⚡ Executive Summary: 2026 Tax Brackets and Rates

- The standard deduction for 2026 increases to $16,100 for single filers and $32,200 for married couples filing jointly.

- The top marginal tax rate remains 37% for single filers earning over $640,600 and married couples earning over $768,700.

- Retirement contribution limits have increased, allowing up to $24,500 for 401(k)s and $7,500 for IRAs in 2026.

- The annual gift tax exclusion rises to $19,000 per recipient for the 2026 tax year.

Table of Contents

- How Do Tax Brackets Work?

- What Are the Tax Brackets for 2026?

- 2026 Standard Deduction and Personal Exemption

- How To Calculate Your Federal Income Tax Bracket

- 2026 Capital Gains Tax Rates and Brackets

- Key Tax Deductions and Credits for 2026

- Retirement Contribution Limits (2026)

- Potential Ways to Get Into a Lower Tax Bracket

- Other Notable 2026 Tax Provisions

- Frequently Asked Questions About 2026 Taxes

Understanding the tax brackets 2026 is the foundation of smart financial planning. The IRS adjusts these figures annually to account for inflation, meaning the income thresholds for each bracket shift slightly every year. If your income stayed exactly the same from last year, these inflation adjustments might actually drop a portion of your income into a lower bracket.

We’ve compiled the official federal income tax brackets 2026, standard deductions, and capital gains rates so you can accurately project your tax liability. And we’ll show you exactly how the math works.

How Do Tax Brackets Work?

The United States uses a progressive tax system. That means you don’t pay a single flat rate on your entire income. Instead, your income is divided into chunks, and each chunk is taxed at a progressively higher rate.

Many taxpayers misunderstand this concept. They assume that moving into a higher tax bracket means all their income is suddenly taxed at that higher rate. That simply isn’t true. Only the specific dollars that fall inside that higher bracket are taxed at the higher rate.

What Is a Marginal Tax Rate?

Your marginal tax rate is the highest tax bracket that your last dollar of income falls into. If you are a single filer with $110,000 of taxable income in 2026, your marginal rate is 24%. But you are not paying 24% on the entire $110,000. You only pay 24% on the income that exceeds the 24% threshold ($105,700).

What Is an Effective Tax Rate?

Your effective tax rate is the actual percentage of your total income that you pay in taxes. You calculate this by dividing your total tax bill by your total taxable income. Because the lower portions of your income are taxed at 10% and 12%, your effective tax rate will always be significantly lower than your marginal tax rate.

What Are the Tax Brackets for 2026?

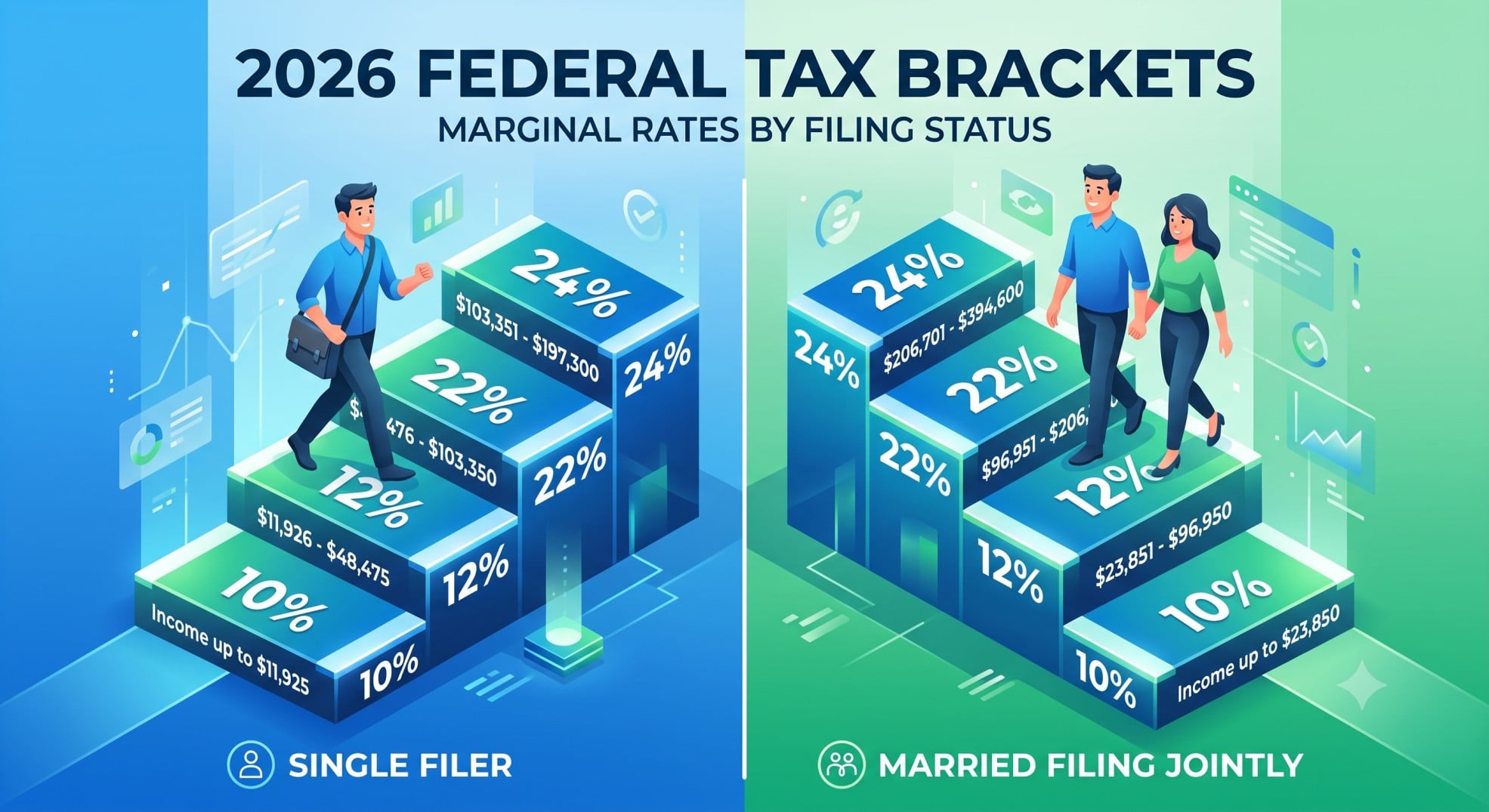

The IRS has released the official 2026 tax tables. There are seven federal income tax brackets 2026: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Your filing status dictates the income ranges for each of these percentages.

Below are the official 2026 income tax brackets for the four primary filing statuses.

2026 Single Filer Tax Brackets

The 2026 single filer tax brackets apply to unmarried individuals who do not qualify for Head of Household status.

| Tax Rate | Taxable Income Bracket |

|---|---|

| 10% | $0 to $12,400 |

| 12% | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 |

| 35% | $256,226 to $640,600 |

| 37% | $640,601 or more |

2026 Married Filing Jointly Tax Brackets

The 2026 married filing jointly tax brackets offer the widest income bands, allowing couples to earn more before hitting higher marginal rates. These brackets also apply to qualifying surviving spouses.

| Tax Rate | Taxable Income Bracket |

|---|---|

| 10% | $0 to $24,800 |

| 12% | $24,801 to $100,800 |

| 22% | $100,801 to $211,400 |

| 24% | $211,401 to $403,550 |

| 32% | $403,551 to $512,450 |

| 35% | $512,451 to $768,700 |

| 37% | $768,701 or more |

2026 Head of Household Tax Brackets

To use the 2026 head of household tax brackets, you must be unmarried, pay for more than half the costs of keeping up a home, and have a qualifying dependent living with you for more than half the year.

| Tax Rate | Taxable Income Bracket |

|---|---|

| 10% | $0 to $17,700 |

| 12% | $17,701 to $67,450 |

| 22% | $67,451 to $105,700 |

| 24% | $105,701 to $201,750 |

| 32% | $201,751 to $256,200 |

| 35% | $256,201 to $640,600 |

| 37% | $640,601 or more |

2026 Married Filing Separately Tax Brackets

The 2026 married filing separately tax brackets mirror the single filer brackets up to the 35% rate. Couples often choose this status to separate tax liability or to optimize income-driven student loan repayment plans.

| Tax Rate | Taxable Income Bracket |

|---|---|

| 10% | $0 to $12,400 |

| 12% | $12,401 to $50,400 |

| 22% | $50,401 to $105,700 |

| 24% | $105,701 to $201,775 |

| 32% | $201,776 to $256,225 |

| 35% | $256,226 to $384,350 |

| 37% | $384,351 or more |

Read more about choosing the right filing status for your situation.

2026 Standard Deduction and Personal Exemption

Before you apply the tax brackets 2026 to your income, you get to subtract deductions. Most taxpayers take the standard deduction rather than itemizing. The 2026 Standard Deduction and Personal Exemption rules remain shaped by the Tax Cuts and Jobs Act (TCJA), meaning personal exemptions are still suspended at $0.

The standard deduction for 2026 has increased to combat inflation:

- Single: $16,100

- Married Filing Jointly: $32,200

- Head of Household: $24,150

- Married Filing Separately: $16,100

If you are blind or age 65 or older, you get an additional standard deduction. For married taxpayers, the additional amount is $1,650. For unmarried taxpayers who are not surviving spouses, the additional amount is $2,050.

How To Calculate Your Federal Income Tax Bracket

To figure out exactly what you owe, you need to calculate your taxable income first. You take your gross income, subtract any above-the-line deductions (like traditional IRA contributions), and then subtract either the standard deduction for 2026 or your itemized deductions.

Once you have your taxable income, you push it through the federal income tax brackets 2026 step by step. Let’s look at two real-world examples.

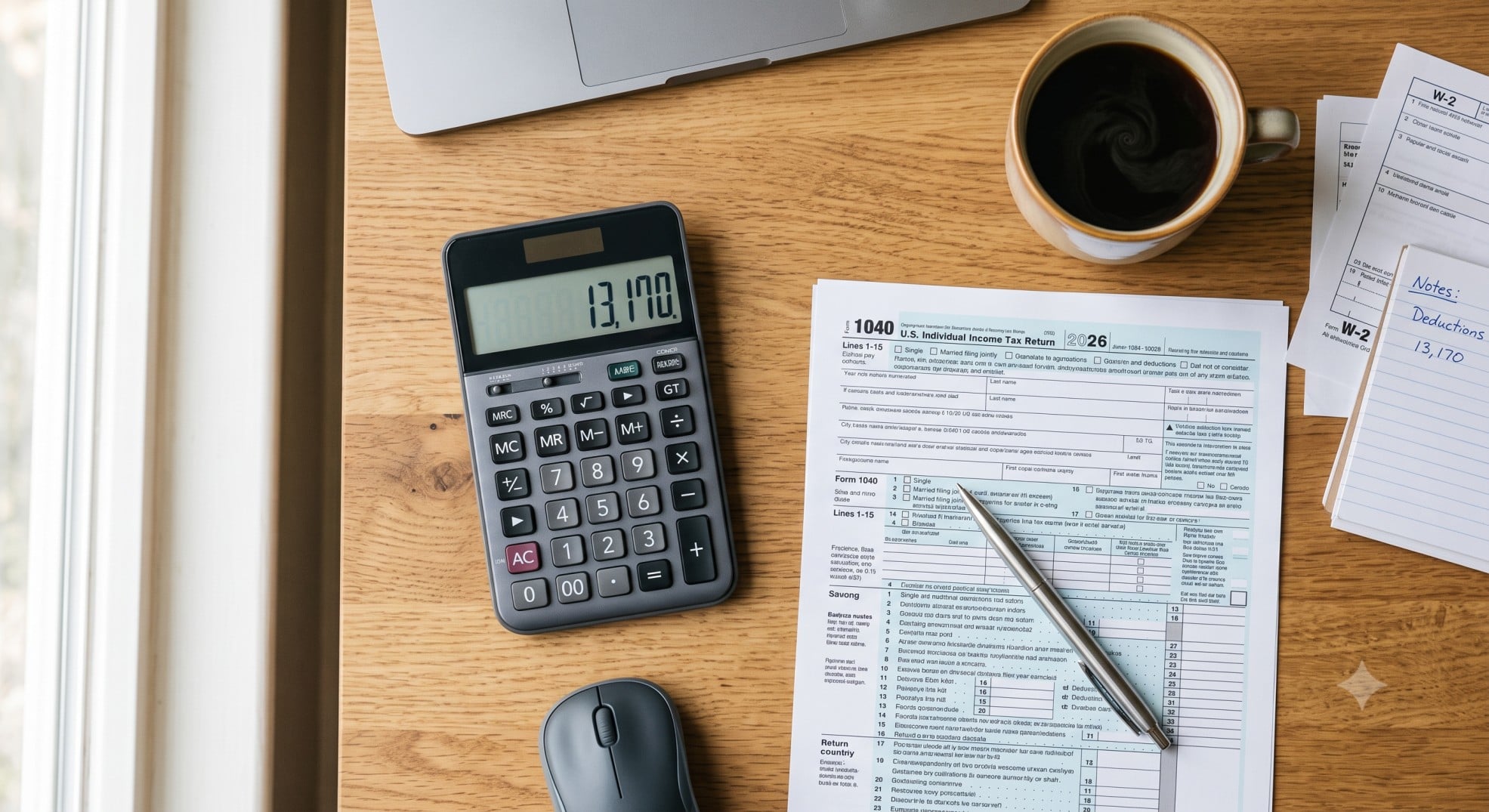

Example 1: Single Filer Calculation

David is a single filer. His gross income in 2026 is $100,000. He takes the standard deduction for 2026 of $16,100. His taxable income is $83,900.

Here is how David’s tax is calculated using the 2026 single filer tax brackets:

- 10% Bracket: The first $12,400 is taxed at 10%. ($12,400 x 0.10 = $1,240)

- 12% Bracket: Income from $12,401 to $50,400 ($38,000 total) is taxed at 12%. ($38,000 x 0.12 = $4,560)

- 22% Bracket: The remaining income from $50,401 to $83,900 ($33,500 total) is taxed at 22%. ($33,500 x 0.22 = $7,370)

David’s total federal income tax liability is $1,240 + $4,560 + $7,370 = $13,170.

His marginal tax rate is 22%, but his effective tax rate is just 13.17% ($13,170 divided by $100,000).

Example 2: Married Filing Jointly Calculation

Sarah and Mark are married and file jointly. Their combined gross income is $250,000. They take the $32,200 standard deduction. Their taxable income is $217,800.

Here is how their tax is calculated using the 2026 married filing jointly tax brackets:

- 10% Bracket: The first $24,800 is taxed at 10%. ($24,800 x 0.10 = $2,480)

- 12% Bracket: Income from $24,801 to $100,800 ($76,000 total) is taxed at 12%. ($76,000 x 0.12 = $9,120)

- 22% Bracket: Income from $100,801 to $211,400 ($110,600 total) is taxed at 22%. ($110,600 x 0.22 = $24,332)

- 24% Bracket: The remaining income from $211,401 to $217,800 ($6,400 total) is taxed at 24%. ($6,400 x 0.24 = $1,536)

Their total federal income tax liability is $2,480 + $9,120 + $24,332 + $1,536 = $37,468.

2026 Capital Gains Tax Rates and Brackets

Ordinary income tax brackets 2026 apply to wages, salaries, and interest. But if you sell an investment held for more than one year, you trigger long-term capital gains. The 2026 Capital Gains Tax Rates and Brackets are highly favorable compared to ordinary income rates.

For 2026, the long-term capital gains rates are 0%, 15%, or 20%, depending on your taxable income.

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 |

| 20% | Over $545,500 | Over $613,700 |

Example 3: Stacking Capital Gains on Ordinary Income

Capital gains sit on top of your ordinary income. Let’s say Maria is a single filer. She has $60,000 in ordinary gross income and a $20,000 long-term capital gain. She takes the $16,100 standard deduction for 2026.

Her taxable ordinary income is $43,900 ($60,000 – $16,100). Because her ordinary income fills up the space below the $49,450 threshold for the 0% capital gains bracket, she still has $5,550 of “room” left in the 0% bracket ($49,450 – $43,900).

So, the first $5,550 of her $20,000 capital gain is taxed at 0%. The remaining $14,450 of her capital gain spills over into the 15% bracket. She pays $2,167.50 in capital gains tax.

Learn more about tax-loss harvesting to offset capital gains.

Key Tax Deductions and Credits for 2026

Deductions lower your taxable income, while credits reduce your actual tax bill dollar-for-dollar. Here are the major figures you need to know for 2026.

2026 Child Tax Credit

The 2026 Child Tax Credit provides up to $2,200 per qualifying child. The credit begins to phase out for married couples filing jointly with a Modified Adjusted Gross Income (MAGI) over $400,000, and $200,000 for all other filers.

2026 Earned Income Tax Credit

The 2026 Earned Income Tax Credit (EITC) is a refundable credit designed for low-to-moderate-income working individuals and couples. The exact credit amount depends on your income and the number of qualifying children you have. The IRS adjusts the maximum credit amounts and phase-out thresholds annually for inflation.

Student Loan Interest Deduction (2026)

The Student Loan Interest Deduction for 2026 allows you to deduct up to $2,500 of interest paid on qualified student loans. This is an above-the-line deduction, meaning you can claim it even if you take the standard deduction. It is subject to income phase-outs.

SALT Deduction Limit (2026)

The State and Local Tax (SALT) deduction allows taxpayers who itemize to deduct certain taxes paid to state and local governments. The SALT Deduction Limit for 2026 remains capped at $10,000 ($5,000 if married filing separately) under current law.

2026 Qualified Business Income Deduction

Self-employed individuals and small business owners can utilize the 2026 Qualified Business Income Deduction (QBID). This allows eligible taxpayers to deduct up to 20% of their qualified business income from a pass-through entity, subject to taxable income thresholds and limitations based on W-2 wages paid by the business.

Retirement Contribution Limits (2026)

Contributing to pre-tax retirement accounts is one of the most powerful ways to reduce your taxable income and drop into lower federal income tax brackets 2026.

The IRS has increased the limits for 2026:

- 401(k), 403(b), and most 457 plans: The base contribution limit is $24,500. If you are age 50 or older, you can make an additional catch-up contribution of $8,000. (Note: Employees aged 60-63 have a special higher catch-up limit of $11,250 if the plan permits).

- Traditional and Roth IRAs: The contribution limit is $7,500. The catch-up contribution for those age 50 and older remains $1,100.

- SIMPLE IRAs: The base limit is $17,000, with a $4,000 catch-up for those 50 and older.

Potential Ways to Get Into a Lower Tax Bracket

Taxpayers often ask about potential ways to get into a lower tax bracket. Because the tax brackets 2026 are marginal, dropping into a lower bracket only saves you the percentage difference on the income that crosses the threshold. Still, aggressive tax planning pays off.

Here are the primary levers you can pull:

- Max out workplace retirement plans: Every dollar you put into a traditional 401(k) or 403(b) reduces your taxable income for the year.

- Fund a Health Savings Account (HSA): If you have a High Deductible Health Plan, you can contribute to an HSA. For 2026, the limit is $4,400 for self-only coverage and $8,750 for family coverage. These contributions are tax-deductible.

- Harvest capital losses: If you sell stocks at a loss, you can use those losses to offset capital gains. If your losses exceed your gains, you can use up to $3,000 of the excess loss to offset your ordinary income.

- Bunch itemized deductions: If your deductible expenses are close to the standard deduction for 2026, consider bunching two years’ worth of charitable contributions or medical expenses into a single year so you can clear the hurdle and itemize.

Other Notable 2026 Tax Provisions

Federal income tax brackets 2026 don’t tell the whole story. Several other taxes and exclusions dictate your final financial picture.

2026 Alternative Minimum Tax

The 2026 Alternative Minimum Tax (AMT) operates parallel to the regular tax system. It ensures high-income earners pay a minimum amount of tax regardless of deductions. For 2026, the AMT exemption amount is $90,100 for single filers and $140,200 for married couples filing jointly. The exemption begins to phase out at $680,200 for singles and $1,280,400 for joint filers.

Social Security and Medicare Tax (2026)

The Social Security and Medicare Tax for 2026 (FICA) remains a combined 7.65% for employees. The Social Security portion (6.2%) is capped. For 2026, you only pay Social Security tax on the first $184,500 of your earnings. The Medicare portion (1.45%) has no wage base limit. High earners also face an Additional Medicare Tax of 0.9% on wages over $200,000 (single) or $250,000 (joint).

Social Security Benefit Taxation (2026)

Depending on your provisional income, up to 85% of your Social Security benefits may be taxable. The Social Security Benefit Taxation for 2026 thresholds remain unchanged. Single filers with provisional income over $34,000 and joint filers over $44,000 will see up to 85% of their benefits taxed at their marginal ordinary income rates.

2026 Annual Exclusion for Gifts

The 2026 Annual Exclusion for Gifts is $19,000. You can give up to $19,000 to as many individual people as you want in 2026 without having to file a gift tax return or eat into your lifetime estate and gift tax exemption. Married couples can combine this to give $38,000 per recipient.

Frequently Asked Questions About 2026 Taxes

What are the tax brackets for 2026?

There are seven federal tax brackets for 2026: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. The specific income ranges for each bracket depend on whether you file as single, married filing jointly, head of household, or married filing separately.

Did the married filing jointly tax brackets 2026 change?

Yes, the IRS adjusted the income thresholds for the married filing jointly tax brackets 2026 upward to account for inflation. For example, the 22% bracket now starts at $100,801, up from the previous year, allowing couples to earn more before hitting higher rates.

What is the standard deduction for a single filer in 2026?

The standard deduction for a single filer in 2026 is $16,100. If you are 65 or older, or blind, you can claim an additional standard deduction of $2,050.

How do I know what tax bracket 2026 I am in?

You find your tax bracket 2026 by calculating your taxable income (gross income minus deductions) and looking at the IRS tax tables for your filing status. The highest percentage bracket your income reaches is your marginal tax bracket.

Are individual tax rates 2026 going up?

The actual percentage rates (10% to 37%) for the individual tax rates 2026 have not increased. However, the income thresholds have shifted upward due to inflation adjustments, which generally benefits taxpayers.

What is the 2026 tax brackets table used for?

The 2026 tax brackets table is used to calculate your exact federal income tax liability. You apply the corresponding percentage to the income that falls within each specific band of the table.

Do state taxes use the federal income tax brackets 2026?

No. State income taxes are entirely separate from federal income tax brackets 2026. Some states have a flat tax rate, some have their own progressive brackets, and some states have no income tax at all.

What happens if my income pushes me into a higher bracket?

If your income pushes you into a higher bracket, only the income that exceeds the bracket threshold is taxed at the higher rate. Your entire income is never retroactively taxed at the new, higher percentage.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.

Your method of explaining the whole thing in this piece of writing is genuinely fastidious, every one be capable of

without difficulty be aware of it, Thanks a lot.

Hmm it appears like your site ate my first comment (it was super

long) so I guess I’ll just sum it up what I wrote and say,

I’m thoroughly enjoying your blog. I as well

am an aspiring blog blogger but I’m still new to everything.

Do you have any tips for novice blog writers?

I’d genuinely appreciate it.

My brother recommended I may like this blog.

He used to be entirely right. This post actually made my day.

You cann’t consider simply how a lot time I had spent for this info!

Thank you!

It’s a shame you don’t have a donate button!

I’d certainly donate to this superb blog!

I suppose for now i’ll settle for book-marking and adding your RSS feed to my

Google account. I look forward to fresh updates and will talk about this site with my Facebook group.

Talk soon!

This is my first time visit at here and i am in fact happy

to read everthing at single place.

Hey there great blog! Does running a blog like this take a

great deal of work? I’ve no understanding of computer programming but I had

been hoping to start my own blog soon. Anyhow,

if you have any ideas or techniques for new blog owners please share.

I understand this is off subject nevertheless I just needed

to ask. Thank you!

Wow, marvelous weblog layout! How long have you ever been running a blog for?

you make blogging look easy. The total glance of your web site is fantastic,

let alone the content material!

Excellent blog you’ve got here.. It’s difficult to find high quality writing like yours nowadays.

I really appreciate people like you! Take care!!

Awesome site you have here but I was curious about if you knew of any community

forums that cover the same topics talked about in this article?

I’d really like to be a part of community where I can get suggestions from other knowledgeable people that

share the same interest. If you have any suggestions, please let me

know. Cheers!

Hi there, I think your website may be having browser compatibility

problems. Whenever I take a look at your website in Safari,

it looks fine however when opening in IE, it’s got some overlapping issues.

I merely wanted to give you a quick heads

up! Besides that, excellent blog!

Superb, what a webpage it is! This blog provides useful data to us, keep it up.