⚡ Executive Summary: UGMA vs. UTMA vs. 529 Plan

- For tax year 2026, 529 plans offer 100% tax-free growth for education, while UGMA and UTMA accounts are subject to the annual Kiddie Tax on unearned income over $2,700.

- Custodial accounts (UGMA/UTMA) are considered student assets on the FAFSA and reduce financial aid eligibility by 20%, whereas parent-owned 529 plans reduce aid by a maximum of only 5.64%.

- Under SECURE 2.0 rules, up to $35,000 of unused 529 plan funds can now be rolled over into the beneficiary’s Roth IRA tax-free, eliminating the old “use-it-or-lose-it” education trap.

- UGMA and UTMA contributions are irrevocable gifts; the child gains total, unrestricted legal control of the money at the state’s age of majority (typically 18 to 21).

Table of Contents

- The Core Differences: UGMA vs. UTMA vs. 529 Plan

- Understanding Custodial Accounts: UGMA and UTMA Explained

- The 529 Plan: Tax-Free Growth College Savings

- The Tax Showdown: Kiddie Tax Rules 2026 vs. Tax-Free Growth

- FAFSA Financial Aid Asset Rules: The 20% Penalty

- The SECURE 2.0 529 to Roth IRA Rollover

- Step-by-Step: How to Choose the Best Way to Save for Kids College 2026

- Can You Convert a Custodial Account to a 529 Plan?

- Frequently Asked Questions About UGMA vs. UTMA vs. 529 Plan

Parents and grandparents looking to transfer wealth to the next generation face a strict set of tax rules. Picking the wrong account structure can trigger massive tax liabilities, destroy a student’s financial aid package, or hand a teenager unrestricted access to a massive portfolio before they are financially mature.

When evaluating the best way to save for kids college 2026, you will inevitably run into three primary options: the UGMA, the UTMA, and the 529 Plan. Each vehicle serves a distinct legal and financial purpose. The right choice depends entirely on whether you prioritize tax efficiency, spending flexibility, or control over the assets.

This comprehensive guide breaks down the exact mechanics of the UGMA vs. UTMA vs. 529 Plan debate. We will cover the updated 2026 tax thresholds, the latest FAFSA loopholes, and how new federal legislation has completely changed the math on college savings.

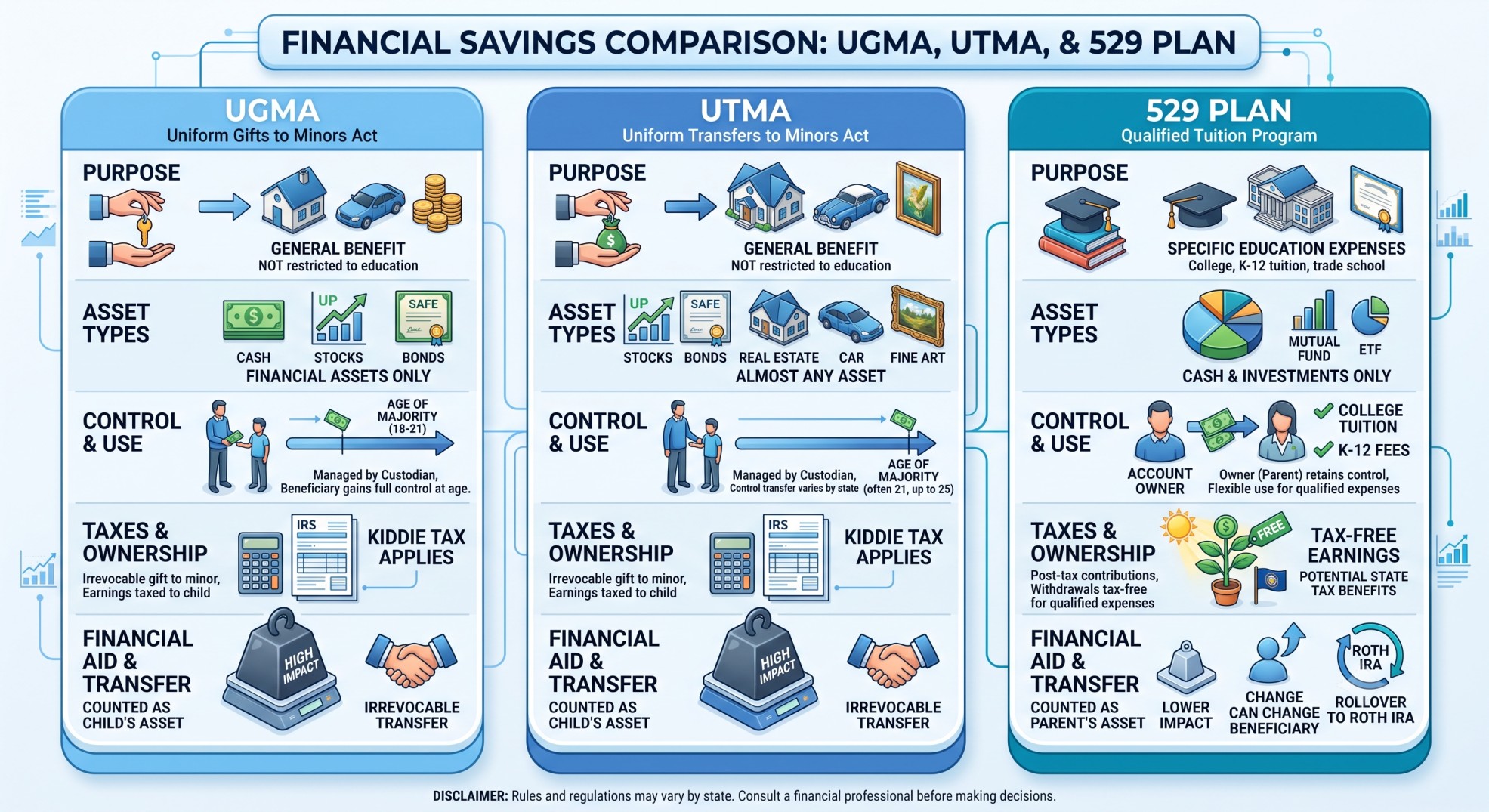

The Core Differences: UGMA vs. UTMA vs. 529 Plan

The fundamental difference between a custodial account vs 529 plan comes down to a trade-off between tax benefits and spending freedom. 529 plans offer unmatched tax shelters strictly for education. Custodial accounts offer ultimate asset flexibility but carry severe tax and financial aid penalties.

| Feature | UGMA (Uniform Gifts to Minors Act) | UTMA (Uniform Transfers to Minors Act) | 529 Plan (Qualified Tuition Plan) |

|---|---|---|---|

| Legal Owner | The Minor | The Minor | The Donor (Parent/Grandparent) |

| Allowed Assets | Financial only (Cash, Stocks, Mutual Funds) | Any property (Real Estate, Fine Art, Cars) | Cash invested in plan portfolios |

| Tax Treatment | Earnings subject to annual Kiddie Tax | Earnings subject to annual Kiddie Tax | 100% tax-free for qualified expenses |

| FAFSA Impact | High (Assessed at 20%) | High (Assessed at 20%) | Low (Assessed at max 5.64%) |

| Control Transfer | Age 18 (Typically) | Age 21 to 25 (State dependent) | Never (Donor retains lifelong control) |

If you are weighing the Uniform Transfers to Minors Act vs 529, you must first decide if you are comfortable surrendering total legal ownership of your money today. Understanding asset control is the foundation of any generational wealth strategy.

Understanding Custodial Accounts: UGMA and UTMA Explained

UGMA and UTMA accounts are custodial brokerage accounts managed by an adult on behalf of a minor child. They allow you to invest money for a minor without the heavy legal fees required to set up a formal trust.

The defining characteristic of both accounts is the rule of irrevocable gifts for minors. The moment you deposit cash or transfer stock into a UGMA or UTMA, that asset legally belongs to the child. You cannot take the money back if you face a personal financial emergency. You cannot transfer the account to a different sibling if the original beneficiary decides not to go to college.

While people often lump them together, the UGMA and UTMA differ in two specific ways.

Asset Class Restrictions

UGMA accounts are strictly limited to standard financial instruments. You can hold cash, stocks, bonds, mutual funds, and index funds. UTMA accounts are far more expansive. They can hold virtually any type of property, including physical real estate, fine art, patents, precious metals, and even family vehicles.

The Age of Majority Custodial Transfer

Because minors cannot legally execute contracts, the adult custodian manages the assets until the child reaches adulthood. The age of majority custodial transfer depends on your state’s specific laws and the type of account.

UGMA accounts typically transfer full, unrestricted control to the child at age 18. UTMA accounts usually allow the custodian to extend control longer, often until the beneficiary reaches age 21, and in some states, age 25. Once that birthday hits, the custodianship terminates. The child can liquidate the entire portfolio and buy a sports car, and the parent has zero legal authority to stop them.

The 529 Plan: Tax-Free Growth College Savings

A 529 plan is a state-sponsored investment account designed specifically to incentivize tax-free growth college savings. Unlike a custodial account, the parent or grandparent who opens the 529 plan retains 100% legal ownership and control of the money forever. The child is merely the listed beneficiary.

This control is absolute. If your child gets a full-ride scholarship or decides to skip college entirely, you can simply change the beneficiary to a sibling, a cousin, or even yourself without triggering any tax penalties. You dictate exactly when and how the money is distributed.

The trade-off for this control and tax efficiency is spending restriction. To keep the earnings tax-free, the money must be spent on qualified education expenses. This includes college tuition, mandatory fees, room and board, books, computers, and up to $10,000 per year for K-12 private school tuition.

If you withdraw 529 funds for non-educational purposes, the earnings portion of the withdrawal is subject to ordinary income tax plus a 10% IRS penalty. Managing non-qualified distributions requires careful tax planning.

The Tax Showdown: Kiddie Tax Rules 2026 vs. Tax-Free Growth

How your investments are taxed year-over-year is where the UGMA vs. UTMA vs. 529 Plan comparison becomes stark. Custodial accounts do not offer tax-deferred growth. They are fully taxable brokerage accounts subject to strict IRS regulations.

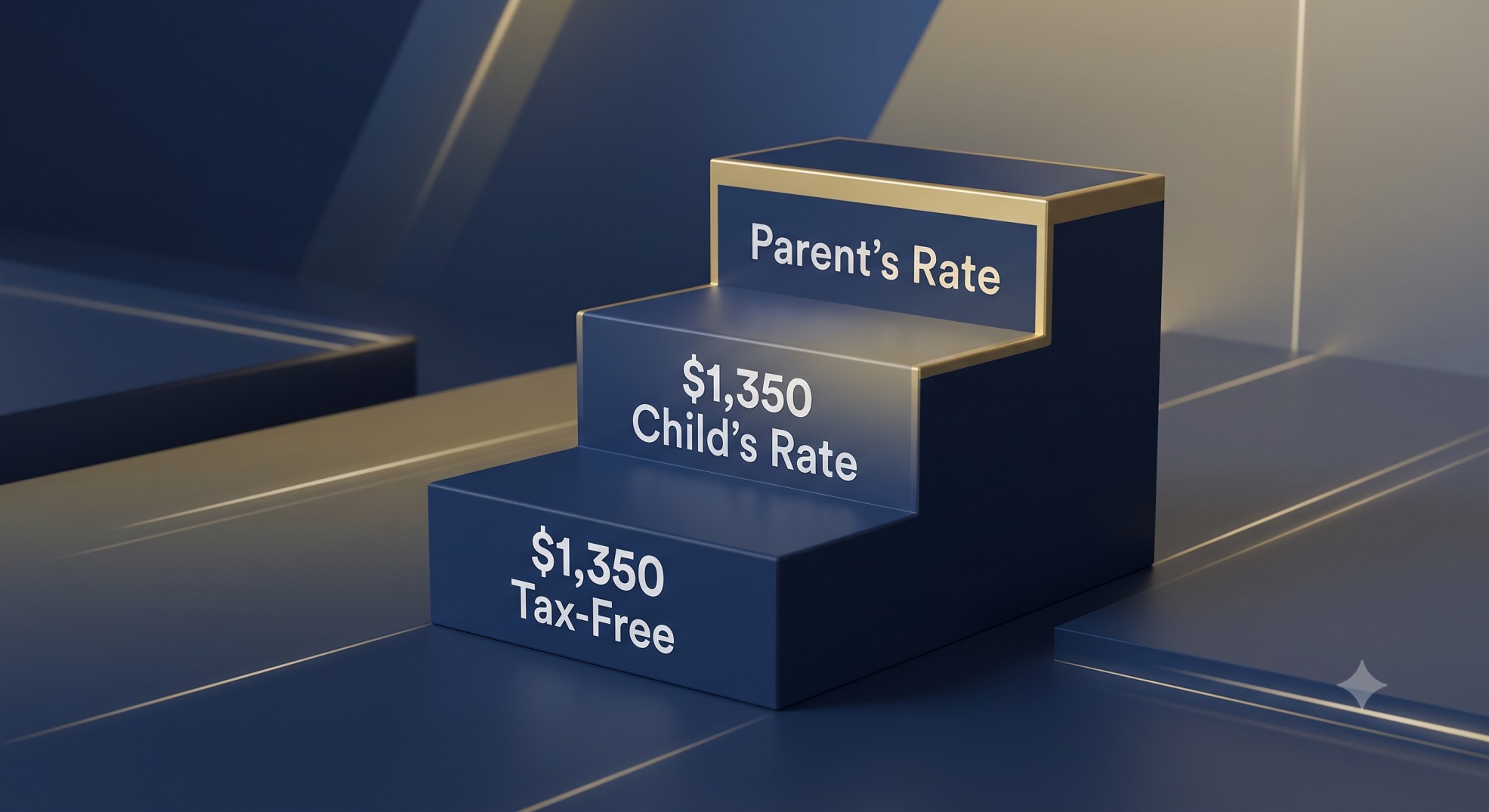

To prevent wealthy parents from shifting assets to their children to exploit lower tax brackets, the IRS enforces the Kiddie Tax. Under the Kiddie Tax rules 2026, any unearned income (dividends, interest, and realized capital gains) generated inside a UGMA or UTMA is taxed aggressively once it crosses a specific threshold.

For the 2026 tax year, the unearned income tax threshold is structured in three tiers:

- The First $1,350: Completely tax-free (covered by the child’s standard deduction).

- The Next $1,350: Taxed at the child’s individual marginal tax rate (usually 10%).

- Anything Over $2,700: Taxed at the parents’ highest marginal income tax rate.

Hypothetical Scenario: The Kiddie Tax Trap

Let’s look at the math. Suppose David funds a UTMA account for his daughter, Sarah. In 2026, the account portfolio is rebalanced, generating $6,000 in realized capital gains and dividends. David is in the 24% federal tax bracket.

Here is how Sarah’s UTMA is taxed under the Kiddie Tax rules 2026:

- The first $1,350 is tax-free.

- The next $1,350 is taxed at Sarah’s 10% rate ($135 tax).

- The remaining $3,300 is taxed at David’s 24% rate ($792 tax).

David and Sarah owe the IRS $927 for the year just to keep the account growing. If those exact same assets were held inside a 529 plan, the annual tax bill would be exactly $0. The 529 plan allows the portfolio to compound year after year without the friction of annual tax drag.

FAFSA Financial Aid Asset Rules: The 20% Penalty

If you expect your family to qualify for need-based student loans, federal grants, or work-study programs, the account structure you choose is critical. The Department of Education uses the Free Application for Federal Student Aid (FAFSA) to calculate your Student Aid Index (SAI).

The FAFSA financial aid asset rules evaluate student-owned assets far more harshly than parent-owned assets. Because UGMA and UTMA accounts are legally owned by the child, they trigger a massive financial aid penalty.

Custodial accounts are assessed at a flat 20% rate. Parent-owned 529 plans are assessed at a maximum rate of only 5.64%.

Hypothetical Scenario: The FAFSA Penalty

Assume a family has saved $60,000 for their child’s college education. Let’s compare the financial aid impact of a custodial account vs 529 plan.

Scenario A (The UTMA): The $60,000 sits in a UTMA. The FAFSA takes 20% of that balance and adds it to the family’s expected contribution. The student’s financial aid package is reduced by a staggering $12,000 per year.

Scenario B (The 529 Plan): The $60,000 sits in a parent-owned 529 plan. The FAFSA assesses it at 5.64%. The student’s financial aid package is reduced by a maximum of only $3,384 per year.

The Grandparent 529 Loophole

Recent updates to the simplified FAFSA introduced a massive advantage for extended families. Under the new rules for the 2024-2025 academic year and beyond, grandparent-owned 529 plans are completely ignored by the federal aid formula. Distributions from a grandparent’s 529 no longer count as untaxed student income. This means a grandparent can hold $100,000 in a 529 plan for a grandchild, and it will reduce the student’s federal aid eligibility by exactly $0. Maximizing grandparent college strategies is now the most efficient way to protect financial aid.

The SECURE 2.0 529 to Roth IRA Rollover

Historically, the biggest argument in favor of the Uniform Transfers to Minors Act vs 529 was flexibility. Parents worried that if their child didn’t go to college, the 529 funds would be trapped, facing a 10% penalty upon withdrawal. Custodial accounts, while tax-heavy, could be used for anything—a wedding, a house down payment, or starting a business.

The SECURE 2.0 Act completely neutralized this argument. Starting in 2024, the federal government introduced the SECURE 2.0 529 to Roth IRA rollover provision.

If a beneficiary finishes college with leftover 529 funds, or decides not to attend college at all, the account owner can roll those unused funds directly into a Roth IRA in the beneficiary’s name, completely tax-free and penalty-free.

The Strict Rollover Rules

You cannot simply dump the entire 529 balance into a Roth IRA overnight. The IRS enforces strict parameters:

- The 15-Year Rule: The 529 account must have been open for at least 15 consecutive years before a rollover can occur.

- Lifetime Cap: There is a strict $35,000 lifetime limit per beneficiary for these rollovers.

- Annual Limits Apply: The rollover is subject to the standard annual Roth IRA contribution limits. For 2026, that limit is $7,500. You must execute the rollover over several years to hit the $35,000 cap.

- Earned Income Requirement: The beneficiary must have earned income in the year of the rollover equal to or greater than the rollover amount.

- The 5-Year Rule: Contributions made to the 529 plan within the last 5 years (and the earnings on those contributions) are ineligible for the rollover.

Hypothetical Scenario: The Roth Head Start

Marcus opened a 529 plan when his son, Leo, was born. Leo graduates from trade school at age 22, leaving $20,000 unused in the 529 plan. Because the account has been open for 22 years, it qualifies for the SECURE 2.0 rollover. Leo gets a job earning $50,000 a year. Marcus rolls over $7,500 in 2026, $7,500 in 2027, and the final $5,000 in 2028 into Leo’s Roth IRA. Leo now has a massive, tax-free head start on his retirement, and Marcus avoided all non-qualified withdrawal penalties.

Step-by-Step: How to Choose the Best Way to Save for Kids College 2026

Determining the best way to save for kids college 2026 requires aligning your financial goals with the legal realities of these accounts. Follow this framework to make the right choice.

Step 1: Define the Primary Goal

Are you saving exclusively for education, or are you trying to build general generational wealth? If the goal is paying for tuition, the 529 plan wins every time due to tax-free growth and FAFSA protections. If you want to gift a child a rental property or seed money for a business, you must use a UTMA.

Step 2: Assess Your Tax Sensitivity

Review your current marginal tax bracket. If you are a high-income earner, the Kiddie Tax rules 2026 will aggressively tax any significant gains in a UGMA or UTMA at your top rate. A 529 plan shields those gains entirely.

Step 3: Evaluate the Child’s Maturity

Be brutally honest about the age of majority custodial transfer. Are you comfortable with an 18-year-old gaining unrestricted legal access to $100,000? If the thought of your teenager liquidating the portfolio to fund a vacation terrifies you, avoid custodial accounts. A 529 plan ensures you retain control of the capital forever.

Step 4: Maximize State Tax Deductions

If you opt for a 529 plan, check your state’s specific rules. Over 30 states offer state income tax deductions or credits for contributing to their sponsored 529 plans. Researching state-specific tax credits can yield an immediate return on your investment.

Can You Convert a Custodial Account to a 529 Plan?

Many parents open a UGMA when a child is born, only to realize years later that the FAFSA penalties and Kiddie Tax drag are destroying their wealth. You can convert a custodial account into a 529 plan, but the process is highly regulated.

You cannot simply transfer stock from a UTMA into a 529. You must liquidate the assets inside the custodial account, which will trigger capital gains taxes subject to the Kiddie Tax rules 2026. Once liquidated, you take the cash and open a specific account called a “Custodial 529 Plan.”

Because the original funds were irrevocable gifts for minors, the Custodial 529 retains that legal status. Unlike a standard 529 plan, you cannot change the beneficiary of a Custodial 529 to a sibling. The money still legally belongs to the original child, and they will gain control of the account at the age of majority. However, by moving the funds into the 529 structure, you successfully shield all future growth from taxes and reduce the FAFSA asset penalty from 20% down to 5.64%.

Frequently Asked Questions About UGMA vs. UTMA vs. 529 Plan

Is a 529 plan better than a UTMA custodial account?

For education savings, yes. A 529 plan is vastly superior because it offers 100% tax-free growth, protects financial aid eligibility, and allows the parent to retain permanent control of the money. A UTMA is only better if you intend to gift non-educational assets, like real estate, and are willing to surrender total control to the child at age 21.

What is the 2026 Kiddie Tax limit for custodial accounts?

For the 2026 tax year, the Kiddie Tax threshold for unearned income is $2,700. The first $1,350 is tax-free, the next $1,350 is taxed at the child’s rate, and any unearned income exceeding $2,700 is taxed at the parents’ highest marginal tax rate.

How does a UGMA account affect FAFSA financial aid eligibility?

A UGMA account severely damages financial aid eligibility. Because it is legally owned by the student, the FAFSA assesses the account balance at a flat 20%. A $50,000 UGMA will reduce a student’s financial aid package by $10,000 per year.

Can you roll over an UTMA into a 529 plan?

Yes, but it requires liquidation. You must sell the assets in the UTMA (which may trigger capital gains taxes), take the cash, and fund a “Custodial 529 Plan.” The money remains an irrevocable gift to that specific child, meaning you cannot change the beneficiary later.

What happens to a UGMA account when the child turns 18?

When the child reaches the state’s statutory age of majority (typically 18 for a UGMA), the custodianship legally terminates. The child gains total, unrestricted control of the assets and can spend the money on anything they want, regardless of the parents’ wishes.

Can I change the beneficiary on a UTMA account?

No. Contributions to a UTMA are irrevocable gifts for minors. Once the money is deposited, it legally belongs to that specific child forever. You cannot transfer the funds to a sibling or take the money back for yourself.

What are the contribution limits for a 529 plan in 2026?

529 plans do not have annual contribution limits, but they do have lifetime aggregate limits set by each state (often exceeding $500,000). However, to avoid filing a federal gift tax return, your contributions should stay under the 2026 annual gift tax exclusion limit of $19,000 per donor, per beneficiary.

Do grandparent-owned 529 plans affect financial aid?

No. Under the new simplified FAFSA rules effective for the 2024-2025 academic year and beyond, grandparent-owned 529 plans are completely ignored. The balances are not reported as assets, and the distributions no longer count as untaxed student income.

What qualifies as an education expense for a 529 plan?

Qualified education expenses include college tuition, mandatory fees, room and board (if enrolled at least half-time), books, supplies, and computers. You can also use up to $10,000 per year for K-12 private school tuition, and up to a $10,000 lifetime limit to pay down student loans.

Can I hold real estate in a UGMA account?

No. UGMA accounts are restricted to financial assets like cash, stocks, bonds, and mutual funds. If you want to transfer physical property, real estate, or fine art to a minor, you must use a UTMA account.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.