Every percentage point of return matters if you’re a high-net-worth investor. Every percentage point lost to taxes matters just as much.

The choice between an Exchange Traded Fund (ETF) and a traditional mutual fund goes far beyond investment strategy under 2026’s tax rules. That choice directly shapes your after-tax wealth. A hidden cost known as “tax drag” can quietly chip away at your portfolio year after year, and most investors never realize how much fund structure alone is costing them.

Sophisticated investors need a clear grasp of these structural differences for effective tax planning 2026. This guide breaks down how mutual fund tax drag stacks up against ETF tax efficiency, using real numbers from a California-based couple’s actual 2026 tax situation.

⚡ Executive Summary: ETF vs. Mutual Fund Tax Drag for 2026

- Tax drag quietly reduces investment returns through dividends and capital gains taxed before you even sell, and fund structure largely determines how much drag you face.

- Mutual funds often create “phantom income” by distributing taxable capital gains even when you haven’t sold a single share, leading to significant capital gains distributions.

- ETFs rely on an in-kind creation and redemption process under IRC Section 852(b)(6) that minimizes taxable distributions and defers taxes until you personally sell.

- HNWIs face a top federal long-term capital gains rate of 20%, a 3.8% Net Investment Income Tax, and state rates as high as 13.3% in California.

- A California couple with a $10 million portfolio saved $55,650 in annual taxes simply by holding a tax-efficient ETF instead of an actively managed mutual fund.

- Asset location, tax-loss harvesting, and vehicle selection all play a role in preserving after-tax wealth, and a qualified tax advisor should confirm strategies for your specific situation.

Table of Contents

- What Is Tax Drag and Why It Quietly Costs You Money

- How Mutual Funds Generate Taxable Distributions Every Year

- Why ETFs Are Structurally Built for Tax Efficiency

- Tax Rates and Thresholds HNWIs Must Watch in 2026

- Case Study: How Much Tax Do the Sterlings Save With an ETF?

- Portfolio Strategies That Reduce Your Tax Drag

- Advanced Moves: Asset Location, Charitable Giving, and Estate Planning

- The Bottom Line for 2026 Tax Planning

What Is Tax Drag and Why It Quietly Costs You Money

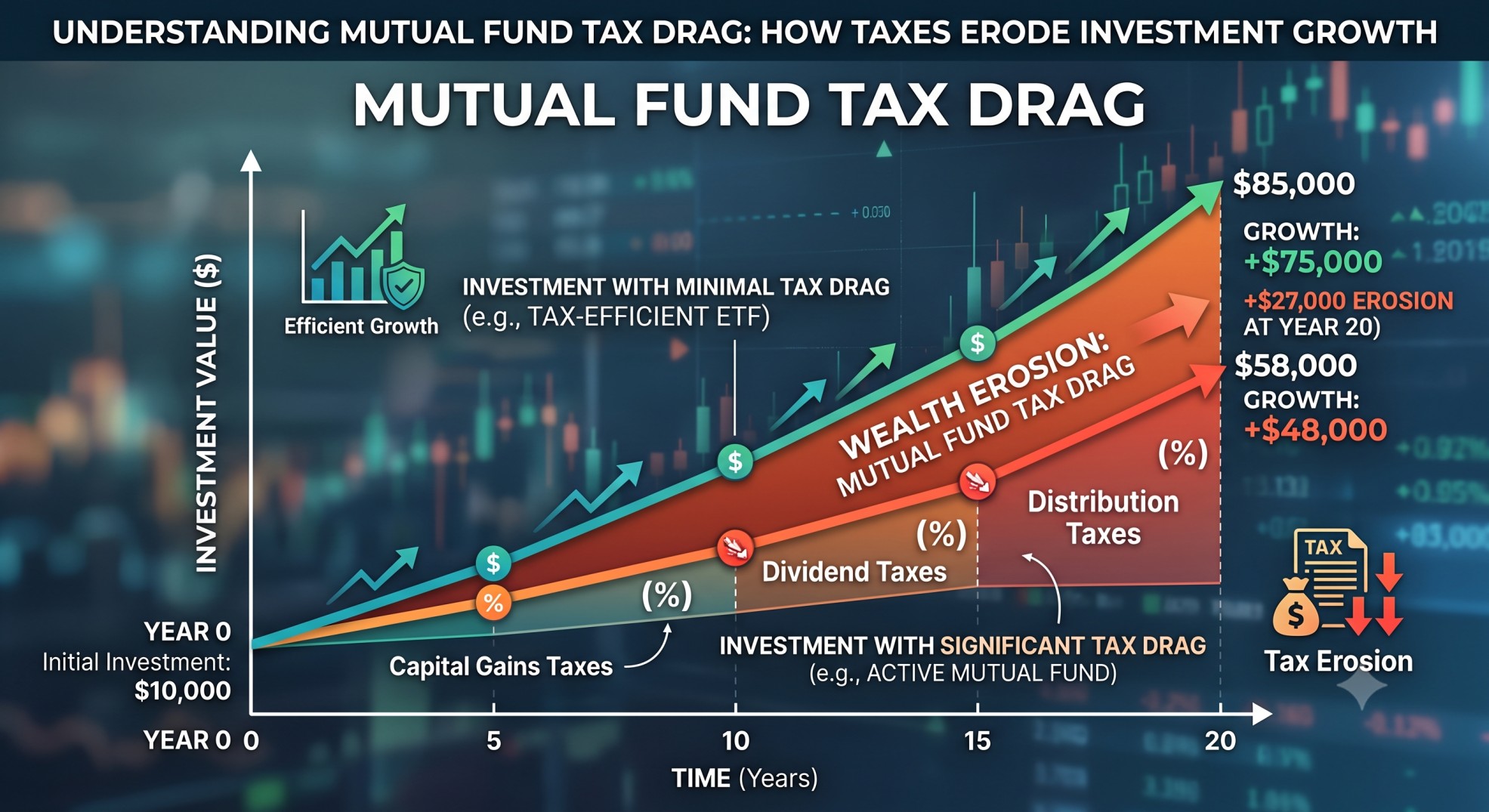

Tax drag is the reduction in your investment returns caused by taxes on income, dividends, and capital gains before you ever sell a single share. It erodes your wealth silently, year after year, without any action on your part.

Fund structure plays a massive role in how much tax liability gets triggered along the way. Some structures generate far more taxable events than others, and that gap shows up directly in your after-tax return. HNWIs feel this pain more than most investors, since they already sit at the highest marginal federal and state tax brackets and often owe the Net Investment Income Tax on top of everything else.

Every dollar lost to unnecessary taxes stops compounding for you. That single fact makes minimizing tax drag one of the most valuable, and most overlooked, parts of wealth management.

How Mutual Funds Generate Taxable Distributions Every Year

Traditional mutual funds pool money from many investors and hand active buying and sell decisions to a professional manager. That active trading routinely creates internal capital gains inside the fund.

Redemptions make the problem worse. When other investors cash out, the fund may need to sell appreciated holdings just to raise the cash, triggering gains that get passed along to every remaining shareholder. This is the primary driver of mutual fund tax drag.

Phantom income results from this exact mechanism. You end up owing tax on distributions even if the fund’s overall value dropped that year, or even if you never sold a single share yourself. These distributions arrive as qualified dividends, non-qualified dividends, short-term capital gains, and long-term capital gains, all taxable in the year you receive them. IRC Sections 851-855 govern how Regulated Investment Companies must pass through this income to shareholders in order to avoid tax at the corporate level, and understanding that rule explains why mutual fund investors so often get surprised at tax time.

Why ETFs Are Structurally Built for Tax Efficiency

ETFs avoid most of this problem through a mechanism called in-kind creation and redemption. Large institutional players known as Authorized Participants can redeem ETF shares by receiving actual securities from the fund instead of cash, a process permitted under IRC Section 852(b)(6).

That in-kind transfer lets the ETF hand off its lowest-basis, most appreciated securities directly to the Authorized Participant. No sale happens on the open market, so no taxable event gets created for the fund or for shareholders who stayed put.

Fewer forced sales mean fewer capital gains distributions land on your tax return each year. Tax realization gets deferred until you decide to sell your own ETF shares, giving you far more control over timing. That control, more than anything else, defines ETF tax efficiency and explains why it matters so much for HNWIs trying to manage phantom income.

Tax Rates and Thresholds HNWIs Must Watch in 2026

Several federal and state thresholds shape how much tax drag actually costs a high-net-worth household in 2026. Here are the numbers that matter most.

- Federal Long-Term Capital Gains (LTCG) and Qualified Dividend Rates: The top federal rate sits at 20% for single filers with taxable income over $545,500 and married filing jointly over $613,700.

- Net Investment Income Tax (NIIT): An additional 3.8% applies to investment income once Modified Adjusted Gross Income (AGI) passes $250,000 for married filing jointly.

- State Income Tax Considerations: States like California impose steep marginal rates, topping out at 13.3% (including the mental health surcharge) for income above $1,350,000 (MFJ).

- SALT Deduction Cap: The federal deduction for State and Local Taxes stays capped at $10,000, hitting HNWIs in high-tax states especially hard.

- Alternative Minimum Tax (AMT): The AMT exemption phases out once Alternative Minimum Taxable Income (AMTI) crosses $1,000,000 for married couples filing jointly.

- Section 199A (QBI) Deduction: High-income earners typically see this deduction fully phased out.

Case Study: How Much Tax Do the Sterlings Save With an ETF?

Mr. and Mrs. Sterling save $55,650 a year in taxes by holding a tax-efficient ETF instead of an actively managed mutual fund, based on their 2026 California tax situation. Here’s exactly how that number gets built.

Persona Profile: Mr. and Mrs. Sterling

Mr. and Mrs. Sterling file jointly and live in California. Their 2026 profile looks like this.

- Filing Status: Married Filing Jointly (MFJ)

- Location: California

- Base Adjusted Gross Income (AGI): $1,500,000 (from salaries, business income, etc.)

- Investment Portfolio Value: $10,000,000

- Non-SALT Itemized Deductions: $150,000 (mortgage interest, charitable contributions)

Two Scenarios, One $10 Million Portfolio

Both scenarios assume a 2% annual qualified dividend yield on the full $10,000,000 equity portfolio.

Scenario 1, Actively Managed Mutual Fund: Active trading and shareholder redemptions push out 2% of NAV annually as long-term capital gains.

- Annual Qualified Dividends: $200,000

- Annual Distributed Long-Term Capital Gains: $200,000

Scenario 2, Tax-Efficient ETF: The in-kind redemption mechanism keeps distributed gains far lower.

- Annual Qualified Dividends: $200,000

- Annual Distributed Long-Term Capital Gains: $50,000

Key 2026 Tax Assumptions Used

- Federal Income Tax: Progressive brackets up to 37% on ordinary income.

- LTCG and Qualified Dividends: Taxed at the top federal rate of 20%.

- NIIT: 3.8% on investment income above $250,000 (MFJ).

- California State Tax: Progressive brackets topping out at 13.3% (including the 1% mental health surcharge) above $1,350,000 (MFJ).

- SALT Cap: Capped at $10,000.

- AMT: Regular tax liability is assumed to exceed any potential AMT liability at this income and deduction level.

- Section 199A: Fully phased out given the Sterlings’ Adjusted Gross Income (AGI).

Mutual Fund Tax Bill

- Total AGI: $1,900,000.00 ($1,500,000 base + $200,000 qualified dividends + $200,000 LTCG distributions)

- Federal Income Tax: $499,360.00

- NIIT: $15,200.00

- California State Tax: $204,795.00

- Total Annual Tax Liability: $719,355.00

ETF Tax Bill

- Total AGI: $1,750,000.00 ($1,500,000 base + $200,000 qualified dividends + $50,000 LTCG distributions)

- Federal Income Tax: $469,360.00

- NIIT: $9,500.00

- California State Tax: $184,845.00

- Total Annual Tax Liability: $663,705.00

The savings: $719,355.00 minus $663,705.00 equals $55,650.00 in annual tax savings, purely from choosing the ETF structure.

This gap comes almost entirely from the difference in distributed capital gains between the two vehicles. It’s the tax drag imposed by the mutual fund’s less efficient structure, and it repeats every single year the Sterlings hold that fund.

Portfolio Strategies That Reduce Your Tax Drag

The Sterling numbers point to a clear strategic lesson. Prioritizing tax-efficient vehicles inside your taxable accounts matters enormously, and ETFs with their lower capital gains distributions typically make sense as core holdings for reducing mutual fund tax drag.

Tax-loss harvesting becomes far easier with ETFs, since intra-day trading lets you sell a losing position and immediately buy a similar, but not “substantially identical,” ETF to avoid the wash sale rule. Actively managed ETFs deserve a look too, since many now use the same in-kind redemption mechanism as index ETFs, giving you active management alongside genuine ETF tax efficiency.

Not every ETF earns that efficiency label, though. Commodity ETFs, leveraged ETFs, and certain international ETFs carry different tax treatment entirely, so careful selection still matters for solid tax planning 2026.

Advanced Moves: Asset Location, Charitable Giving, and Estate Planning

Asset location ranks among the most powerful strategies available to sophisticated investors. Tax-inefficient holdings, such as actively managed mutual funds or high-dividend stocks, belong in tax-advantaged accounts like IRAs or 401(k)s, while tax-efficient ETFs work better in taxable brokerage accounts where their structural advantage actually counts.

Charitable giving adds another lever. Donating appreciated securities directly to a charity avoids capital gains tax entirely, while still giving you a deduction based on the fair market value of those assets.

Estate planning ties into all of this too. Heirs who inherit low-basis, tax-efficient ETFs typically receive a “step-up in basis” at your death, wiping out capital gains on the appreciation that built up during your lifetime. These layered strategies strengthen wealth preservation and belong in any serious tax planning 2026 conversation.

The Bottom Line for 2026 Tax Planning

ETFs carry a real structural edge over mutual funds for high-net-worth investors heading into 2026. Fewer capital gains distributions and less phantom income translate directly into ETF tax efficiency you can measure in dollars, not just theory.

Annual savings compound fast. The Sterling case study shows a $55,650 yearly gap from vehicle choice alone, money that keeps growing instead of disappearing to the IRS and California’s Franchise Tax Board.

Structure clearly is not just an academic distinction here. It shapes your bottom line directly, and it deserves serious weight in your tax planning 2026 decisions. IRS Publication 550, Investment Income and Expenses, offers additional technical detail on how investment income gets taxed if you want to dig deeper.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.