A single extra dollar of retirement income sounds harmless enough. For thousands of Medicare beneficiaries, that one dollar can trigger thousands of dollars in surprise premium charges the very next year. Financial planners have a name for this: the IRMAA tax trap.

Retirement income planning for 2026 needs to account for this trap early. Medicare’s Income-Related Monthly Adjustment Amount, or IRMAA, quietly raises your Part B and Part D premiums based on income you reported two years earlier. Decisions you make today about IRA withdrawals, Roth conversions, or investment sales can echo forward and hit your Medicare premiums in ways you never expected.

⚡ Executive Summary: The IRMAA Tax Trap Explained

- Your Modified Adjusted Gross Income (MAGI) from two years prior determines your Medicare Part B and Part D premiums.

- A small increase in MAGI can push you into a higher IRMAA bracket, triggering significantly higher Medicare premiums for the entire year.

- The standard 2026 Part B premium is $202.90 a month, while average Part D coverage runs about $34.50 a month.

- Higher earners pay an additional IRMAA surcharge that can add hundreds of dollars to their monthly costs.

- Proactive planning, including Roth conversions and Qualified Charitable Distributions, helps you manage MAGI before it becomes a problem.

- A qualifying life-changing event lets you appeal an IRMAA determination and potentially lower your premium.

Table of Contents

- How Medicare’s IRMAA Really Works

- 2026 IRMAA Brackets and the Income Cliff Effect

- A Real-World Example: How One Extra Dollar Cost Eleanor Vance Thousands

- Practical Strategies to Stay Out of a Higher IRMAA Bracket

- Already Hit With IRMAA? Here’s How to Appeal It

- Key Takeaways Before You File Your Next Tax Return

How Medicare’s IRMAA Really Works

Medicare covers essential health needs for adults 65 and older, but certain parts carry income-based surcharges built right into the premium. That surcharge is the Income-Related Monthly Adjustment Amount, or IRMAA, and it applies to both Part B medical insurance and Part D prescription drug coverage. Beneficiaries with higher reported income simply pay more for the same coverage everyone else receives.

What Is IRMAA, Exactly?

IRMAA is an extra charge added on top of your standard Medicare Part B and Part D premiums. Congress created this surcharge so that beneficiaries with higher incomes contribute more toward their own healthcare costs. Depending on your income, your monthly Medicare bill can end up far higher than the standard rate published each year.

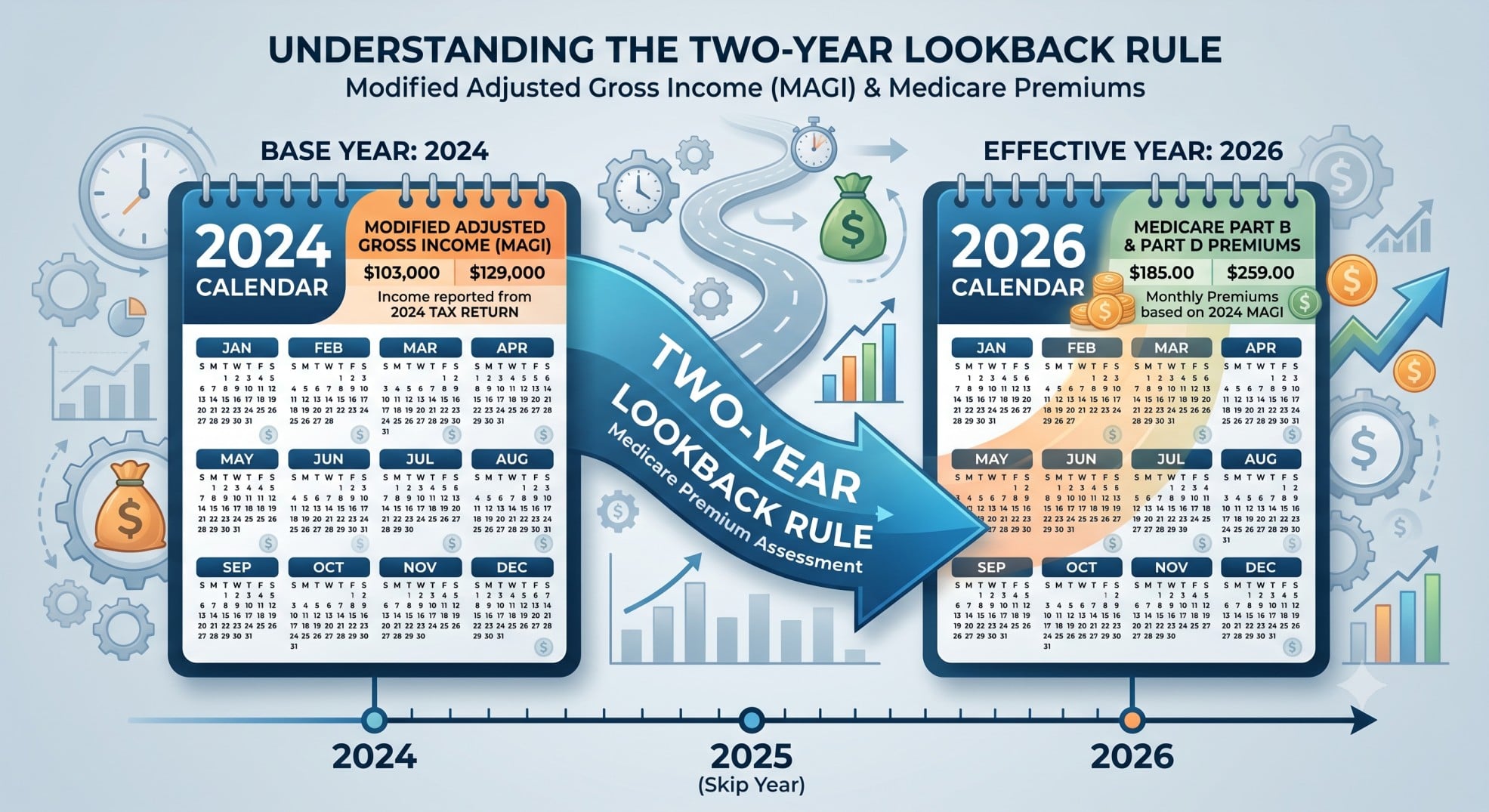

Why Does Medicare Look at Income From Two Years Ago?

The Social Security Administration bases your current-year IRMAA on the Modified Adjusted Gross Income you reported two years earlier. Your 2026 Medicare premiums, in other words, depend entirely on the MAGI shown on your 2024 federal tax return. That gap between the income year and the premium year is exactly why planning ahead matters, since a decision you make this year won’t show up on your Medicare bill until 2028.

What Is Modified Adjusted Gross Income (MAGI) for IRMAA?

MAGI for IRMAA purposes equals your regular Adjusted Gross Income plus certain tax-exempt income added back in, such as tax-exempt interest from municipal bonds. This calculation differs from the MAGI used for other tax provisions, and the difference catches many retirees off guard. Income that looks tax-free on paper can still shove you into a higher Modified Adjusted Gross Income bracket for Medicare purposes.

2026 IRMAA Brackets and the Income Cliff Effect

The dollar amounts matter more than most retirees realize. Crossing an income threshold by even a small margin can raise your Medicare premiums for an entire year, a phenomenon commonly called the “cliff effect.”

What Are the Standard Medicare Premiums for 2026?

Standard Medicare Part B premiums for 2026 sit at $202.90 a month, with standalone Part D plans averaging roughly $34.50 a month. Beneficiaries whose MAGI falls below the lowest IRMAA threshold pay exactly these amounts, with no surcharge attached.

2026 IRMAA Brackets Based on 2024 MAGI

Surcharges kick in once your 2024 MAGI exceeds $109,000 for single filers or $218,000 for married couples filing jointly. These thresholds rise with inflation each year, though the top bracket stays frozen until 2028. The table below breaks down every bracket and its corresponding premium.

| Filing Status | 2024 MAGI | Monthly Part B Premium (includes surcharge) | Monthly Part D IRMAA Surcharge (added to plan premium) |

|---|---|---|---|

| Single | $109,000 or less | $202.90 (Standard) | $0 |

| $109,001 to $137,000 | $284.10 | $14.50 | |

| $137,001 to $171,000 | $405.80 | $37.50 | |

| $171,001 to $205,000 | $527.50 | $60.40 | |

| $205,001 to $499,999 | $649.20 | $83.30 | |

| $500,000 or more | $689.90 | $91.00 | |

| Married Filing Jointly | $218,000 or less | $202.90 (Standard) | $0 |

| $218,001 to $274,000 | $284.10 | $14.50 | |

| $274,001 to $342,000 | $405.80 | $37.50 | |

| $342,001 to $410,000 | $527.50 | $60.40 | |

| $410,001 to $749,999 | $649.20 | $83.30 | |

| $750,000 or more | $689.90 | $91.00 | |

| Married Filing Separately | $109,000 or less | $202.90 (Standard) | $0 |

| Above $109,000 and less than $391,000 | $649.20 | $83.30 | |

| $391,000 or more | $689.90 | $91.00 |

What Is the IRMAA “Cliff Effect”?

The cliff effect means crossing an income threshold by even one dollar makes you pay the full surcharge for that entire bracket, not just on the amount over the line. A single filer with 2024 MAGI of $205,000 sits in the fourth bracket, paying a $527.50 Part B premium. Push that MAGI to $205,001, and the same filer jumps into the fifth bracket, paying $649.20 instead. One extra dollar of income costs that person an additional $121.70 every month, or $1,460.40 over the year, for Part B alone.

A Real-World Example: How One Extra Dollar Cost Eleanor Vance Thousands

Numbers on a bracket chart only tell half the story. Here’s how the cliff effect plays out for a real retiree navigating her 2026 Medicare costs.

Case Study: Eleanor Vance and the IRMAA Tax Trap (2026)

Eleanor Vance, 70, lives in California and draws a comfortable retirement income from several sources: Social Security benefits of $30,000 (with $25,500 taxable at her income level), pension income of $60,000, IRA distributions of $49,000, and investment income of $70,000 from dividends and capital gains.

Key 2026 assumptions used in this example: a federal standard deduction of $17,000 for a single filer 65 or older, a California standard deduction of $6,000 plus a $150 senior exemption credit, a standard Medicare Part B premium of $202.90 a month, an average Part D premium of $34.50 a month, and a Net Investment Income Tax threshold of $200,000 for single filers.

Scenario 1 — Eleanor’s base income: Her total income produces a MAGI of $204,500, just under the $205,000 threshold for single filers.

- Federal income tax: $39,000.00

- California state income tax: $13,000.00

- Net Investment Income Tax: $1,330.00 (3.8% of the $35,000 by which her $70,000 investment income exceeds the $200,000 MAGI threshold)

- Medicare Part B premium including IRMAA: $6,330.00 (($202.90 standard + $324.60 surcharge) × 12 months)

- Medicare Part D premium including IRMAA: $1,138.80 (($34.50 standard + $60.40 surcharge) × 12 months)

- Total tax burden: $60,800.80

Scenario 2 — one extra $1,000 IRA distribution: Eleanor pulls an additional $1,000 from her IRA, pushing her MAGI to $205,500 and over the threshold.

- Federal income tax: $39,320.00 (the extra $1,000 taxed at her 32% marginal rate)

- California state income tax: $13,080.00 (the extra $1,000 taxed at her 8% marginal rate)

- Net Investment Income Tax: $1,330.00 (unchanged, since her investment income remains the limiting factor)

- Medicare Part B premium including IRMAA: $7,790.40 (($202.90 standard + $446.30 surcharge) × 12 months)

- Medicare Part D premium including IRMAA: $1,413.60 (($34.50 standard + $83.30 surcharge) × 12 months)

- Total tax burden: $62,934.00

The trap revealed: That single $1,000 increase in MAGI triggered a $320.00 jump in federal tax, an $80.00 jump in state tax, a $1,460.40 jump in her Part B premium, and a $274.80 jump in her Part D premium — a total increase of $2,135.20 for one extra $1,000 of income.

Eleanor’s effective marginal rate on that last $1,000 works out to 213.52% ($2,135.20 divided by $1,000). Crossing into a higher IRMAA bracket cost her an extra $121.70 a month for Part B and $22.90 a month for Part D — $1,735.20 a year — stacked directly on top of her regular income taxes.

Practical Strategies to Stay Out of a Higher IRMAA Bracket

Eleanor’s story is a warning, not a life sentence. Several planning tools can help you keep your MAGI below the next threshold.

Make MAGI Management Your Starting Point

Controlling income during the look-back year is the foundation of every other strategy on this list. That means mapping out retirement account withdrawals, investment gains, and any other taxable income well before the tax year closes.

Use Roth Conversions to Shift Future Income

Roth conversions move money from a traditional IRA or 401(k) into a Roth account. Converting raises your MAGI in the year you do it, but qualified Roth withdrawals come out tax-free in retirement and never count toward MAGI for IRMAA purposes later. Many retirees use “bracket filling,” converting just enough to use up a lower tax bracket without tipping into a higher IRMAA tier, ideally before Medicare eligibility begins or Required Minimum Distributions kick in.

Send IRA Funds Directly to Charity With a QCD

Qualified Charitable Distributions let anyone 70½ or older send IRA funds straight to a qualified charity. That distribution never touches taxable income, and it satisfies your Required Minimum Distribution without adding a dime to your MAGI. Retirees who give charitably each year often find this the simplest fix on the list.

Balance Withdrawals Across Account Types

Spreading withdrawals across taxable, tax-deferred, and tax-free accounts keeps any single year’s MAGI from spiking unexpectedly. Large, one-time withdrawals or investment sales are usually what push retirees into a higher IRMAA bracket without warning. A diversified withdrawal plan gives you room to maneuver every year.

Other Ways to Keep Income Off Your MAGI Radar

- Harvest capital losses: Selling losing investments strategically offsets gains and lowers your overall taxable income.

- Max out pre-tax contributions: Workers still employed can contribute the maximum to 401(k)s and similar accounts to shrink current MAGI.

- Delay Social Security: Waiting to claim benefits can lower taxable income in early retirement, leaving more room for other strategies.

- Tap HSAs for medical costs: Withdrawals for qualified medical expenses come out tax-free and never touch MAGI.

- Consider life insurance cash value: Some policies allow structured withdrawals that don’t count toward MAGI for IRMAA purposes.

Already Hit With IRMAA? Here’s How to Appeal It

Yes, you can appeal an IRMAA determination if you’ve experienced a qualifying life-changing event. The Social Security Administration will reconsider your surcharge once you document the event and show how it affected your income.

Which Life-Changing Events Qualify?

The event must happen after the tax year used to calculate your current IRMAA. For your 2026 IRMAA, that means the event needs to have occurred in 2025 or 2026. Qualifying events include marriage, divorce or annulment, death of a spouse, work stoppage or reduction such as retirement, loss of income-producing property, loss or reduction of certain pension income, and an employer settlement payment.

How Do You File the Appeal?

Filing starts with contacting the Social Security Administration directly. Form SSA-44, “Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event,” is the document you’ll need to complete, along with supporting paperwork proving your life-changing event. The SSA reviews each case individually and may lower your Medicare premiums once your new income is verified. Full details are available directly from the Social Security Administration’s IRMAA page.

Key Takeaways Before You File Your Next Tax Return

Avoiding the IRMAA tax trap comes down to a handful of habits worth repeating every year.

- Know your MAGI: Understand exactly how each income source feeds into your Modified Adjusted Gross Income.

- Plan distributions with intention: Manage retirement account withdrawals so they don’t accidentally push you over a threshold.

- Look at Roth conversions early: They can shrink your future IRMAA exposure if timed correctly.

- Use QCDs after 70½: They lower MAGI and cover your RMD requirement in one move.

- Bring in a professional: A tax advisor who specializes in retirement planning can tailor these strategies to your situation, and the IRS offers additional guidance through its retirement topics resource on IRA distributions.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.