Table of Contents

- Understanding the 15.3% Self-Employment Tax in 2026

- Calculating Your Self-Employment Tax (Schedule SE)

- Real-World Scenario: Alex, The Freelance Software Developer

- Strategic Tax Planning for Freelancers

- Beyond the Basics: Advanced Considerations for Freelancers

- Essential Resources and Professional Guidance

Self-employment comes with a kind of freedom no office job can match. But that freedom carries a price tag most new freelancers don’t see coming: the 15.3% self-employment tax. This isn’t some obscure line item buried in your return. It’s your direct contribution to Social Security and Medicare, and getting it right matters for your long-term financial health.

For 2026, the rules around this tax have specific numbers and thresholds you need on your radar. Solid tax planning 2026 starts with understanding exactly how this tax works, what it costs you, and where you can legally reduce that cost. That’s what this guide walks through.

⚡ Executive Summary: Key Takeaways for Freelancers

- The self-employment tax rate holds steady at 15.3% for 2026, covering both Social Security and Medicare.

- The Social Security wage base limit for 2026 is $184,500.

- You can deduct one-half of your self-employment tax, which lowers your Adjusted Gross Income (AGI).

- Quarterly estimated tax payments aren’t optional; skipping them triggers penalties.

- Maximizing business deductions and the Qualified Business Income (QBI deduction) can meaningfully cut your tax bill.

- Careful record-keeping paired with professional advice keeps you compliant and stress-free.

Understanding the 15.3% Self-Employment Tax in 2026

What Exactly Is Self-Employment Tax?

Self-employment tax is your contribution to Social Security and Medicare, paid directly instead of through payroll withholding. Traditional employees pay the same taxes under the FICA umbrella, split between them and their employer. As a self-employed worker, you cover both halves yourself, which is exactly what funds your future Social Security and Medicare benefits.

Who Actually Has to Pay This Tax?

You owe self-employment tax once your net earnings from self-employment hit $400 or more.

That threshold applies broadly. Freelancers, independent contractors, sole proprietors, and business partners all fall under this rule. Basically, if you’re earning income outside a standard employer-employee arrangement, this tax almost certainly applies to you.

Key Tax Rules and Rates for 2026

A handful of specific figures drive your calculations for the 2026 tax year. Knowing these numbers cold makes your tax planning 2026 far more accurate.

- Self-Employment Tax Rate: The rate sits at 15.3%, split between 12.4% for Social Security and 2.9% for Medicare.

- Social Security Wage Base Limit (2026): Earnings up to $184,500 face the 12.4% Social Security portion. Anything above that limit escapes Social Security tax entirely.

- Medicare Tax Limit: No wage base cap exists for the 2.9% Medicare portion. Every dollar of net self-employment earnings gets taxed for Medicare.

- Additional Medicare Tax (0.9%): High earners face an extra 0.9% Medicare tax above certain thresholds: $200,000 for single filers, $250,000 for married filing jointly, and $125,000 for married filing separately in 2026.

- Deduction for One-Half of SE Tax: Half of your total self-employment tax is deductible from gross income, directly reducing your AGI.

- Net Earnings Calculation: Only 92.35% of your net profit gets subjected to self-employment tax, an adjustment that accounts for the employer’s share of FICA.

- Minimum Net Earnings: The $400 threshold triggers your obligation to pay.

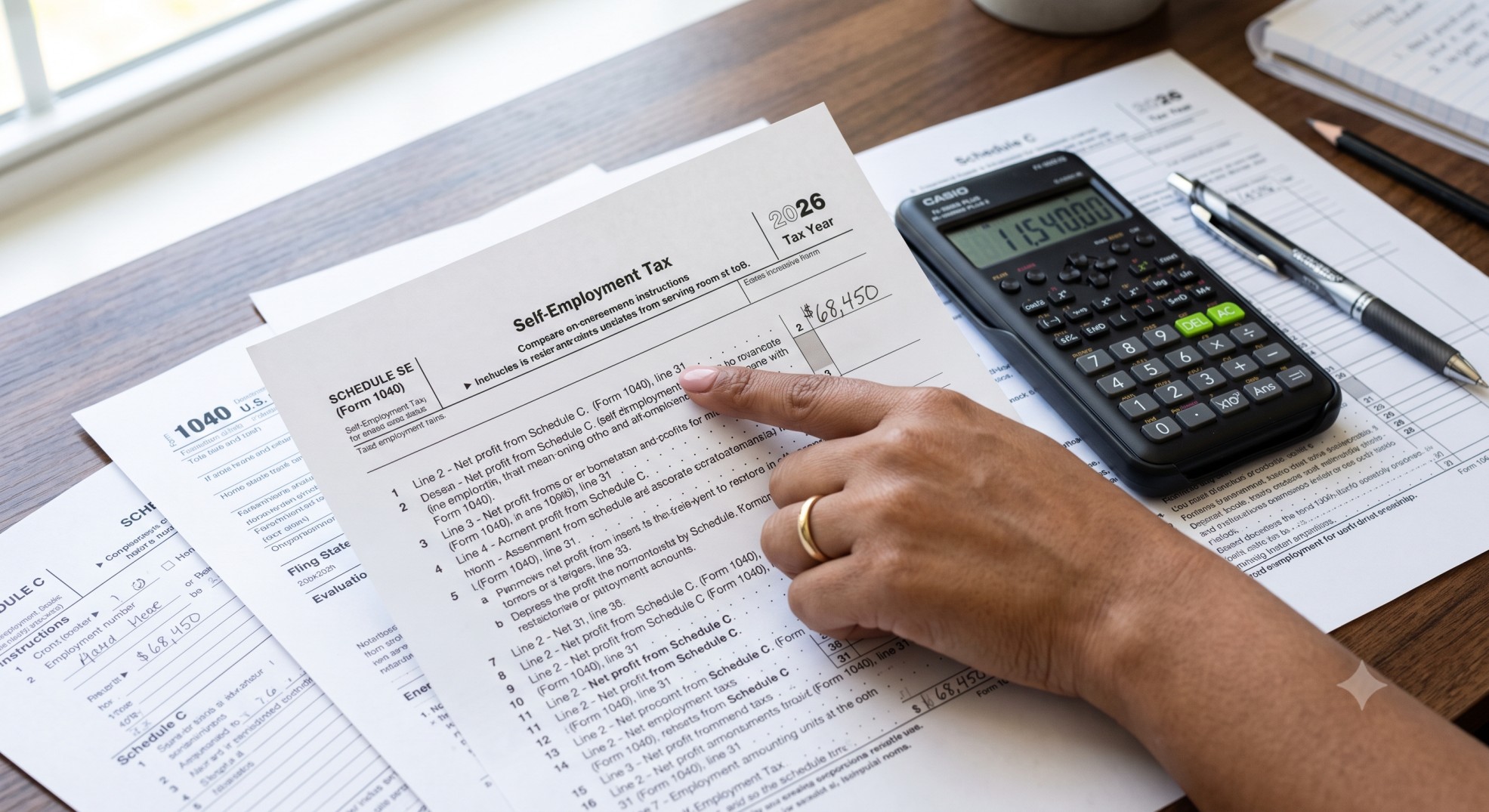

Calculating Your Self-Employment Tax (Schedule SE)

Getting to your final self-employment tax number takes a few clear steps, all of which feed into Schedule SE, Form 1040.

Step-by-Step Calculation Process

Here’s how the math breaks down:

- Determine Net Earnings: Subtract total business expenses from total business income to land on your net earnings from self-employment.

- Apply the 92.35% Rule: Multiply net earnings by 92.35% to find the portion subject to self-employment tax.

- Calculate Social Security Tax: Multiply that figure by 12.4%, capped at the 2026 wage base limit of $184,500.

- Calculate Medicare Tax: Multiply the same figure by 2.9%, with no income ceiling.

- Add Additional Medicare Tax: If your earnings clear the relevant threshold, tack on 0.9% for the applicable portion.

- Total SE Tax: Add together the Social Security, Medicare, and any Additional Medicare tax amounts.

- Deductible Half: Divide your total self-employment tax by two; that number is deductible on Form 1040.

Essential Forms: Schedule SE and Form 1040-ES

Schedule SE (Form 1040) is where you calculate your self-employment tax, capturing net earnings and applying the correct rates and limits. Form 1040-ES, Estimated Tax for Individuals, handles the other side of the equation, helping you calculate and pay quarterly estimated taxes so you stay current throughout the year.

Real-World Scenario: Alex, The Freelance Software Developer (2026 Tax Year)

Case Study: Alex, The Freelance Software Developer

Meet Alex, a freelance software developer living in California and filing as a single taxpayer.

Alex juggles self-employment taxes, state income tax, and a handful of deductions. This scenario walks through Alex’s full 2026 tax picture, spotlighting the 15.3% self-employment tax alongside the other moving pieces.

Alex’s Financial Snapshot (2026 Estimates)

- Gross Freelance Income: $200,000

- Business Expenses: $30,000 (software, home office, professional development)

- Net Self-Employment Earnings: $170,000

- Investment Income: $25,000

- Self-Employed Health Insurance Premiums: $8,000

- SEP IRA Contribution: $25,000

- Property Taxes: $7,000

- Mortgage Interest: $15,000

- Charitable Contributions: $5,000

The Tax Calculation Journey

- Net Self-Employment Earnings:

Subtracting business expenses from gross income gives Alex a clear profit figure.

- Calculated Net SE Earnings: $170,000

- Self-Employment (SE) Tax:

This tax covers Social Security and Medicare, applied to 92.35% of net earnings. For 2026, the Social Security wage base is $184,500.

- SE Taxable Earnings (92.35% of Net SE Earnings): $157,095.00

- Social Security Tax (12.4% up to wage base): $19,480.00 (below the $184,500 wage base)

- Medicare Tax (2.9% on all SE Taxable Earnings): $4,555.76

- Total Self-Employment Tax: $24,035.76

- Deductible Half of SE Tax (reduces AGI): $12,017.88

- Adjusted Gross Income (AGI):

AGI shapes eligibility for many deductions and credits, calculated after certain above-the-line deductions.

- Calculated AGI: $149,982.12 (Gross Income + Investment Income – Business Expenses – Deductible Half SE Tax – Health Insurance – SEP IRA)

- California State Income Tax:

As a California resident, Alex owes state income tax, calculated first to determine the state tax portion of federal itemized deductions.

- CA Taxable Income: $123,982.12 (AGI minus CA Itemized Deductions of $26,000, higher than the CA Standard Deduction of $6,000)

- Calculated CA Income Tax: $9,036.30

- Federal Deductions (Itemized vs. Standard):

Alex weighs the standard deduction against itemized deductions, which include the capped State and Local Tax (SALT) amount.

- Federal Itemized SALT (capped at $10,000): $10,000.00 (Property Tax + CA Income Tax, capped)

- Total Federal Itemized Deductions: $30,000.00 (SALT Cap + Mortgage Interest + Charitable Contributions)

- 2026 Standard Deduction (Single, estimated): $15,500.00

- Deduction Chosen (Itemized): $30,000.00

- Qualified Business Income (QBI) Deduction (Section 199A):

The QBI deduction allows eligible self-employed taxpayers to deduct up to 20% of qualified business income. Alex’s taxable income falls below the estimated 2026 lower threshold for single filers (~$201,200), so the deduction equals the lesser of 20% of QBI or 20% of taxable income before the QBI deduction.

- Federal Taxable Income (before QBI deduction): $119,982.12 (AGI minus Chosen Deduction)

- Calculated QBI Deduction: $23,996.42 (20% of Taxable Income before QBI, lower than 20% of Net SE Earnings)

- Federal Income Tax:

Once all deductions are applied, Alex’s final taxable income is taxed at progressive rates.

- Final Federal Taxable Income: $95,985.70

- Calculated Federal Income Tax: $14,756.94

- Net Investment Income Tax (NIIT):

This 3.8% tax targets certain investment income once Modified Adjusted Gross Income (MAGI) crosses specific thresholds.

- Alex’s MAGI ($149,982.12) stays below the 2026 threshold for single filers ($200,000).

- Calculated NIIT: $0.00

- Alternative Minimum Tax (AMT):

AMT operates as a parallel tax system meant to ensure higher earners pay a minimum tax amount. In Alex’s case, the SALT cap already limits the state tax add-back, and no other major AMT preference items apply, so AMT never triggers.

- AMT Triggered: No

- AMT Liability: $0.00

Alex’s Total Tax Burden for 2026

- Total Federal Tax Liability (Income Tax + SE Tax + NIIT + AMT): $38,792.70

- Total California State Tax Liability: $9,036.30

- Overall Tax Burden: $47,829.00

Takeaway for Freelancers and Gig Workers

- The 15.3% Self-Employment Tax carries real weight: It’s often the single largest tax component freelancers face, covering Social Security and Medicare. Half of it remains deductible, trimming your AGI.

- Strategic deductions matter: Maxing out pre-tax contributions like a SEP IRA and deducting self-employed health insurance premiums lowers AGI substantially, which then reduces both federal and state taxable income.

- The QBI deduction delivers major value: Section 199A can meaningfully cut your federal income tax liability, especially when taxable income stays below the phase-out thresholds.

- The SALT cap leaves a mark: The $10,000 cap on State and Local Tax deductions means high-tax state residents like Alex can’t fully deduct state income and property taxes, which inflates federal taxable income.

- State taxes add real weight: Don’t overlook state income tax obligations, particularly in high-tax states like California, since they add a substantial layer to your overall burden.

- Planning ahead pays off: Estimating income and expenses throughout the year lets you make accurate quarterly payments and avoid surprises at filing time.

Strategic Tax Planning for Freelancers: Minimizing Your SE Tax Burden

Smart tax planning for 2026 can meaningfully shrink your self-employment tax bill. Freelancers have several legitimate levers to pull.

Maximizing Business Deductions

Every legitimate business expense lowers your net earnings, which reduces both income tax and self-employment tax. Detailed record-keeping makes all the difference here.

- Home Office Deduction: Using part of your home exclusively and regularly for business may qualify you for this deduction.

- Health Insurance Premiums: Premiums for health, dental, and qualified long-term care insurance are often deductible if you’re self-employed and lack access to an employer-sponsored plan.

- Retirement Contributions: SEP IRAs, Solo 401(k)s, and SIMPLE IRAs shrink taxable income while building your retirement savings at the same time.

- Vehicle Expenses: Deduct actual costs or use the IRS standard mileage rate for business use of your vehicle.

- Office Supplies, Software, Professional Development: These common expenses qualify as ordinary costs of doing business.

- Professional Services: Fees paid to accountants, lawyers, and other professionals for business purposes are deductible.

The Qualified Business Income (QBI) Deduction Under Section 199A

Eligible self-employed individuals can deduct up to 20% of qualified business income through the QBI deduction, a major benefit for many freelancers. The One Big Beautiful Bill Act (OBBBA) made this deduction permanent.

- Below the Lower Threshold: You claim the full 20% deduction, capped at 20% of taxable income before the QBI deduction.

- Between Lower and Upper Thresholds (Phase-Out): The deduction becomes limited based on W-2 wages paid by the business and the unadjusted basis of qualified property.

- Above the Upper Threshold: W-2 wages and the unadjusted basis of qualified property fully limit the deduction.

Estimated 2026 Taxable Income Thresholds (before QBI deduction):

- Single/Head of Household:

- Lower Threshold: ~$201,200

- Upper Threshold: ~$252,700

- Married Filing Jointly:

- Lower Threshold: ~$402,300

- Upper Threshold: ~$505,300

- Married Filing Separately:

- Lower Threshold: ~$201,200

- Upper Threshold: ~$252,700

Note: These 2026 thresholds are estimates based on inflation adjustments from 2025 figures and remain subject to official IRS release.

Estimated Tax Payments: Avoiding Penalties

No employer withholds taxes from self-employment income, which means quarterly estimated payments fall entirely on you. Missing them triggers underpayment penalties.

2026 Federal Estimated Tax Payment Deadlines:

- April 15, 2026 (for January 1 to March 31 income)

- June 15, 2026 (for April 1 to May 31 income)

- September 15, 2026 (for June 1 to August 31 income)

- January 15, 2027 (for September 1 to December 31 income)

Form 1040-ES handles the calculation and payment process. Missing these deadlines results in penalties, so mark them on your calendar now.

Separating Business and Personal Finances

Separate bank accounts for business and personal finances make record-keeping dramatically simpler. Tracking income and expenses becomes far easier, and you’ll thank yourself if an audit ever comes knocking.

Beyond the Basics: Advanced Considerations for Freelancers

Worker Classification in the Gig Economy

Whether you’re classified as an employee or an independent contractor carries major tax consequences. Independent contractors pay self-employment tax directly, while employers handle payroll taxes for employees. Misclassification can expose companies to severe penalties.

Gig workers labeled as independent contractors bear responsibility for self-employment tax, whereas employers typically cover payroll taxes for their employees. This debate continues to play out, particularly amid ongoing disputes involving major gig economy platforms.

Limited Partner Exception to Self-Employment Tax

Recent court rulings have reshaped how certain partners get treated for self-employment tax purposes. The Fifth Circuit Court of Appeals, in Sirius Solutions LLLP v. Commissioner, ruled that a “limited partner” means someone with limited liability under state law, regardless of how actively involved they are in the business.

This ruling contradicts earlier Tax Court decisions, creating a split between circuits. The issue may eventually land before the Supreme Court.

Impact of the One Big Beautiful Bill Act (OBBBA)

The One Big Beautiful Bill Act introduced several notable changes, chief among them making the QBI deduction permanent. Freelancers relying on this deduction now have long-term certainty around it. The act also included temporary changes to the State and Local Tax (SALT) cap for some taxpayers.

Essential Resources and Professional Guidance

Staying current on the rules and knowing when to call in expert help both matter for solid tax planning for 2026.

IRS Publications and Forms

The IRS offers several resources that help freelancers understand their obligations:

- IRS Publication 334, “Tax Guide for Small Business”: A comprehensive guide for sole proprietors.

- IRS Publication 505, “Tax Withholding and Estimated Tax”: Explains how to calculate and pay estimated taxes.

- Schedule SE (Form 1040): Used to calculate your self-employment tax.

- Form 1040-ES, “Estimated Tax for Individuals”: Helps you make quarterly payments.

You’ll find these and other helpful documents on the IRS website.

When to Seek Professional Advice

Complex situations call for professional advice, even with a solid guide in hand. High income, unusual business structures, or complicated deductions all justify a call to a tax professional. A qualified expert brings personalized guidance and helps you stay compliant with confidence.

Final Thoughts

The 15.3% self-employment tax forms a central part of life as a freelancer or gig worker. Understanding its components, maximizing smart deductions, and making timely estimated payments protect your financial health year after year.

Proactive tax planning for 2026 buys you peace of mind and lets you keep more of what you earn. Educate yourself on these rules, then consult a tax professional for guidance tailored to your specific situation.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.