Knowing how your Social Security benefits are taxed, along with other income, is important for retirement planning. For older adults, unexpected tax bills can greatly affect financial security. This article explains Social Security taxation 2026 clearly, helping you plan and avoid surprises. We will look at how your other income sources affect your benefits. We will also offer strategies to improve your tax situation, helping you keep more of your earnings.

Executive Summary

- Your Social Security benefits may be taxed federally based on your “provisional income.”

- Provisional income thresholds for Social Security taxation 2026 are not indexed for inflation, pushing more individuals into taxable tiers.

- Up to 85% of your benefits can be included in your taxable income, depending on your provisional income level.

- Other income sources like pensions, investments, and RMDs greatly affect your provisional income.

- Proactive tax planning strategies, such as Roth conversions and Qualified Charitable Distributions (QCDs), can help manage your tax bill.

- A new, temporary OBBBA Older Adult Bonus Deduction can reduce your taxable income, but it does not lower your provisional income for Social Security purposes.

Understanding How Your Social Security Benefits Are Taxed

The federal government may tax a portion of your Social Security benefits. This depends on your total income. The rules for this taxation come from Internal Revenue Code (IRC) Section 86. The IRS also provides detailed guidance in IRS Publication 915, “Social Security and Equivalent Railroad Retirement Benefits.”

The “Provisional Income” Calculation

Your “provisional income” is how the IRS decides if your Social Security benefits are taxable. The IRS also calls this “combined income.” It includes three main parts:

- Your Adjusted Gross Income (AGI), not counting your Social Security benefits.

- Any tax-exempt interest you receive, such as from municipal bonds.

- Fifty percent (50%) of your total Social Security benefits for the year.

You add these three amounts together to get your provisional income. This figure then determines which tax thresholds apply to you.

2026 Federal Provisional Income Thresholds

The amount of your Social Security benefits subject to tax depends on your provisional income and your filing status. These thresholds are important for tax planning.

- For Single filers, Head of Household, or Qualifying Widow(er):

- If your provisional income is below $25,000: None of your Social Security benefits are taxable.

- If your provisional income is between $25,000 and $34,000: Up to 50% of your Social Security benefits may be taxed.

- If your provisional income exceeds $34,000: Up to 85% of your Social Security benefits may be taxed.

- For Married Filing Jointly:

- If your provisional income is below $32,000: None of your Social Security benefits are taxable.

- If your provisional income is between $32,000 and $44,000: Up to 50% of your Social Security benefits may be taxed.

- If your provisional income exceeds $44,000: Up to 85% of your Social Security benefits may be taxed.

- For Married Filing Separately (and lived with spouse at any time during the year): Up to 85% of your Social Security benefits are taxable on any positive provisional income. This effectively means there is no lower threshold for this group.

It is important to remember that these provisional income thresholds have not changed since 1984. They are not adjusted for inflation. Therefore, more older adults find their benefits taxed over time.

Clarifying the “Up To” Percentage

The phrases “up to 50%” or “up to 85%” can be confusing. They refer to the maximum portion of your Social Security benefits that might be included in your taxable income. They do not refer to the tax rate you will pay. Your actual tax bracket determines the rate applied to that taxable portion. For example, if 85% of your benefits are taxable, that amount is added to your other income. Then, your marginal tax rate applies to that combined total.

Real-World Scenario: Eleanor Vance’s 2026 Tax Journey

Meet Eleanor Vance: An Older Adult’s Tax Journey in California

Eleanor Vance is a 72-year-old widow living in California. She relies on her Social Security benefits, a small pension, and some investment income. She wants to understand her Social Security taxation 2026.

Eleanor’s Estimated 2026 Income:

- Social Security Benefits: $24,000 ($2,000/month, reflecting a 2.8% COLA increase for 2026).

- Pension Income: $10,000 (taxable).

- Taxable Interest & Dividends: $3,000.

- Tax-Exempt Municipal Bond Interest: $2,000.

- Total Gross Income: $39,000.

Understanding Social Security Taxation

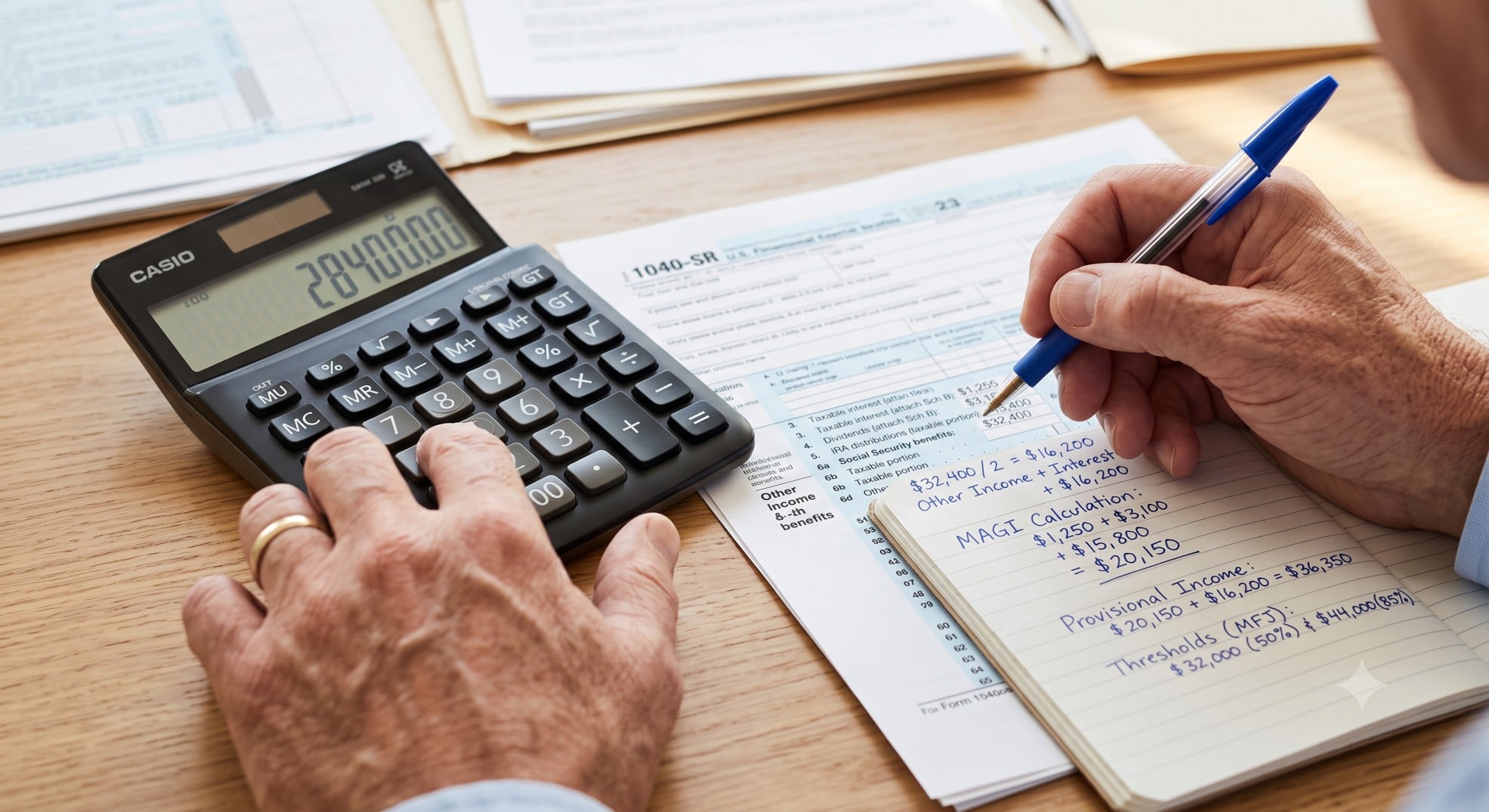

Eleanor is a single filer. She needs to calculate her provisional income to see how much of her Social Security benefits will be taxed. Her Standard Deduction for 2026 is estimated at $17,600 (base $14,600 + age 65+ $1,750 + single $1,250). However, the OBBBA Older Adult Bonus Deduction is also available.

The Numbers for Eleanor Vance

- Calculate Provisional Income:

- AGI (excluding SS benefits): $10,000 (Pension) + $3,000 (Taxable Interest) = $13,000

- Plus Tax-Exempt Interest: $2,000

- Plus 50% of Social Security Benefits: 0.50 * $24,000 = $12,000

- Eleanor’s Provisional Income: $13,000 + $2,000 + $12,000 = $27,000

- Determine Taxable Portion of Social Security:

- Eleanor’s provisional income ($27,000) falls between $25,000 and $34,000 for a single filer.

- This means up to 50% of her Social Security benefits are taxable.

- The calculation is: (Provisional Income – $25,000) * 0.50 = ($27,000 – $25,000) * 0.50 = $2,000 * 0.50 = $1,000.

- Also, 50% of her Social Security benefits is $12,000.

- The taxable amount is the lesser of $1,000 or $12,000.

- Taxable Social Security Benefits: $1,000

- Calculate Eleanor’s AGI:

- Pension: $10,000

- Taxable Interest: $3,000

- Taxable Social Security: $1,000

- Eleanor’s AGI: $10,000 + $3,000 + $1,000 = $14,000

- Calculate Taxable Income:

- Eleanor’s AGI: $14,000

- Her Standard Deduction for 2026 is $17,600.

- Additionally, she qualifies for the OBBBA Older Adult Bonus Deduction of $6,000.

- Her total deduction is $17,600 + $6,000 = $23,600.

- Since her AGI ($14,000) is less than her total deduction ($23,600), her Taxable Income is $0.

Takeaway

Even though Eleanor’s Social Security benefits were partially taxable, her large Standard Deduction and the new OBBBA Older Adult Bonus Deduction resulted in zero federal taxable income. This scenario highlights how different tax rules interact. It also shows the importance of calculating all components of your income and deductions.

Key Factors Influencing Your Social Security Tax Bill in 2026

Several things can increase the taxable portion of your Social Security benefits. Knowing these helps with tax planning.

The Impact of Other Income Sources

Your provisional income includes more than just your Social Security benefits. Other income sources greatly affect your Social Security taxation 2026. These include:

- Pensions: Distributions from traditional pensions are fully taxable.

- Investment Income: Interest, dividends, and capital gains from investments increase your AGI.

- Required Minimum Distributions (RMDs): Withdrawals from traditional IRAs and 401(k)s after age 73 (or 75 for those born in 1960 or later) are taxable. They directly increase your AGI.

- Part-Time Work: Any wages earned from working in retirement also add to your AGI.

All these income streams contribute to your provisional income calculation. Therefore, they can push you into a higher Social Security taxation bracket.

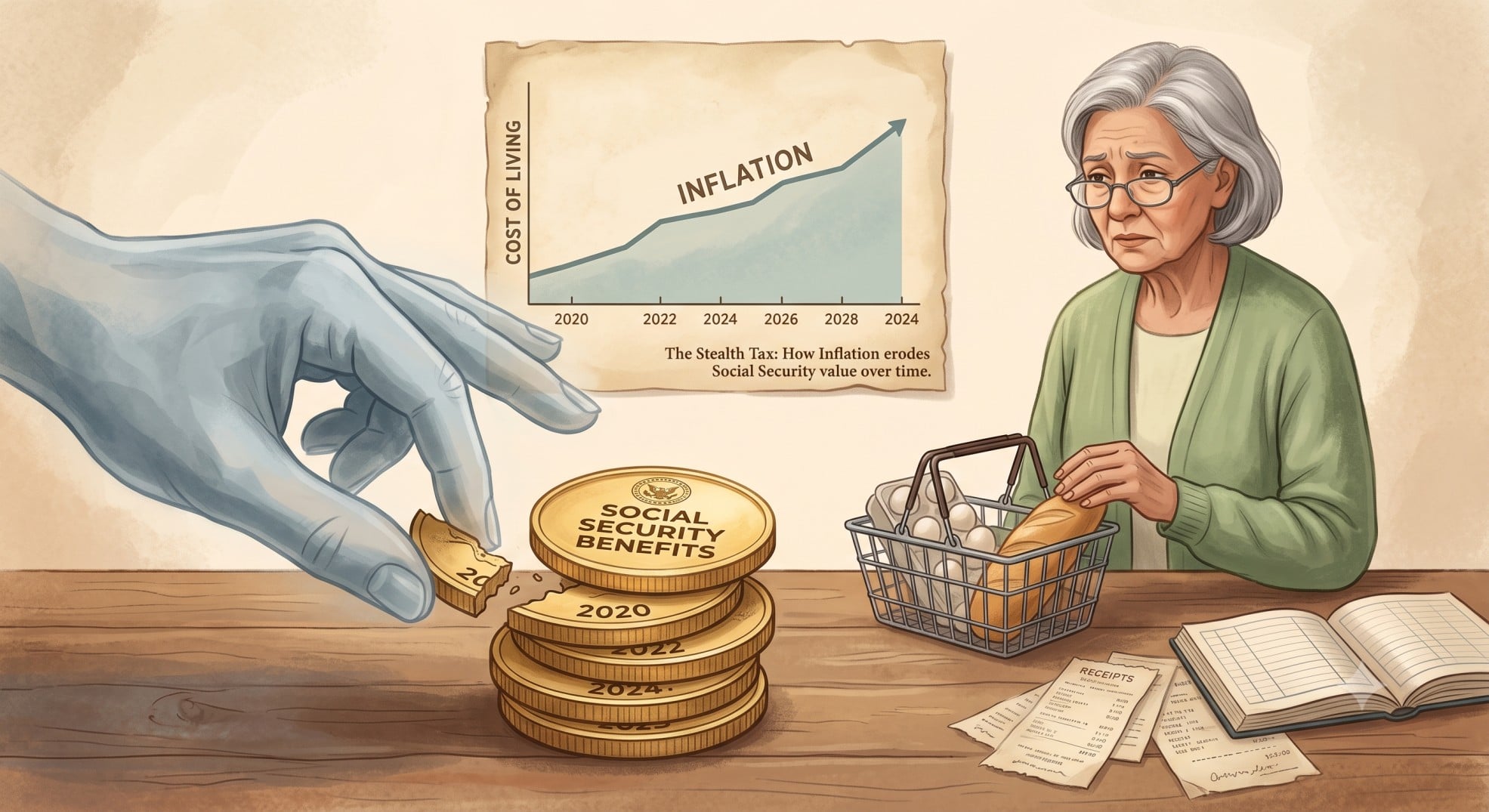

Why Inflation Matters: The “Stealth Tax”

As mentioned, the provisional income thresholds for Social Security taxation have not changed since 1984. However, Social Security benefits receive annual Cost-of-Living Adjustments (COLAs). Other income sources also tend to grow over time. This combination means that more and more older adults find a portion of their Social Security benefits subject to federal income tax. This effect is often called a “stealth tax.” It erodes the purchasing power of your benefits without any change in tax law.

State-Level Taxation of Social Security

While this article focuses on federal Social Security taxation, it is important to note that some states also tax Social Security benefits. For instance, California does not tax Social Security benefits. However, other states do. This adds another layer of complexity to your overall tax picture. Always check your state’s specific tax laws.

Proactive Tax Planning Strategies for Older Adults

Smart tax planning can help you manage your provisional income. This can reduce the amount of Social Security benefits subject to tax. Here are some strategies for Social Security taxation 2026.

Roth Conversions

Converting funds from a traditional IRA or 401(k) to a Roth IRA can be a good strategy. You pay taxes on the converted amount in the year of conversion. However, qualified withdrawals from a Roth IRA in retirement are tax-free. They also do not count towards your AGI or provisional income. This can greatly reduce future RMDs and lower your provisional income in retirement years.

Qualified Charitable Distributions (QCDs)

If you are 70½ or older and charitably inclined, a Qualified Charitable Distribution (QCD) can be beneficial. You can donate up to $111,000 directly from your IRA to a qualified charity in 2026. This distribution counts towards your RMD for the year. However, it is not included in your AGI. This helps manage your provisional income and potentially reduces your Social Security taxation 2026.

Strategic Withdrawal Order

Consider the order in which you withdraw funds from your retirement accounts. Prioritizing withdrawals from tax-free accounts (like Roth IRAs) or taxable brokerage accounts before tax-deferred accounts can keep your AGI lower. This strategy helps manage your provisional income. It can also reduce the taxable portion of your Social Security benefits.

Understanding Tax-Exempt Investments

Municipal bonds offer federally tax-exempt interest. However, this interest still counts towards your provisional income. While it is not taxed directly, it can push you over the provisional income thresholds. Consequently, more of your Social Security benefits may become taxable. Therefore, it is important to consider this when evaluating such investments.

Important 2026 Tax Figures & Updates

Staying informed about key figures and legislative changes is important for tax planning.

2026 Social Security COLA

Social Security and Supplemental Security Income (SSI) benefits will increase by 2.8% in 2026. This adjustment begins with payments in January 2026 for Social Security beneficiaries. While beneficial, this COLA can also contribute to higher provisional income.

Maximum Taxable Earnings for Social Security (Wage Base)

For 2026, the maximum amount of earnings subject to Social Security tax (OASDI) is $184,500. This is an increase from $176,100 in 2025. The Social Security tax rate remains at 6.2% for employees and employers.

Medicare Part B Premiums

The standard monthly rate for Medicare Part B in 2026 is projected to be $202.90. This is an increase from $185 in 2025. This increase can partially offset the COLA gain for many beneficiaries.

One Big Beautiful Bill Act (OBBBA) Older Adult Bonus Deduction

The OBBBA introduced a new, temporary deduction for older adults. If you are 65 or older, you can claim an additional $6,000 deduction. Joint filers, where both are 65+, can claim $12,000. This deduction applies if your Modified Adjusted Gross Income (MAGI) is under $175,000 ($250,000 for joint filers). This deduction reduces your taxable income. However, it does not directly lower your provisional income for Social Security taxation 2026 purposes.

What If You Repay Benefits? Recent Tax Court Insights

The IRS maintains strict rules regarding Social Security benefits and repayments. Recent Tax Court cases provide important clarifications.

- In Smith v. Commissioner, T.C. Memo. 2026-25, the court confirmed that benefits are taxable in the year received. Repayments made in later years cannot offset the tax liability for the year the benefits were initially received. This is due to the “claim of right” doctrine.

- Ecret v. Commissioner, T.C. Memo. 2024-23, clarified the interaction between workers’ compensation and Social Security benefits. If workers’ compensation reduces your Social Security disability payments, the portion of workers’ compensation equal to that reduction is treated as a taxable Social Security benefit. This can make otherwise non-taxable workers’ compensation taxable.

These cases highlight the importance of understanding the timing of income and how different benefit programs interact. Always consult with a tax professional if you face such situations.

Conclusion

Understanding the rules for Social Security taxation 2026 is important for financial planning. The non-indexed provisional income thresholds mean that proactive tax planning is more important than ever for older adults. Strategies like Roth conversions, QCDs, and strategic withdrawals can help manage your tax liability. Staying informed about key figures and legislative updates is also important.

We strongly recommend consulting with a qualified tax professional or financial advisor. They can provide personalized advice tailored to your specific situation. This ensures you make the best financial decisions for your retirement.

Disclaimer

This article provides general information for the 2026 tax year based on current laws, regulations, and projections. Tax laws are complex and subject to change.

The information presented here is not intended as tax, legal, or financial advice.

Readers should consult with a qualified tax professional, financial advisor, or attorney to discuss their specific situation and to receive personalized advice tailored to their individual circumstances.

Always refer to official IRS publications and the Social Security Administration for the most up-to-date and definitive information.