⚡ Executive Summary: 2025 Tax Brackets & Deductions

- The 2025 tax brackets maintain the seven marginal rates of 10%, 12%, 22%, 24%, 32%, 35%, and 37%, but the income thresholds have shifted upward to account for inflation.

- The standard deduction 2025 increased significantly to $15,750 for single filers and married filing separately, and $31,500 for married couples filing jointly.

- New legislation introduced major targeted deductions for 2025, including tax-free exemptions for up to $25,000 in tip income and up to $12,500 in overtime pay.

- The State and Local Tax deduction cap was raised from $10,000 to $40,000 for the 2025 tax year.

Filing your taxes requires a clear understanding of exactly where your income falls within the federal system. The IRS adjusts income thresholds annually, and recent legislative updates have completely reshaped the baseline deductions available to everyday taxpayers. If you want to accurately project your liability for the year, you need to master the 2025 tax brackets.

We have broken down the official rates, the newly expanded standard deductions, and the exact math you need to calculate your tax bill. Let’s look at how these federal tax brackets 2025 apply to your specific financial situation.

Table of Contents

- How the 2025 Tax Brackets Work

- The Official Tax Brackets 2025 Chart

- The Standard Deduction 2025: Massive Increases

- Step-by-Step: How to Calculate Your 2025 Taxes

- New Deductions Impacting Federal Tax Brackets 2025

- State Taxes vs. Federal Tax Brackets

- Capital Gains Tax Rates 2025

- Frequently Asked Questions About 2025 Tax Brackets

How the 2025 Tax Brackets Work

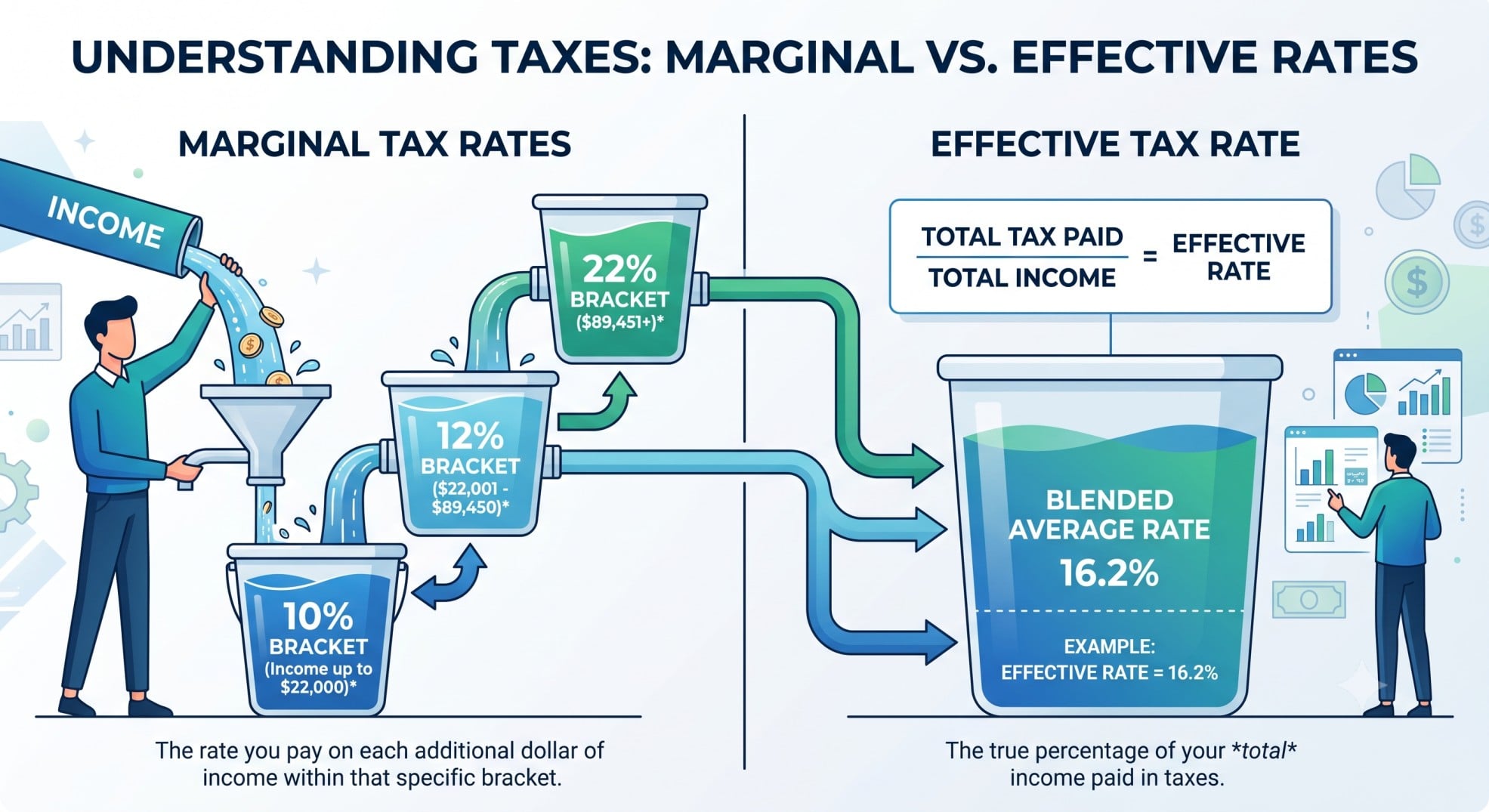

The United States uses a progressive tax system. This means your income is divided into chunks, and each chunk is taxed at a progressively higher rate. You do not pay a single flat percentage on everything you earn.

Many taxpayers mistakenly believe that moving into a higher tax bracket means all their income gets taxed at that new, higher rate. That is mathematically false. When your income crosses into a new bracket, only the dollars that fall inside that specific tier are taxed at the higher rate. The rest of your income is still taxed at the lower rates of the previous brackets.

Think of the 2025 tax brackets as a series of buckets. You fill the 10% bucket first. Once that bucket is full, the overflow goes into the 12% bucket. When the 12% bucket fills up, the rest spills into the 22% bucket, and so on. This system ensures that your effective tax rate—the actual percentage of your total income that goes to the IRS—is always lower than your top marginal tax bracket.

The Official Tax Brackets 2025 Chart

To determine your top marginal rate, you need to look at your taxable income—not your gross salary. Taxable income is what remains after you subtract your standard or itemized deductions. Reviewing the tax brackets 2025 chart below will help you identify exactly where your final dollars are taxed.

Here are the official income tax brackets 2025 for all major filing statuses, including the often-overlooked married filing separately category.

2025 Tax Brackets Single Filers

The 2025 tax brackets single tiers apply to unmarried individuals who do not qualify for head of household status.

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 to $11,925 |

| 12% | $11,926 to $48,475 |

| 22% | $48,476 to $103,350 |

| 24% | $103,351 to $197,300 |

| 32% | $197,301 to $250,525 |

| 35% | $250,526 to $626,350 |

| 37% | $626,351 or more |

2025 Tax Brackets Married Filing Jointly

Couples should review the 2025 tax brackets married filing jointly before deciding whether to file together or separately. Filing jointly generally provides wider income bands, keeping more of your combined income in lower tax tiers.

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 to $23,850 |

| 12% | $23,851 to $96,950 |

| 22% | $96,951 to $206,700 |

| 24% | $206,701 to $394,600 |

| 32% | $394,601 to $501,050 |

| 35% | $501,051 to $751,600 |

| 37% | $751,601 or more |

2025 Tax Brackets Married Filing Separately

If you are married but choose to keep your tax liabilities distinct, you will use these brackets. The thresholds are exactly half of the joint filing amounts. This status is often chosen when one spouse has significant medical deductions or is enrolled in an income-driven student loan repayment plan.

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 to $11,925 |

| 12% | $11,926 to $48,475 |

| 22% | $48,476 to $103,350 |

| 24% | $103,351 to $197,300 |

| 32% | $197,301 to $250,525 |

| 35% | $250,526 to $375,800 |

| 37% | $375,801 or more |

2025 Tax Brackets Head of Household

To qualify for these more favorable rates, you must be unmarried and pay for more than half the costs of keeping up a home for a qualifying dependent.

| Tax Rate | Taxable Income Range |

|---|---|

| 10% | $0 to $17,000 |

| 12% | $17,001 to $64,850 |

| 22% | $64,851 to $103,350 |

| 24% | $103,351 to $197,300 |

| 32% | $197,301 to $250,525 |

| 35% | $250,526 to $626,350 |

| 37% | $626,351 or more |

Keep a copy of the tax brackets 2025 chart for your records as you plan your estimated quarterly payments or adjust your W-4 withholdings. Adjusting your payroll withholdings early in the year prevents surprise tax bills next April.

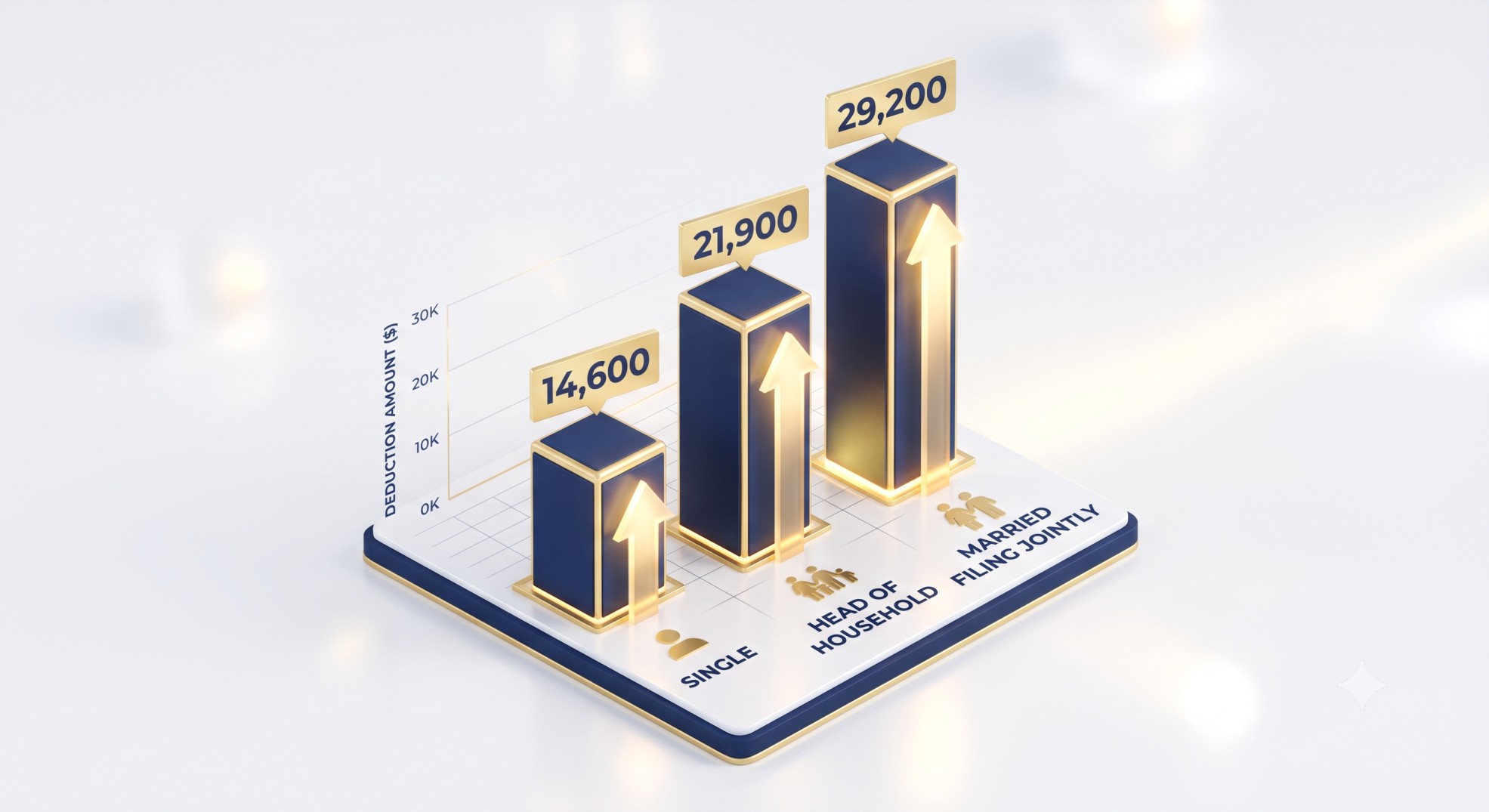

The Standard Deduction 2025: Massive Increases

Before you apply the percentages from the tax brackets 2025 chart, you get to reduce your gross income by either taking the standard deduction or itemizing your deductions. Because of recent legislative updates under the One Big Beautiful Bill Act, the standard deduction 2025 saw a massive increase.

Here are the baseline standard deduction amounts for the 2025 tax year:

- Single Filers: $15,750

- Married Filing Jointly: $31,500

- Head of Household: $23,625

- Married Filing Separately: $15,750

If you are 65 or older, or blind, the IRS grants an additional standard deduction. For 2025, this extra amount is $2,000 for Single or Head of Household filers, and $1,600 per qualifying individual for Married Filing Jointly.

But the biggest change for seniors in 2025 is the introduction of a brand-new, standalone $6,000 deduction for individuals age 65 and older. This deduction stacks on top of the standard deduction. It begins to phase out if your modified adjusted gross income exceeds $75,000 for singles or $150,000 for married couples.

Step-by-Step: How to Calculate Your 2025 Taxes

Understanding your personal tax rate 2025 requires doing the actual math. Let’s walk through four realistic hypothetical scenarios to show exactly how the standard deduction 2025 and the marginal brackets interact.

Example 1: The Single Filer

Maria is a single graphic designer earning a gross salary of $85,000 in 2025. She does not itemize, so she claims the standard deduction.

- Gross Income: $85,000

- Minus Standard Deduction: -$15,750

- Taxable Income: $69,250

Now, we push her $69,250 taxable income through the single tiers:

- 10% Bracket: The first $11,925 is taxed at 10% = $1,192.50

- 12% Bracket: The income from $11,926 to $48,475 is taxed at 12% = $4,386.00

- 22% Bracket: The remaining income from $48,476 to $69,250 is taxed at 22% = $4,570.50

Maria’s total federal tax liability is $10,149.00. Even though she hit the 22% tax bracket 2025, her effective tax rate is only about 11.9%.

Example 2: Married Filing Jointly with Overtime

David and Sarah are married and file jointly. David earns a base salary of $130,000, and Sarah does not work. This year, David also earned $10,000 in mandatory overtime pay, bringing their gross household income to $140,000. Under the new 2025 rules, up to $25,000 of overtime pay is tax-deductible for joint filers.

- Gross Income: $140,000

- Minus Overtime Deduction: -$10,000

- Adjusted Gross Income: $130,000

- Minus Standard Deduction: -$31,500

- Taxable Income: $98,500

Now we apply the 2025 tax brackets married filing jointly:

- 10% Bracket: The first $23,850 is taxed at 10% = $2,385.00

- 12% Bracket: The income from $23,851 to $96,950 is taxed at 12% = $8,772.00

- 22% Bracket: The remaining income from $96,951 to $98,500 is taxed at 22% = $341.00

Their total federal tax liability is $11,498.00. By utilizing the new overtime deduction and the expanded standard deduction, they shielded $41,500 of their income from federal taxes entirely.

Example 3: Married Filing Separately

James and Emily are married but choose to file separately because James is on an income-driven repayment plan for his student loans. James earns $60,000 a year. By filing separately, his student loan payment is calculated only on his income, not their combined household income.

- Gross Income: $60,000

- Minus Standard Deduction: -$15,750

- Taxable Income: $44,250

Pushing his $44,250 taxable income through the married filing separately brackets:

- 10% Bracket: The first $11,925 is taxed at 10% = $1,192.50

- 12% Bracket: The remaining $32,325 is taxed at 12% = $3,879.00

James owes $5,071.50 in federal income tax 2025. He never touches the 22% bracket.

Example 4: The Senior Filer

Robert is a 68-year-old single retiree with $60,000 in gross taxable income for 2025. Because of his age, he qualifies for multiple baseline deductions.

- Standard Deduction: $15,750

- Age 65+ Additional Deduction: $2,000

- New Senior Deduction: $6,000

- Total Deductions: $23,750

- Taxable Income: $60,000 – $23,750 = $36,250

Pushing his $36,250 taxable income through the brackets:

- 10% Bracket: The first $11,925 is taxed at 10% = $1,192.50

- 12% Bracket: The remaining $24,325 is taxed at 12% = $2,919.00

Robert’s total federal tax liability is just $4,111.50.

New Deductions Impacting Federal Tax Brackets 2025

The 2025 tax year introduces several highly targeted deductions that directly lower your adjusted gross income before the federal tax brackets 2025 are even applied. If you qualify for these, your tax 2025 liability will drop significantly.

The Tip Income Deduction

Service industry workers can now deduct up to $25,000 of qualified tip income from their federal taxes. This deduction phases out if your modified adjusted gross income exceeds $150,000 for single filers or $300,000 for married couples. Reporting tip income correctly on your W-2 is required to claim this benefit.

The Overtime Pay Deduction

If you earn time-and-a-half overtime pay required by the Fair Labor Standards Act, you can deduct up to $12,500 of that premium pay as a single filer, or up to $25,000 if married filing jointly. The same income phase-outs apply.

The Auto Loan Interest Deduction

For vehicles purchased between January 1, 2025, and December 31, 2028, taxpayers can deduct up to $10,000 in auto loan interest annually. The vehicle must be for personal use and assembled in the United States. This deduction phases out for taxpayers earning over $100,000 as a single filer or $200,000 for joint filers.

The Expanded SALT Deduction

For taxpayers who itemize rather than taking the standard deduction 2025, the State and Local Tax deduction cap has been raised. Previously stuck at $10,000, the cap is now $40,000 for the 2025 tax year. This is a massive benefit for high earners living in states with heavy income or property taxes. The deduction begins to phase out once your adjusted gross income hits $500,000.

State Taxes vs. Federal Tax Brackets

The irs tax brackets 2025 only dictate what you owe the federal government. You must calculate your state income taxes separately. State tax systems vary wildly across the country.

Some states, like California and New York, use progressive tax brackets similar to the federal system. Other states, like Pennsylvania and Utah, charge a flat income tax rate regardless of how much you earn. Meanwhile, states like Texas, Florida, and Nevada charge zero state income tax.

If you are a US citizen living abroad, your situation is even more complex. The United States taxes based on citizenship, not residency. This means US expats must file federal returns using the 2025 income tax brackets regardless of where they live. For example, if you live and work in Kuala Lumpur, you must evaluate the lhdn tax rate 2025 alongside your US federal obligations. You can usually claim the Foreign Earned Income Exclusion or Foreign Tax Credit to avoid double taxation, but the filing requirement remains strict.

Capital Gains Tax Rates 2025

The 2025 tax brackets we discussed above apply to ordinary income—things like W-2 wages, 1099 contract work, and short-term capital gains. If you sell an asset you have held for longer than one year, you unlock preferential long-term capital gains tax rates.

For 2025, the long-term capital gains rates remain 0%, 15%, and 20%, but the income thresholds have increased:

- 0% Rate: Applies to taxable income up to $48,350 for single filers or $96,700 for married filing jointly.

- 15% Rate: Applies to taxable income from $48,351 to $533,400 for single filers or $96,701 to $600,050 for married filing jointly.

- 20% Rate: Applies to taxable income over $533,400 for single filers or $600,050 for married filing jointly.

High earners may also be subject to the 3.8% Net Investment Income Tax if their modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married couples filing jointly.

Frequently Asked Questions About 2025 Tax Brackets

What are the 2025 tax brackets?

The 2025 tax brackets are the seven marginal income tiers set by the IRS: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. The specific income ranges for each tier adjust annually for inflation and dictate your federal tax liability.

How much is the standard deduction 2025?

The standard deduction for 2025 is $15,750 for single filers and married individuals filing separately, $31,500 for married couples filing jointly, and $23,625 for heads of household.

What are the 2025 tax brackets married filing jointly?

For married couples filing jointly in 2025, the 10% bracket covers income up to $23,850. The 12% bracket goes up to $96,950, the 22% up to $206,700, the 24% up to $394,600, the 32% up to $501,050, the 35% up to $751,600, and the 37% bracket applies to income over $751,600.

Did the SALT deduction limit change for 2025 taxes?

Yes. For the 2025 tax year, the State and Local Tax deduction limit increased from $10,000 to $40,000. This higher cap begins to phase out for taxpayers with an adjusted gross income over $500,000.

How does the new overtime deduction work for income tax 2025?

Starting in 2025, you can deduct up to $12,500 as a single filer or $25,000 as a joint filer of qualified overtime pay from your taxable income. This applies to the premium portion of time-and-a-half pay and phases out for high earners.

Are the irs tax brackets 2025 different from 2024?

The seven percentage rates remain exactly the same as 2024, but the income thresholds for the irs tax brackets 2025 have been increased to account for inflation, allowing you to earn more money before hitting a higher tax rate.

What is the personal tax rate 2025 for capital gains?

Long-term capital gains are taxed at 0%, 15%, or 20% depending on your overall taxable income. Short-term capital gains, which are assets held for one year or less, are taxed at your ordinary income tax rate 2025.

Where can I find a reliable tax brackets 2025 chart?

You can find the official tax brackets 2025 chart directly in this guide, which reflects the exact inflation-adjusted figures released by the IRS and the Treasury Department for the current tax year.

How do state taxes interact with federal tax brackets 2025?

State taxes operate completely independently of the federal tax brackets 2025. You must calculate your federal liability using the IRS brackets, and then calculate your state liability using your specific state’s flat or progressive tax code.

Do US expats pay the lhdn tax rate 2025 or US taxes?

US expats living in Malaysia must navigate both. They are subject to the lhdn tax rate 2025 for their local Malaysian tax obligations, but because the US taxes global income, they must also file a US return using the 2025 federal brackets. Expats typically use the Foreign Tax Credit to avoid double taxation.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.