction (2026)

- Single filers: $16,100.

- Married Filing Jointly: $32,200.

- Head of Household: $24,150.

Additional Standard Deduction (Age 65 or Blind)

- Single filers: $2,050.

- Married Filing Jointly: $1,650 per qualifying spouse.

Temporary Senior Bonus Deduction (Age 65+)

- Single filers: Up to $6,000, phasing out for MAGI above $75,000.

- Married Filing Jointly: Up to $12,000, phasing out for MAGI above $150,000. This deduction runs through 2028.

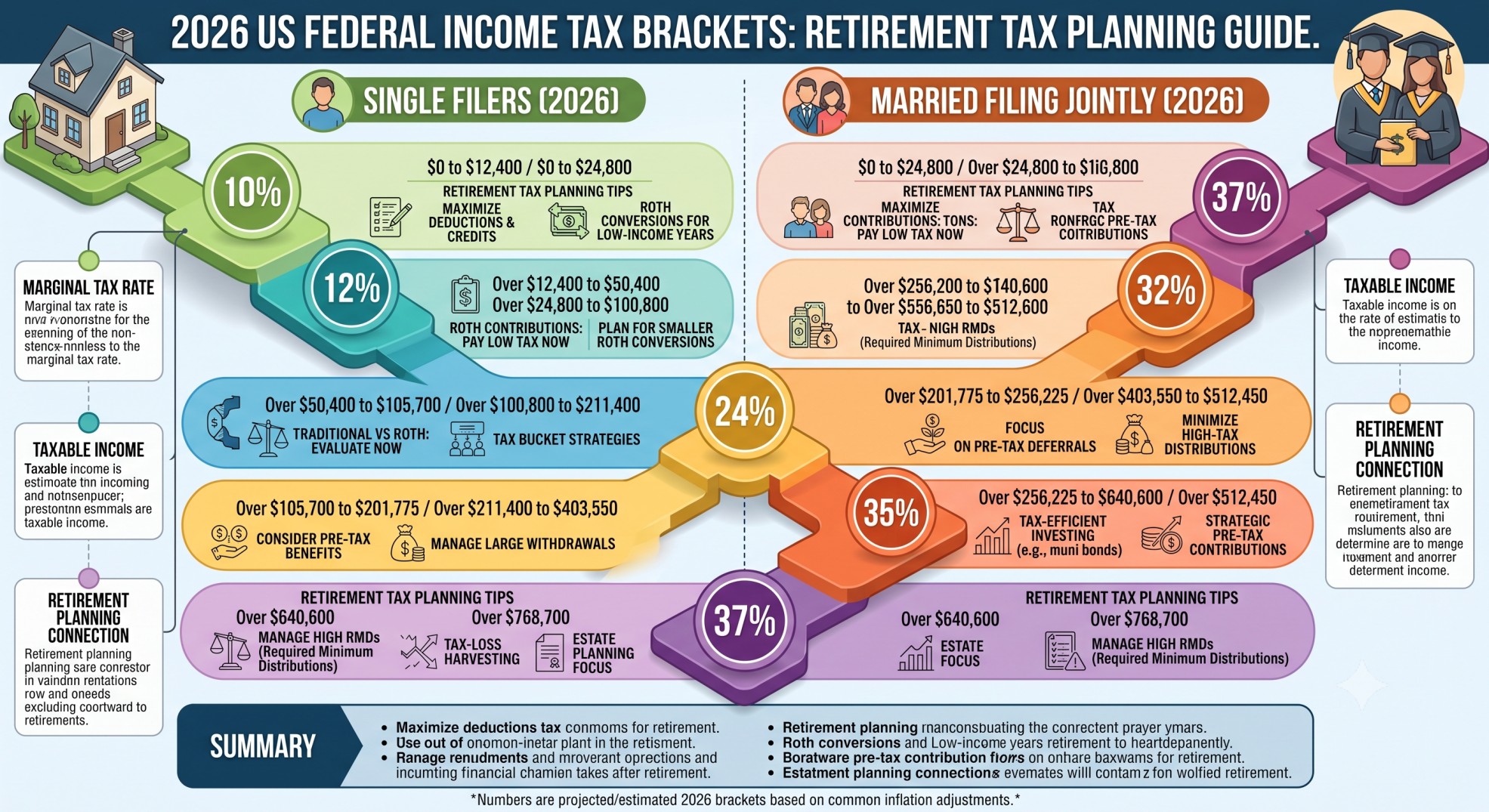

Federal Income Tax Brackets (2026)

The seven federal rates (10%, 12%, 22%, 24%, 32%, 35%, and 37%) stay in effect. Income thresholds get adjusted for inflation. The 12% tax bracket for single filers, for instance, extends up to $50,400, and up to $100,800 for married filing jointly.

Medicare Income-Related Monthly Adjustment Amount (IRMAA) Thresholds (2026)

IRMAA surcharges for Medicare Part B and Part D kick in once your MAGI, drawn from two years prior (your 2024 tax return for 2026 premiums), exceeds $109,000 for single filers. For married filing jointly, that threshold is $218,000. Five income brackets apply to IRMAA, with the highest tier starting at $500,000 for single filers or $750,000 for married filing jointly.

Social Security Benefit Taxation Thresholds (2026)

- Single filers: Up to 50% of benefits are taxable if combined income falls between $25,000 and $34,000. Up to 85% is taxable if combined income exceeds $34,000.

- Married Filing Jointly: Up to 50% of benefits are taxable if combined income falls between $32,000 and $44,000. Up to 85% is taxable if combined income exceeds $44,000.

Social Security Taxable Wage Base (2026)

The maximum earnings subject to Social Security tax is $184,500.

Real-World Case Study: Eleanor’s Bridge Year in California

Numbers make the Bridge Years strategy easier to picture. Here’s how a 2026 Roth conversion might play out for a real retiree.

The Persona

Eleanor, 63, lives in San Francisco and recently retired from her full-time career. She plans to start Social Security at age 67 and holds a Traditional IRA balance of $800,000. She’s looking for ways to boost her retirement income while trimming future tax burdens.

2026 Income and Deductions (Estimated)

Part-time Consulting Income: $30,000

Taxable Interest and Dividends: $5,000

Long-Term Capital Gains: $10,000 (from non-retirement investments)

Federal Standard Deduction (Single, under 65): $16,100

California Standard Deduction (Single): $5,400

Scenario A: No Roth Conversion (Baseline)

Eleanor takes no action on her Traditional IRA in this scenario. Her income comes solely from part-time work, investment income, and capital gains.

Total Gross Income: $45,000

Federal Taxable Ordinary Income: $18,900

Federal Income Tax: $2,036

California Taxable Income: $39,600

California State Tax: $976

Total Tax Liability: $3,012

Scenario B: Strategic Roth Conversion

Eleanor decides to put the Bridge Years strategy to work. She converts $27,700 from her Traditional IRA to a Roth IRA, and that amount gets added straight to her ordinary income.

Total Gross Income: $72,700 ($45,000 + $27,700 Roth Conversion)

Federal Taxable Ordinary Income: $46,600

Federal Income Tax: $6,432.50

California Taxable Income: $67,300

California State Tax: $2,884

Total Tax Liability: $9,316.50

Tax Cost of Conversion: Eleanor pays an additional $6,304.50 in 2026 because of the conversion ($9,316.50 minus $3,012).

Comparing the Two Scenarios

Converting $27,700 to a Roth IRA costs Eleanor an extra $6,304.50 in taxes for 2026. That might look like a steep upfront price. Long term, though, it delivers real payoffs:

- Future Tax-Free Growth and Withdrawals: The $27,700, plus every dollar it earns going forward, comes out of her Roth IRA completely tax-free in retirement, no matter where future tax rates land.

- Smaller Future RMDs: Her Traditional IRA balance now sits $27,700 lower. Her RMDs, which start at age 73, shrink accordingly, potentially keeping her in lower tax brackets later in retirement.

- Lower Future Taxable Income: Smaller RMDs mean less taxable income down the road, which can also ease the taxation of Social Security benefits and help hold down Medicare Part B premiums.

- Tax Rate Certainty: Eleanor paid tax on this $27,700 at her current, relatively low marginal federal rate (mostly 12%) and California rate (mostly 6-8%). She sidesteps the risk of paying at higher rates later.

Neither Alternative Minimum Tax (AMT), Net Investment Income Tax (NIIT), nor Section 199A (QBI) come into play at Eleanor’s income levels. Her MAGI stays well below the NIIT threshold, and she has no qualified business income for Section 199A purposes.

The Takeaway

Eleanor’s Bridge Years Roth conversion counts as a smart long-term financial move, even with an immediate tax cost of $6,304.50. Converting funds during a lower-income stretch locks in future tax-free income while cutting her exposure to higher tax rates and larger RMDs later in retirement. The move gives her more control over her future tax situation and sharpens the tax efficiency of her retirement savings overall.

Critical Considerations Before You Convert in 2026

The Bridge Years strategy carries real advantages, but several details deserve close attention before you act.

The 5-Year Rule for Roth Conversions

Each Roth conversion starts its own 5-year clock. If you’re under age 59½, the converted principal has to stay in the Roth IRA for five full calendar years to avoid a 10% early withdrawal penalty. This rule applies separately to the principal of every individual conversion.

The IRMAA Lookback Period

Medicare premiums for 2026 get calculated from your MAGI on your 2024 tax return. A large Roth conversion this year, in other words, could bump up your Medicare premiums in 2028. Timing conversions carefully, especially before Medicare enrollment, helps you fall outside that two-year lookback window.

Coordinating with Other Income Sources

Weigh all your income sources before planning a Roth conversion, including Social Security, pensions, and other investments. The goal is avoiding an accidental jump into a higher tax bracket, and preventing an unwanted increase in Social Security taxation along the way.

State Income Taxes on Conversions

Most states, California included, tax Roth conversion amounts. Factor this into your overall calculation, and check your own state’s specific rules before you convert.

Capital Gains Harvesting in the Bridge Years

Low-income Bridge Years also open the door to capital gains harvesting. This tactic involves selling appreciated investments to realize gains inside the 0% long-term capital gains tax bracket. For 2026, that bracket extends up to $49,450 for single filers and up to $98,900 for married couples.

Regulatory Landscape and What’s Ahead for 2026

Tax law shifts constantly. Recent legislation and ongoing IRS guidance both shape the environment surrounding retirement tax planning right now.

The Impact of SECURE Act 2.0

SECURE Act 2.0, passed in 2022, reshaped RMD ages significantly. It raised the age to 73 for those born between 1951 and 1959, and moved it to 75 for anyone born in 1960 or later. The act also eliminated RMDs for Roth 401(k)s, bringing them in line with Roth IRAs.

TCJA Sunsetting Provisions (Post-2025)

Several provisions of the Tax Cuts and Jobs Act (TCJA) are scheduled to expire after 2025, with potential effects on tax brackets and the Standard Deduction. Future tax rates could climb as a result, which makes a 2026 Roth conversion even more appealing right now.

Ongoing IRS Guidance

The IRS keeps issuing guidance on retirement plan rules. IRS Announcement 2026-7, for example, points to a further delay, pushing back the applicability date for certain portions of upcoming final RMD regulations until at least January 1, 2027. This reflects the ongoing fine-tuning of SECURE Act 2.0.

Conclusion: Take Control of Your Retirement Tax Future

The Bridge Years strategy stands out as an effective approach to retirement tax planning for anyone over 65. Converting pre-tax funds to a Roth IRA during a lower-income stretch cuts your future tax burden, creates a stream of tax-free income, and can ease Medicare premiums along the way.

Why Professional Guidance Still Matters

Tax law stays complex and shifts often, and your own financial picture is unique to you. A qualified tax professional or financial advisor can weigh your specific numbers and tailor advice to your situation, walking you through exactly how the Bridge Years strategy might fit your plan.

Managing Your Tax Future Starts Now

Smart retirement tax planning helps you make informed choices and strengthen your financial future. Weigh whether the Bridge Years strategy lines up with your retirement goals, and start managing your tax situation today rather than waiting until RMDs force your hand.

Visit the IRS website for more information on current tax rules.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.