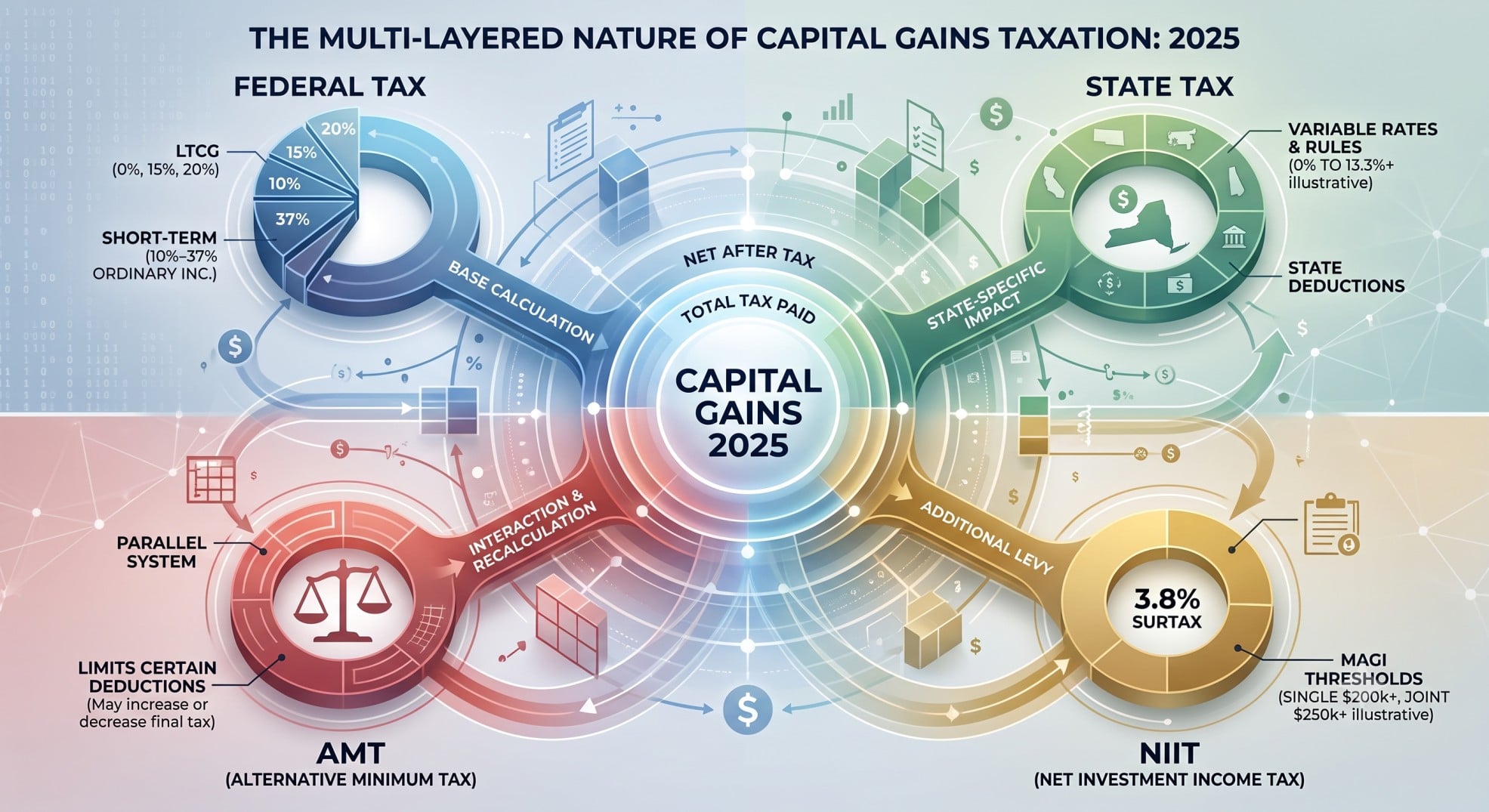

For High-Net-Worth Individuals, capital gains are not merely subject to a single federal rate. The 2025 tax year involves a complex mix of federal, state, and specialized taxes that can dramatically alter your effective tax rate. Understanding these advanced strategies is not just about compliance; it’s about preserving wealth. This guide explains the multi-layered capital gain tax 2025 calculations, revealing critical factors that demand your attention and strategic planning. We will also examine the impact of the Net Investment Income Tax and the Alternative Minimum Tax.

Executive Summary

- The 2025 capital gain tax involves federal, state, Net Investment Income Tax (NIIT), and Alternative Minimum Tax (AMT) considerations.

- Short-term capital gains are taxed at ordinary income rates, while long-term capital gains benefit from preferential rates (0%, 15%, 20%).

- The 3.8% Net Investment Income Tax applies to investment income for individuals exceeding specific Modified Adjusted Gross Income (MAGI) thresholds.

- The Alternative Minimum Tax (AMT) can significantly increase the tax burden for high earners, overriding some regular tax benefits.

- State taxes, like California’s progressive rates, add another layer of complexity to capital gains taxation.

- Strategic planning, including tax-loss harvesting and charitable giving, is vital for mitigating capital gain tax impact.

Introduction: Understanding Capital Gains for HNWIs in 2025

Capital gains taxation is very important for high-net-worth individuals (HNWIs). Indeed, these individuals often have substantial investment portfolios. The 2025 tax year has a multi-layered approach to taxing these gains. This includes federal rates, state-specific rules, the Net Investment Income Tax (NIIT), and the Alternative Minimum Tax (AMT). Therefore, advanced planning is necessary. This comprehensive guide will help you understand the details of the capital gain tax 2025.

Understanding the Fundamentals: Short-Term vs. Long-Term Capital Gains

Defining Capital Assets and Holding Periods

The Internal Revenue Code (IRC) defines what constitutes a capital asset. According to IRC Section 1221, most property held for personal use or investment qualifies. This includes stocks, bonds, and real estate. Also, the holding period for these assets is crucial. IRC Section 1222 distinguishes between short-term and long-term assets. Short-term assets are held for one year or less. Conversely, long-term assets are held for more than one year.

Short-Term Capital Gains (STCG) Taxation

Short-term capital gains are taxed as ordinary income. As a result, they are subject to your marginal federal income tax rates. For 2025, these rates range from 10% to 37%. For example, a married couple filing jointly will see the 10% rate apply up to $23,850. The top 37% rate applies to income of $751,601 or more. Single filers face a 10% rate up to $11,925 and a 37% rate for income of $626,351 or more.

Long-Term Capital Gains (LTCG) Preferential Rates

Long-term capital gains generally receive preferential tax treatment. These rates are 0%, 15%, or 20%. The specific rate depends on your taxable income and filing status. For instance, the 0% rate applies to lower income thresholds. The 20% rate applies to the highest income brackets. This preferential treatment is a key aspect of the long-term capital gains system.

Here are the 2025 income thresholds for long-term capital gains rates:

- 0% Rate:

- Single: Taxable income up to $48,350

- Married Filing Jointly: Taxable income up to $96,700

- Head of Household: Taxable income up to $64,750

- Married Filing Separately: Taxable income up to $48,350

- 15% Rate:

- Single: Taxable income between $48,351 and $533,400

- Married Filing Jointly: Taxable income between $96,701 and $600,050

- Head of Household: Taxable income between $64,751 and $566,700

- Married Filing Separately: Taxable income between $48,351 and $300,000

- 20% Rate:

- Single: Taxable income exceeding $533,400

- Married Filing Jointly: Taxable income exceeding $600,050

- Head of Household: Taxable income exceeding $566,700

- Married Filing Separately: Taxable income exceeding $300,000

Beyond the Basics: Special Capital Gains Considerations for HNWIs

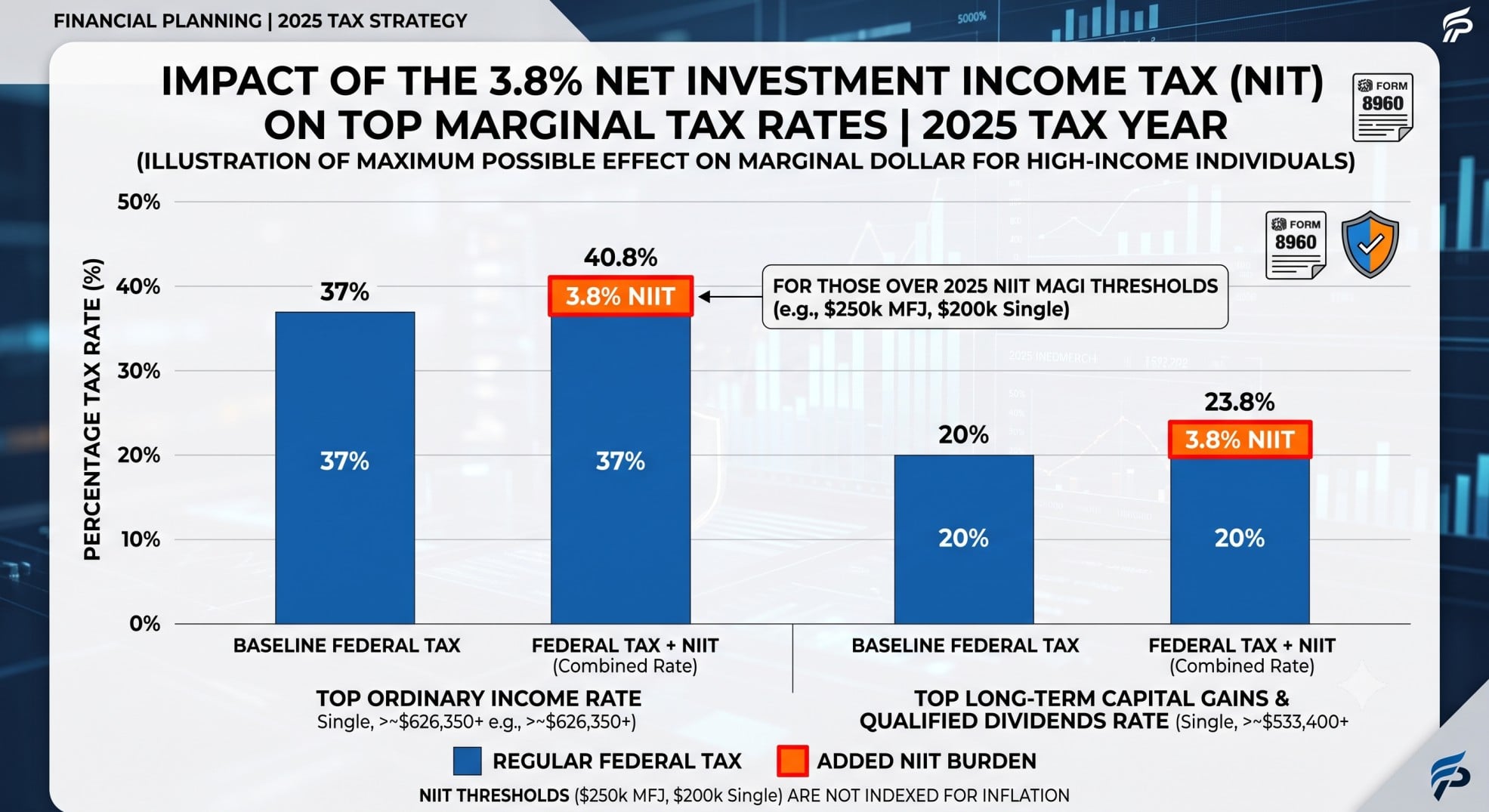

The Net Investment Income Tax (NIIT) – IRC Section 1411

An additional 3.8% Net Investment Income Tax (NIIT) applies to certain investment income. This tax affects individuals, estates, and trusts. It applies when their Modified Adjusted Gross Income (MAGI) exceeds specific thresholds. For 2025, these thresholds are: $200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately. The NIIT applies to the lesser of net investment income or the amount by which MAGI exceeds the threshold. This tax can increase the effective top capital gains rate to 23.8% (20% + 3.8%) for long-term capital gains. It can also reach up to 40.8% (37% + 3.8%) for short-term gains.

Qualified Dividends: Taxed Like LTCG

Qualified dividends are taxed at the same preferential rates as long-term capital gains. These rates are 0%, 15%, or 20%. The specific rate depends on the taxpayer’s income and filing status. To qualify, dividends must meet specific IRS criteria. This includes a minimum holding period for the stock. Therefore, understanding these criteria is important for tax planning.

Special Asset Categories and Their Tax Treatment

- Collectibles: Net capital gains from selling collectibles (e.g., art, stamps, coins) held for over one year are taxed at a maximum rate of 28%. Short-term gains on collectibles are taxed at ordinary income rates.

- Section 1250 Unrecaptured Gain: A portion of the gain from selling Section 1250 real property is attributable to depreciation. This portion is taxed at a maximum rate of 25%. This applies to depreciation claimed in excess of straight-line depreciation.

- Qualified Small Business Stock (QSBS) – IRC Section 1202: The taxable part of a gain from selling Section 1202 qualified small business stock is taxed at a maximum 28% rate. However, certain exclusions may apply.

Capital Loss Limitations and Carryovers

If capital losses exceed capital gains, taxpayers can deduct up to $3,000 of the excess loss against ordinary income each year. This limit is $1,500 if married filing separately. Any remaining capital loss can be carried forward to future tax years. This strategy, known as tax-loss harvesting, is a key planning tool.

The Alternative Minimum Tax (AMT): A Parallel System for High Earners

What is AMT and Why it Matters for HNWIs

The Alternative Minimum Tax (AMT) ensures high-income individuals pay a minimum tax. It acts as a parallel tax system. The AMT can negate some regular tax benefits. Therefore, it is a significant consideration for HNWIs. Understanding its impact is crucial for accurate tax projections for the capital gain tax 2025.

Key AMT Adjustments and Preferences

Several adjustments and preferences can trigger the AMT. A common one is the add-back of state and local tax (SALT) deductions. Other common adjustments relevant to HNWIs include certain accelerated depreciation and incentive stock options. These items are treated differently under AMT rules compared to regular tax rules.

Calculating AMT for 2025

Calculating AMT involves specific exemption amounts and phase-out thresholds. The AMT rates are 26% and 28%. Taxpayers pay the higher of their regular tax liability or their Tentative Minimum Tax (TMT).

State-Specific Capital Gains Taxation: The California Example

General Principles of State Capital Gains Taxation

Most states tax capital gains as ordinary income. However, some states have no income tax, which can be advantageous. Conversely, high-tax states can significantly increase the overall tax burden. Therefore, state residency plays a large role in total tax liability.

Deep Dive: California’s Impact on Capital Gains

California has progressive income tax rates. These rates can go up to 13.3% for high earners. Capital gains are treated as ordinary income at the state level in California. Furthermore, California imposes a 1% mental health surcharge on taxable income over $1,000,000. This results in a significant combined federal and state burden for California residents. Consequently, California HNWIs face one of the highest effective capital gain tax rates in the nation.