For high-net-worth individuals (HNWIs), the 2025 tax year presents challenges. This often involves “stealth taxes” that significantly impact investment returns and overall wealth. Beyond the headline tax rates, the 3.8% NIIT stands as a prime example. It silently expands its reach due to non-indexed thresholds. This isn’t merely about paying more; it’s about understanding the interaction of federal and state regulations. Furthermore, it involves phase-outs and the need for smart HNWI tax planning to protect your financial future. Are you prepared for these hidden traps?

Executive Summary

- The 3.8% NIIT (Net Investment Income Tax) remains an important concern for HNWIs in 2025.

- Its thresholds are not indexed for inflation, making it a growing “stealth tax” burden.

- Key thresholds for individuals are $250,000 (MFJ), $200,000 (Single/HoH), and $125,000 (MFS).

- Other “stealth tax” factors include the $10,000 SALT cap, QBI deduction phase-outs, and the Alternative Minimum Tax (AMT).

- Smart HNWI tax planning strategies, such as Roth conversions and municipal bonds, are important.

- Consulting a qualified tax professional is important for personalized advice.

The 3.8% NIIT: Understanding Its Reach in 2025

The 3.8% NIIT is an important consideration for high-net-worth individuals. It applies to certain investment income when Modified Adjusted Gross Income (MAGI) exceeds specific thresholds. This tax has a wide impact on investment portfolios.

Rules and Regulations: IRC Section 1411

The Net Investment Income Tax originates from Internal Revenue Code (IRC) Section 1411. It became effective on January 1, 2013, as part of the Affordable Care Act. The tax aims to fund healthcare initiatives. The IRS provides guidance through Topic No. 559, Net Investment Income Tax. Furthermore, instructions for IRS Form 8960 detail its calculation and reporting.

2025 NIIT Thresholds (Non-Indexed)

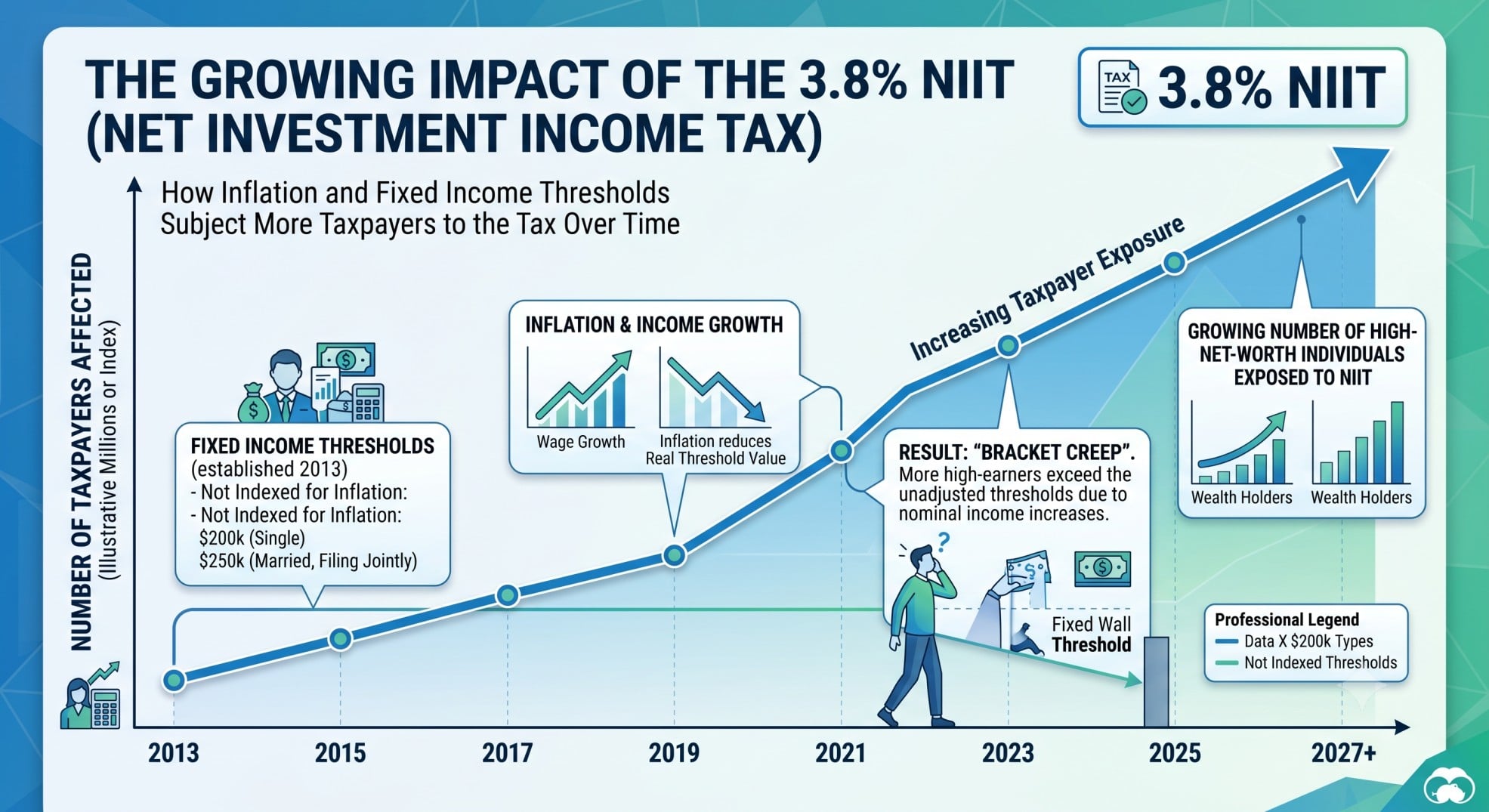

For the 2025 tax year, the Modified Adjusted Gross Income (MAGI) thresholds that trigger the 3.8% NIIT remain unchanged. They are not adjusted for inflation. This lack of indexing is the main reason for its “stealth tax” effect. As incomes rise, more taxpayers fall into its scope.

- Married Filing Jointly / Qualified Surviving Spouse: $250,000

- Single / Head of Household: $200,000

- Married Filing Separately: $125,000

For estates and trusts, the threshold is indexed for inflation. In 2025, estates and trusts face NIIT if their Adjusted Gross Income (AGI) exceeds $15,650.

What is Net Investment Income (NII)?

Net Investment Income (NII) generally includes passive income sources. These are the types of income subject to the 3.8% NIIT:

- Interest from savings accounts, CDs, and money market funds.

- Dividends, both qualified and nonqualified.

- Capital gains from selling investments, real estate, or businesses.

- Rental and royalty income, if considered passive.

- Income from businesses trading financial instruments or commodities.

- Taxable annuity payments, excluding those from IRAs.

- Income from a trade or business that is a passive activity for the taxpayer.

Income Exempt from NIIT

Certain income types are excluded from NII. These are not subject to the 3.8% NIIT:

- Wages and self-employment income.

- Social Security benefits.

- Pension and IRA distributions.

- Roth IRA withdrawals.

- Income from an active trade or business where the taxpayer materially participates.

- Life insurance proceeds.

- Interest from tax-exempt municipal bonds.

- Excluded gain from the sale of a principal residence (up to $250,000 for single filers, $500,000 for married filing jointly).

The “Stealth Tax” Trap: Beyond the 3.8%

The “stealth tax” goes beyond the direct impact of the 3.8% NIIT. Several other tax provisions quietly increase the burden on HNWIs. These factors combine to create a complex and often higher effective tax rate.

Fixed Thresholds and Purchasing Power

The individual NIIT thresholds have remained fixed since 2013. Meanwhile, inflation and investment growth continue to push more HNWIs into the NIIT’s scope. This happens without any legislative changes. For example, long-term capital gains for high earners are typically taxed at 20%. With the 3.8% NIIT, the effective federal rate becomes 23.8%. This erosion of purchasing power is an important concern for smart HNWI tax planning.

The SALT Cap’s Hidden Impact

The $10,000 federal deduction limit for State and Local Taxes (SALT) affects HNWIs. This is especially true for those in high-tax states. It effectively increases their federal taxable income. Only $10,000 of state and local taxes can be deducted. This limitation contributes to the overall “stealth tax” burden. It reduces available Itemized Deductions.

QBI Deduction’s Disappearing Act for High Earners

The Section 199A Qualified Business Income (QBI) deduction offers a 20% deduction for qualified business income. However, it phases out completely for HNWIs above certain Adjusted Gross Income (AGI) thresholds. The deduction fully phases out for married filing jointly taxpayers with AGI above certain thresholds. This eliminates a potential tax break for many high earners. It further complicates smart HNWI tax planning.

AMT’s Persistent Reach

The Alternative Minimum Tax (AMT) continues to apply to high earners. It ensures a minimum federal tax liability. The AMT often applies due to the add-back of state and local taxes. This means that even if you can deduct some SALT for regular tax purposes, it might be added back for AMT. This can result in a higher tax bill than expected.

Complex Interactions: The Interaction of Multiple Taxes

These various taxes, combined with progressive federal and state Tax Brackets, create a significantly higher effective tax rate. This rate is often higher than initially perceived. Understanding these complex interactions is crucial for effective smart HNWI tax planning. It requires a broad approach to wealth management.

Real-World Impact: The Doe Family’s 2025 “Stealth Tax” Scenario

The Doe Family Profile (2025 Tax Year):

- Filing Status: Married Filing Jointly

- Adjusted Gross Income (AGI): $400,000

- Net Investment Income (NII): $150,000 (includes $100,000 in long-term capital gains and $50,000 in dividends)

- State & Local Taxes (SALT): $30,000 (property tax and state income tax)

- Qualified Business Income (QBI): $100,000 (from a service business, AGI above phase-out)

- Other Deductions: $20,000 (mortgage interest, charitable contributions)

Impact Analysis:

- NIIT Trigger: Yes, their AGI ($400,000) exceeds the Married Filing Jointly threshold ($250,000).

- NIIT Calculation: The NIIT applies to the lesser of their NII ($150,000) or the amount their MAGI exceeds the threshold ($400,000 – $250,000 = $150,000). Therefore, $150,000 is subject to NIIT.

- NIIT Amount: $150,000 × 3.8% = $5,700.

- SALT Cap Impact: Only $10,000 of their $30,000 in SALT is deductible. This effectively increases their federal taxable income by $20,000.

- QBI Deduction: Zero. Their AGI of $400,000 is well above the 2025 phase-out threshold for MFJ.

- Effective Capital Gains Rate: The $100,000 long-term capital gain is subject to the 20% federal rate for HNWIs. Additionally, it incurs the 3.8% NIIT. This results in a 23.8% effective federal rate on that gain.

- Overall “Stealth Tax” Burden: The Doe family faces an additional $5,700 in NIIT. They also see a $20,000 increase in taxable income due to the SALT cap. Furthermore, they lose a potential QBI deduction. These factors significantly increase their overall effective tax rate beyond statutory federal income tax rates.

Strategies to Reduce the NIIT and “Stealth Tax” Traps

Smart and effective strategies are important for HNWIs. These approaches help reduce the impact of the 3.8% NIIT and other “stealth tax” burdens. Effective smart HNWI tax planning requires a broad approach.

Investment & Income Planning

- Roth Conversions: Converting traditional IRA assets to Roth IRAs can shield future growth from NIIT. While the conversion is taxable, qualified Roth withdrawals are tax-free.

- Municipal Bonds: Investing in municipal bonds generates income generally exempt from both federal income tax and the 3.8% NIIT. This is a straightforward way to reduce NII.

- Tax-Loss Harvesting & Capital Gain Timing: Strategically realizing capital losses can offset capital gains, reducing NII. Spreading large gains over multiple years can help manage MAGI.

- 1031 Like-Kind Exchanges: For real estate investors, these exchanges defer capital gains taxes and NIIT when reinvesting in similar properties.

Business & Activity Optimization

- Active Participation in Businesses: Income from an active trade or business is generally exempt from NIIT. Meeting “material participation” standards can convert passive income to active.

- Achieving “Trader Status”: For securities traders, meeting specific IRS criteria can convert investment income into business income, exempting it from NIIT.

Using Tax-Advantaged Accounts

- Prioritizing Income-Generating Investments: Place high-yield bonds or dividend stocks within tax-deferred accounts like 401(k)s and IRAs. This defers or eliminates NIIT exposure.

- Contributions Reducing MAGI: Contributions to traditional IRAs or 401(k)s can reduce your current-year MAGI. This might help keep you below NIIT thresholds.

Strategic Gifting & Estate Planning

- Gifting Appreciated Assets to Charity: Donating appreciated securities avoids realizing capital gains and the associated NIIT. It also provides a charitable deduction.

- Estate and Trust Planning: Distributing investment income from estates and trusts to beneficiaries not subject to NIIT can be an effective strategy.

Future Tax Policy Changes for 2025 and Beyond

Many provisions from the Tax Cuts and Jobs Act (TCJA) are set to expire at the end of 2025. This could lead to significant changes in the tax landscape. While the NIIT itself was not directly altered by the TCJA, these expirations could indirectly affect investment income taxation. Therefore, staying informed about potential legislative changes is an an important part of smart HNWI tax planning.

Conclusion: Your Call to Action for 2025 Tax Preparedness

The 3.8% NIIT and other “stealth tax” burdens need careful attention from high-net-worth individuals. Non-indexed thresholds and complex interactions mean general advice isn’t enough. Smart HNWI tax planning is crucial. Understanding these details can greatly affect your financial future.

We recommend consulting with a qualified and licensed tax professional or financial advisor. They can provide personalized tax planning tailored to your unique circumstances. Visit the IRS website for more general information on tax deductions and credits. Plan for 2025 now.

Disclaimer: This content is for informational purposes only. It does not constitute tax, legal, or financial advice. Tax laws are complex and subject to change. Individual circumstances vary significantly. Always consult with a qualified and licensed tax professional or financial advisor for personalized advice.

Frequently Asked Questions

What is the 3.8% Net Investment Income Tax (NIIT)?

The 3.8% NIIT is a tax applied to certain investment income for high-net-worth individuals (HNWIs) when their Modified Adjusted Gross Income (MAGI) exceeds specific thresholds. It was introduced as part of the Affordable Care Act to fund healthcare initiatives.

What are the NIIT thresholds for 2025?

For the 2025 tax year, the NIIT thresholds are not indexed for inflation and remain fixed at: $250,000 for Married Filing Jointly / Qualified Surviving Spouse, $200,000 for Single / Head of Household, and $125,000 for Married Filing Separately. For estates and trusts, the threshold is $15,650.

What types of income are subject to the 3.8% NIIT?

Net Investment Income (NII) generally includes passive income sources such as interest, dividends, capital gains from selling investments, rental and royalty income (if passive), income from businesses trading financial instruments, taxable annuity payments (excluding IRAs), and income from a passive trade or business.

What income is exempt from the NIIT?

Income types exempt from NIIT include wages, self-employment income, Social Security benefits, pension and IRA distributions, Roth IRA withdrawals, income from an active trade or business where the taxpayer materially participates, life insurance proceeds, interest from tax-exempt municipal bonds, and excluded gain from the sale of a principal residence.

Why is the NIIT considered a “stealth tax”?

The NIIT is considered a “stealth tax” because its thresholds are not adjusted for inflation. As incomes and investment values rise over time, more taxpayers are drawn into its scope without any legislative changes, effectively increasing their tax burden silently.

What are some strategies to reduce the impact of NIIT and other “stealth taxes”?

Strategies include Roth conversions, investing in municipal bonds, tax-loss harvesting, 1031 like-kind exchanges, actively participating in businesses, achieving “trader status,” prioritizing income-generating investments in tax-advantaged accounts, making contributions that reduce MAGI, and strategic gifting or estate planning.