For years, the $10,000 federal cap on State and Local Tax (SALT) deductions has been a thorn in the side of high-net-worth individuals. This particularly affects those residing in states with substantial income and property taxes. Just when relief seemed possible with an increased cap for 2025, a new, more subtle threat has emerged: the “$500k Torpedo Trap.” This isn’t just about a higher cap; it’s about a critical income range where your effective marginal tax rate could skyrocket. This silently reduces your hard-earned wealth. Are you prepared for this new tax challenge and to ensure your strategies are effective to save SALT deduction in 2025 and 2026? This article will explain how to manage your MAGI phase-out and use the PTE election for effective tax planning.

Executive Summary

- The federal SALT deduction cap increases to $40,000 for most filers in 2025.

- However, this increased cap phases out for Modified Adjusted Gross Income (MAGI) above $500,000.

- The “SALT Torpedo Trap” refers to a sharp increase in effective marginal tax rates for MAGI between $500,000 and $600,000.

- Pass-Through Entity (PTE) elections remain a powerful strategy to bypass the individual SALT cap.

- Strategic MAGI management, including income timing and retirement contributions, can help avoid the phase-out.

- Proactive tax planning and professional advice are essential to optimize your tax position for 2025 and beyond.

Understanding the Changes to the SALT Deduction for 2025

The TCJA’s Legacy: The $10,000 Cap and Its Impact

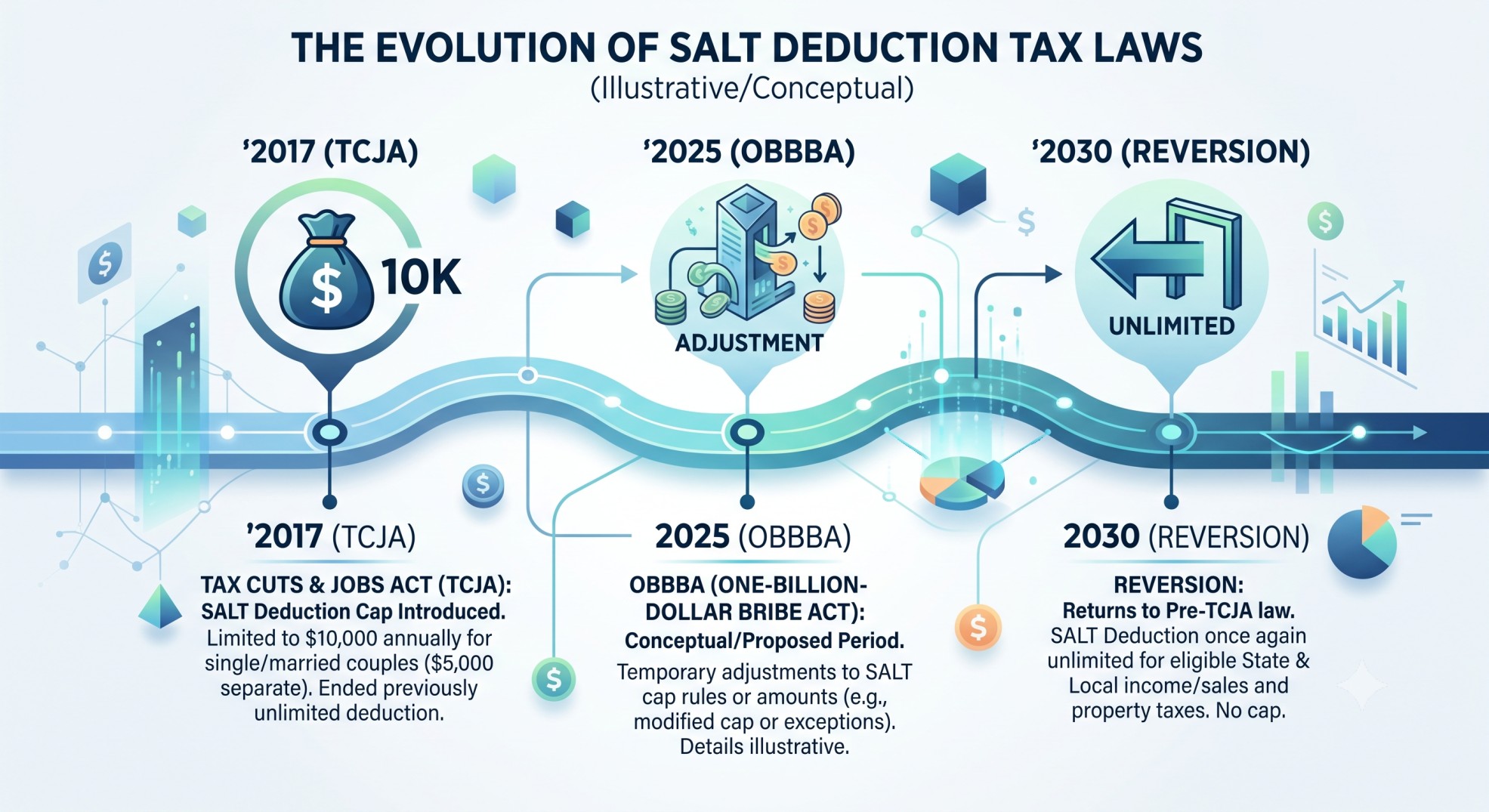

The Tax Cuts and Jobs Act (TCJA) of 2017 introduced a $10,000 federal cap on individual State and Local Tax (SALT) deductions. This cap applied from 2018 through 2025. This limitation disproportionately affected high-net-worth individuals, especially those in states with high income and property taxes. Many taxpayers found their federal tax liability increasing significantly because of this restriction.

The One Big Beautiful Bill Act (OBBBA) of 2025: An Important Change?

An important change arrived with the One Big Beautiful Bill Act (OBBBA), enacted on July 4, 2025. This legislation raised the federal SALT deduction cap. For 2025, the cap increases to $40,000 for most filers, including single, married filing jointly, and head of household. Married individuals filing separately will see a cap of $20,000. This increased cap is scheduled to last from 2025 through 2029. It will also increase by 1% annually during this period. However, the cap is set to revert to the original $10,000 ($5,000 for MFS) starting in 2030.

The Important New Element: Modified Adjusted Gross Income (MAGI) Phase-out

The increased SALT cap is not universal; it comes with a new MAGI phase-out mechanism. For 2025, the phase-out begins when your Adjusted Gross Income (AGI), specifically your Modified Adjusted Gross Income (MAGI), exceeds $500,000. For married individuals filing separately, this threshold is $250,000. Your deduction is reduced by 30% of the excess MAGI over this threshold. However, the cap cannot be reduced below $10,000 ($5,000 for MFS). This phase-out effectively eliminates the benefit of the increased cap once your MAGI reaches $600,000 ($300,000 for MFS). Understanding this MAGI phase-out is vital for effective tax planning.

The $500k Torpedo Trap: A Closer Look

What is the “SALT Torpedo Trap”?

The “SALT Torpedo Trap” describes a sharp increase in effective marginal tax rates for high-net-worth individuals. This occurs when their MAGI falls between $500,000 and $600,000. Within this specific income range, taxpayers face a double impact. They pay higher taxes on their additional income, and they simultaneously lose a portion of their SALT deduction. This combination can lead to an effective marginal tax rate as high as 45.5% on income earned within this $100,000 window. It’s a silent wealth reduction mechanism.

Identifying Your Risk: Are You Affected?

High-net-worth individuals must determine if their MAGI falls into this critical range. Common income sources contributing to MAGI include W-2 wages, business income from S-corporations or partnerships, investment income, and capital gains. Carefully projecting your income for 2025 is essential. This helps identify if you are at risk of hitting the MAGI phase-out. Proactive tax planning can help avoid this trap.

Advanced Strategies to Save Your SALT Deduction in 2025

Using Pass-Through Entity (PTE) Tax Workarounds

IRS Notice 2020-75 remains highly relevant for business owners. This notice clarifies that state and local income taxes paid by a partnership or an S-corporation at the entity level are deductible by the PTE. This effectively allows entity-level state tax payments to bypass the individual SALT cap. Many states have adopted elective PTE taxes. Understanding your state’s specific PTE election rules and requirements is important. Ensure proper entity payment and compliance to maximize this benefit and save SALT deduction.

Strategic MAGI Management to Avoid the Torpedo Trap

Managing your MAGI is a powerful way to avoid the “SALT Torpedo Trap.” Consider income timing strategies, such as deferring income like bonuses or capital gains into a later tax year. You might also accelerate deductions. Maximizing pre-tax contributions to retirement accounts, such as 401(k)s and traditional IRAs, can also reduce your MAGI. However, exercise caution with Roth conversions. These conversions generate taxable income, which increases your MAGI and could inadvertently trigger the MAGI phase-out.

Re-evaluating Itemized Deductions vs. Standard Deduction

With the increased SALT cap, more high-net-worth individuals may find it beneficial to itemize their deductions. Previously, the $10,000 cap often made the Standard Deduction more attractive. Now, compare your total Itemized Deductions, including the potentially higher SALT amount, against the standard deduction. This comparison will determine the most advantageous approach for your tax situation.

Proactive Planning and Modeling

The complexity of the new rules requires proactive tax planning. Simulating different income scenarios is essential. This helps you understand the precise impact on your federal tax liability. Identifying optimal strategies tailored to your individual circumstances can significantly improve your tax situation. This forward-looking approach is key to successfully managing the 2025 tax year and beyond to save SALT deduction.

Real-World Scenario: The $500k Torpedo Trap: Saving Your SALT Deduction in 2025

For High-Net-Worth Individuals (HNWI), the $10,000 cap on State and Local Tax (SALT) deductions has been a significant federal tax burden. While this cap is set to expire after 2025, proactive strategies are crucial for maximizing deductions in the current tax environment. One such advanced strategy, particularly effective in high-tax states like California, is the Pass-Through Entity (PTE) Elective Tax. This case study illustrates how a HNWI can manage the “torpedo trap” of the SALT cap in 2025 using this powerful workaround.

Scenario Overview: The California Entrepreneur

Meet Mr. and Mrs. Smith, a married couple filing jointly in California for the 2025 tax year. They have a combined W-2 income of $500,000 and own a successful S-Corporation generating $1,500,000 in qualified business income (QBI). Their investment portfolio yields $170,000 in long-term capital gains, qualified dividends, interest, and rental income. They also pay $25,000 in property taxes, $30,000 in mortgage interest, and contribute $50,000 to charity.

Their estimated total California state income tax liability (before any PTE election) is substantial, reflecting California’s high tax rates. We will analyze two scenarios: one where they pay state taxes personally, subject to the federal SALT cap, and another where their S-Corporation elects to pay the California PTE tax.

Scenario 1: The Baseline – No PTE Election

In this scenario, the Smiths pay their California state income taxes personally. Their total state and local taxes (including property tax) far exceed the federal $10,000 SALT deduction cap.

- Adjusted Gross Income (AGI): $2,200,000

- Total State & Local Taxes Paid Personally: $212,500 (Estimated CA Income Tax + Property Tax)

- Allowable SALT Deduction (Capped): $10,000

- Total Allowable Itemized Deductions: $90,000 (Capped SALT + Mortgage Interest + Charity)

- Qualified Business Income (QBI) Deduction: $250,000

- Final Taxable Income: $1,859,999.99

- Regular Federal Income Tax: $588,853.50

- Alternative Minimum Tax (AMT) Calculated: $590,586.00

- Net Investment Income Tax (NIIT): $7,600.00

- Total Federal Tax Liability: $598,186.00

In this baseline, the Smiths’ high state tax burden significantly limits their federal deduction, and they are subject to the Alternative Minimum Tax (AMT) due to the add-back of state and local taxes.

Scenario 2: Using the PTE Election

Now, the Smiths’ S-Corporation elects to pay the California Pass-Through Entity (PTE) tax. This allows the business to deduct a portion of the state income tax at the entity level, which flows through as a federal deduction before the $10,000 SALT cap applies to their personal taxes.

By making the PTE election, the Smiths’ business income for federal tax purposes is reduced by the state tax paid at the entity level. This effectively bypasses the SALT cap for a significant portion of their state tax liability.

- PTE Tax Paid by Business: $139,500 (1,500,000 QBI * 9.3% CA PTE rate)

- Adjusted Gross Income (AGI): $2,060,500 (Lower due to business income reduction)

- Personal CA State Income Tax Paid: $110,500 (Reduced due to PTE credit)

- Total State & Local Taxes Paid Personally: $135,500 (Reduced CA Income Tax + Property Tax)

- Allowable SALT Deduction (Capped): $10,000

- Total Allowable Itemized Deductions: $90,000

- Qualified Business Income (QBI) Deduction: $250,000

- Final Taxable Income: $1,720,500.00

- Regular Federal Income Tax: $537,238.50

- Alternative Minimum Tax (AMT) Calculated: $476,521.00

- Net Investment Income Tax (NIIT): $7,600.00

- Total Federal Tax Liability: $544,838.50

Takeaway

The PTE election significantly reduced the Smiths’ federal tax liability.

- Total Federal Tax Liability (Without PTE): $598,186.00

- Total Federal Tax Liability (With PTE): $544,838.50

- Federal Tax Savings: $53,347.50

This case study demonstrates that for HNWI in high-tax states, the PTE election is a powerful strategy to reduce the impact of the federal SALT deduction cap. By shifting state income tax payments from the individual to the pass-through entity, a substantial portion of state taxes becomes federally deductible, leading to significant federal tax savings. This strategy is particularly important in 2025, as it allows taxpayers to maximize their deductions before the potential expiration of the SALT cap or other legislative changes in 2026.

Looking Ahead: The SALT Deduction in 2026 and Beyond

Annual Cap and MAGI Threshold Increases (1% annually)

The increased SALT cap and the MAGI phase-out thresholds will both increase by 1% annually from 2026 through 2029. This means the thresholds will slightly adjust each year. Staying informed about these incremental changes is part of effective tax planning.

The 2030 Reversion: Preparing for the $10,000 Cap

It is crucial to remember the temporary nature of the increased cap. The SALT cap is scheduled to revert to $10,000 ($5,000 for MFS) starting in 2030. Therefore, long-term tax planning must account for this future change. This ensures strategies remain effective well into the next decade.

Potential for Further Legislative Changes

Tax law is always changing and subject to frequent changes. Future legislative actions could further modify the SALT deduction rules. So, staying informed about potential legislative developments is essential. Always consult with professionals to adapt your strategies as needed.

Conclusion

The evolving rules surrounding the SALT deduction present both challenges and opportunities for high-net-worth individuals. The “SALT Torpedo Trap” and the new MAGI phase-out require careful attention. However, advanced strategies like the PTE election and proactive MAGI management can help you save SALT deduction. These tools protect your wealth in 2025 and beyond. Given the complexity and individual-specific nature of tax planning, we advise you to consult with a qualified tax advisor, CPA, or tax attorney. They can provide personalized guidance tailored to your unique financial situation. This ensures compliance and maximizes your tax efficiency.

Citations and Resources:

- IRS Credits and Deductions

- Internal Revenue Code (IRC) Section 164 – Cornell Law School LII

- IRS Notice 2020-75

- Treasury Regulations Section 1.164-1 (Available via eCFR, e.g., eCFR.gov)

- For professional analysis and consensus, refer to publications from Bloomberg Tax, Tax Foundation, Wall Street Journal, and Forbes.

Glossary:

- Adjusted Gross Income (AGI): Your gross income minus specific deductions allowed by the IRS. It’s a key figure for many tax calculations.

- Itemized Deductions: Eligible expenses that individual taxpayers can claim on federal income tax returns. These reduce your taxable income.

- Modified Adjusted Gross Income (MAGI): AGI with certain deductions added back. It is used to determine eligibility for various tax benefits and phase-outs.

- Pass-Through Entity (PTE) Election: A state-level election allowing partnerships or S-corporations to pay state income taxes at the entity level. This bypasses the federal SALT cap for individual owners.

- SALT Deduction: The deduction for state and local taxes paid, including income, sales, and property taxes.

- Standard Deduction: A specific dollar amount that reduces the amount of income on which you’re taxed. Taxpayers can choose between the standard deduction or itemized deductions.

- Tax Planning: The analysis of a financial situation or plan to ensure all elements work together to allow you to pay the lowest taxes possible.

Frequently Asked Questions

What is the federal SALT deduction cap for 2025?

The federal SALT deduction cap increases to $40,000 for most filers in 2025 ($20,000 for married individuals filing separately). This increased cap is scheduled to last until 2029, increasing by 1% annually, before reverting to $10,000 ($5,000 for MFS) starting in 2030.

What is the “SALT Torpedo Trap”?

The “SALT Torpedo Trap” describes a sharp increase in effective marginal tax rates for high-net-worth individuals whose Modified Adjusted Gross Income (MAGI) falls between $500,000 and $600,000. In this income range, taxpayers face a double impact of higher taxes on additional income and a simultaneous loss of their SALT deduction, potentially leading to effective marginal tax rates as high as 45.5%.

How does the MAGI phase-out affect the increased SALT cap?

The increased SALT cap begins to phase out when your Modified Adjusted Gross Income (MAGI) exceeds $500,000 ($250,000 for married individuals filing separately). Your deduction is reduced by 30% of the excess MAGI over this threshold. The cap cannot be reduced below $10,000 ($5,000 for MFS), and the benefit of the increased cap is effectively eliminated once your MAGI reaches $600,000 ($300,000 for MFS).

How can Pass-Through Entity (PTE) elections help bypass the individual SALT cap?

IRS Notice 2020-75 clarifies that state and local income taxes paid by a partnership or S-corporation at the entity level are deductible by the PTE. This allows entity-level state tax payments to bypass the individual SALT cap, as the deduction occurs before income flows to the individual, thereby reducing their federal taxable income. Many states have adopted elective PTE taxes.

What strategies can help manage MAGI to avoid the Torpedo Trap?

Strategies to manage MAGI include timing income (e.g., deferring bonuses or capital gains into a later tax year), accelerating deductions, and maximizing pre-tax contributions to retirement accounts (such as 401(k)s and traditional IRAs). However, caution is advised with Roth conversions, as they generate taxable income and can inadvertently increase your MAGI.

What is the long-term outlook for the SALT deduction cap?

The increased SALT cap and MAGI phase-out thresholds will both increase by 1% annually from 2026 through 2029. However, it is crucial to remember that the cap is scheduled to revert to the original $10,000 ($5,000 for MFS) starting in 2030. Long-term tax planning must account for this future change, and staying informed about potential legislative developments is essential.