Are you still waiting on an IRS decision for your Employee Retention Credit claim? A hidden deadline is already running against you — and it does not stop for appeals, paperwork, or any step of the administrative process.

Miss this deadline, and your right to recover that money disappears permanently. This is the ERC Two-Year Trap, and every small business owner with a pending or disputed ERC claim needs to understand it before it is too late in 2026.

⚡ Executive Summary: The ERC Two-Year Trap Explained

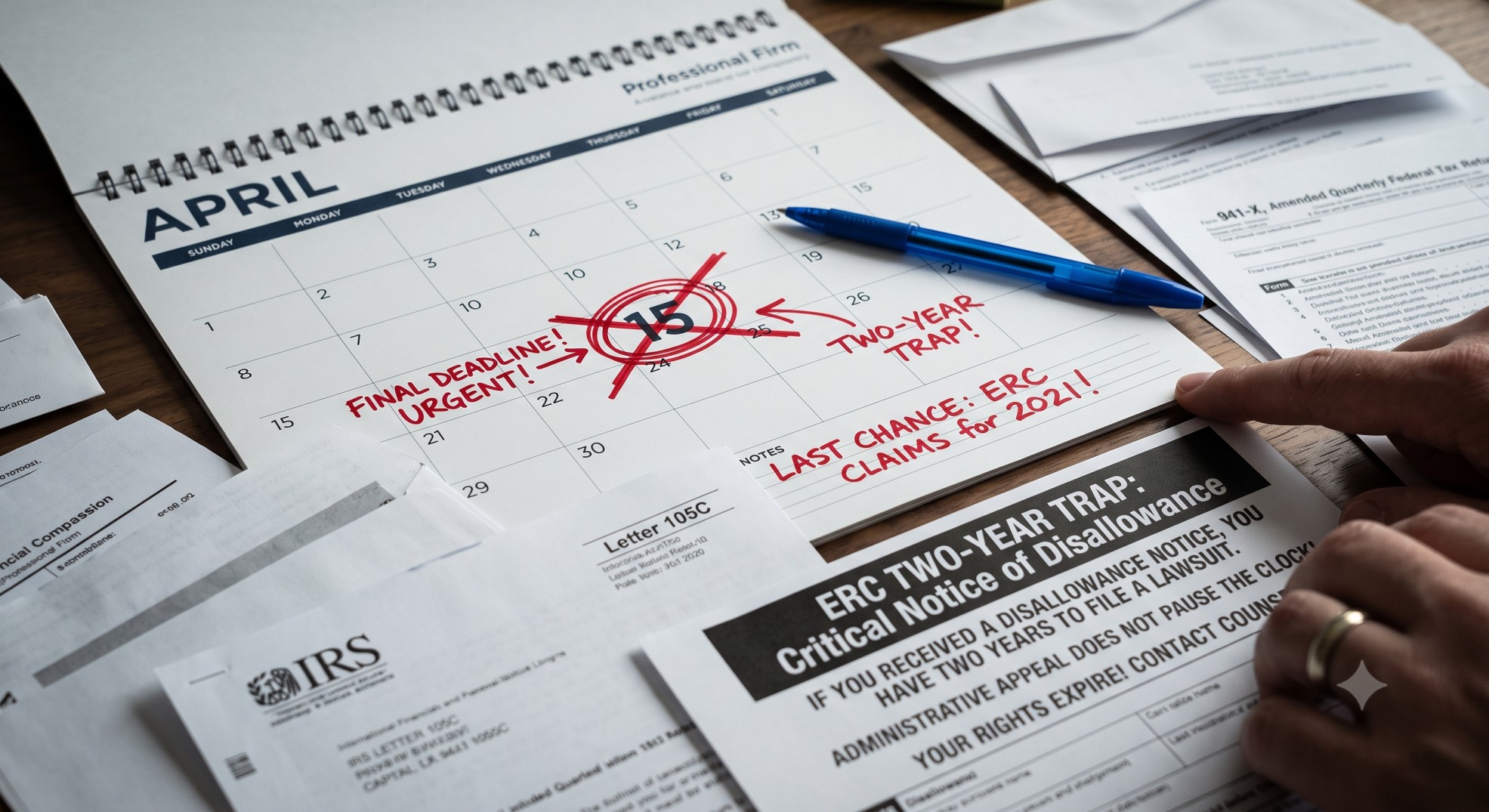

- The IRS appeals process for your ERC claim does not pause the two-year clock for filing a federal refund lawsuit.

- Under IRC Section 6532(a)(1), the two-year deadline to sue starts the day the IRS mails you a formal disallowance notice.

- Missing this deadline permanently eliminates your right to recover the refund — regardless of whether your original claim was completely valid.

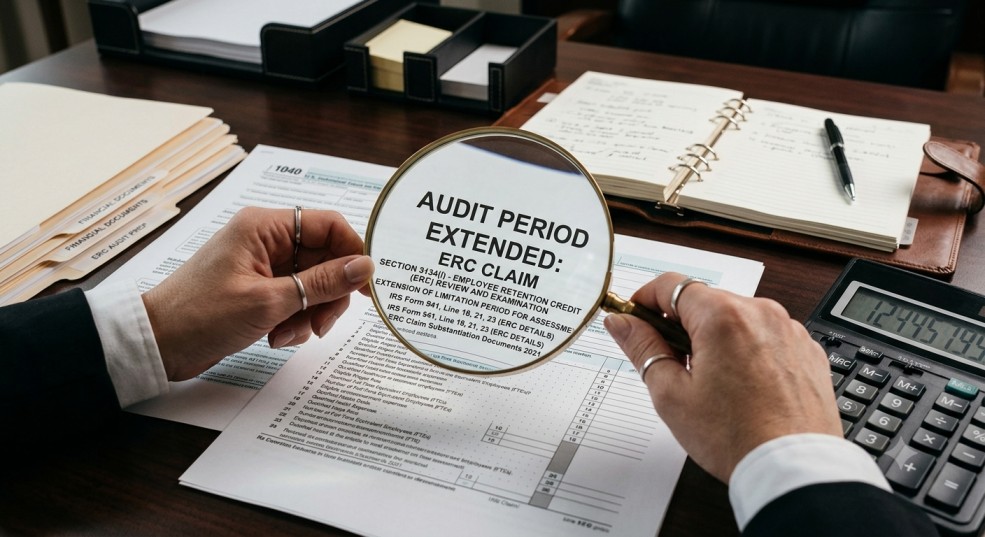

- The One Big Beautiful Bill Act (OBBBA), signed in July 2025, extended the IRS audit window for all ERC-related claims to six years.

- Form 907 can extend your right to sue, but you must request it before your window closes — the IRS introduced a streamlined Form 907 process in April 2026.

- A California S-Corp case study in this article shows how passive waiting cost one business owner $68,591.53 in permanently lost tax savings.

Table of Contents

- The ERC and Why It Still Matters in 2026

- The Two-Year Trap: A Deadline You Cannot Afford to Miss

- Real-World Impact: How the ERC Two-Year Trap Cost Sarah $68,591

- Other Critical ERC Deadlines and Risks in 2026

- How to Protect Your Business From the ERC Two-Year Trap

- What Tax Experts Are Saying in 2026

- Don’t Let Your ERC Refund Disappear

The ERC and Why It Still Matters in 2026

What Was the Employee Retention Credit?

The Employee Retention Credit (ERC) helped businesses keep employees on payroll during the COVID-19 pandemic. Congress created it through the Coronavirus Aid, Relief, and Economic Security (CARES) Act in March 2020 and later expanded it under the American Rescue Plan Act of 2021 (ARP).

Eligible businesses could claim a refundable tax credit for qualified wages paid. IRC Section 3134 governed wages paid in late 2021, while IRC Section 2301 of the CARES Act covered earlier periods.

Why ERC Claims Face Heavy Scrutiny Right Now

Widespread fraud and aggressive third-party promoters drove many businesses into filing questionable ERC claims, drawing sustained IRS attention that has only intensified since.

The “One Big Beautiful Bill Act” (OBBBA), signed in July 2025, extended the IRS assessment period to six years for all ERC-related claims. That window starts from the later of the original return filing date or the credit claim submission date — meaning the IRS can audit claims filed in 2024 or earlier well into 2029.

Audits and disallowances are not behind you. They are very much ahead of you in 2026.

The Two-Year Trap: A Deadline You Cannot Afford to Miss

The Statute of Limitations for ERC Refund Lawsuits

If the IRS disallows your ERC claim, you generally have two years to sue the government in federal court. IRC Section 6532(a)(1) establishes this rule — and the clock starts the day the IRS mails you a formal IRS disallowance notice.

Here is the part that catches business owners off guard: engaging in the IRS administrative appeals process does not pause that clock. Those two years keep running whether you are actively appealing or not.

Many business owners assume that fighting a disallowance buys them more time to sue. It does not. That assumption is the trap itself.

How Missing This Deadline Permanently Destroys Your Refund

Miss the two-year window, and you forfeit your right to file an ERC refund lawsuit — permanently.

Your claim’s merit becomes irrelevant at that point. A perfectly legitimate credit worth tens of thousands of dollars becomes unrecoverable. That outcome — a valid refund lost not because the claim was wrong, but because a deadline expired — is exactly what the ERC Two-Year Trap produces.

Real-World Impact: How the ERC Two-Year Trap Cost Sarah $68,591

Case Study: How Sarah Lost $68,591 by Waiting on IRS Appeals

The Scenario: Sarah owns a consulting S-Corporation in California. In 2021, her business claimed $150,000 in Employee Retention Credit.

Under IRS rules, businesses must reduce their deductible wage expenses by the amount of any ERC claimed. Sarah’s S-Corp therefore did not deduct those $150,000 in wages on its 2021 Form 1120-S, and that reduction flowed directly through to her personal 2021 Form 1040.

What Went Wrong: By 2026, after a lengthy appeals process, the IRS disallowed the entire $150,000 ERC. The statute of limitations for amending Sarah’s 2021 personal income tax return (Form 1040) expired on April 15, 2025. She could no longer file an amended return to claim the deduction for those $150,000 in wages.

Her 2021 taxable income remained higher than it should have been — and the resulting tax overpayments became permanently unrecoverable.

Scenario Details (2021 Tax Year, Single Filer in California):

- S-Corp Net Income (before ERC wage adjustment): $300,000.00

- Owner’s W-2 Salary from S-Corp: $100,000.00

- Other Investment Income: $50,000.00

- ERC Wages Disallowed: $150,000.00

Original 2021 Tax Liability (ERC wages NOT deducted, as filed):

- Adjusted Gross Income (AGI): $450,000.00

- Federal Taxable Income: $437,450.00

- Federal Income Tax: $127,650.50

- California State Income Tax: $40,581.96

- FICA Tax (on W-2 wages): $7,650.00

- Net Investment Income Tax (NIIT): $1,900.00

- Total Original Tax Liability: $177,782.46

Hypothetical 2021 Tax Liability (if ERC wages had been deducted):

- Adjusted S-Corp K-1 Income: $150,000.00

- Adjusted Gross Income (AGI): $300,000.00

- Federal Taxable Income: $287,450.00

- Federal Income Tax: $75,150.50

- California State Income Tax: $24,490.42

- FICA Tax (on W-2 wages): $7,650.00

- Net Investment Income Tax (NIIT): $1,900.00

- Total Hypothetical Tax Liability: $109,190.92

Total Lost Tax Savings (Gone Permanently):

- Lost Federal Income Tax Savings: $52,500.00

- Lost California State Income Tax Savings: $16,091.53

- Lost Net Investment Income Tax (NIIT) Savings: $0.00

- Total Lost Tax Savings (Refund Forever Gone): $68,591.53

The Lesson: Sarah’s situation is not a hypothetical edge case — this pattern is playing out for small business owners across the country right now. Waiting on the IRS appeals process to conclude caused her to miss the amendment window for her 2021 return. That single oversight cost her more than $68,000 in recoverable tax savings she can never get back. Knowing your deadlines and acting before they expire is the only defense that actually works.

Other Critical ERC Deadlines and Risks in 2026

The Extended IRS Audit Window You Need to Know About

The IRS has significantly more time to audit ERC claims than it does for standard tax returns. The OBBBA, enacted in July 2025, extended the audit period to six years, starting from the later of the original return filing date or the credit claim submission date.

For businesses that filed ERC claims in 2024 or earlier, the IRS can examine those returns well into 2029. Meticulous recordkeeping is not a suggestion — it is your primary line of defense.

The Government’s Right to Claw Back Erroneous Refunds

Receiving an ERC refund does not mean the IRS has permanently accepted your claim. Under IRC Section 7405(b), the government can sue to recover an erroneous refund within two years — a window that extends to five years if fraud or misrepresentation was involved.

Even a processed and deposited refund can become a liability if the underlying claim is later found to be improper.

A New IRS Option for Wage Deduction Coordination

New IRS guidance from March 2025 offers a practical path for some businesses caught in the wage deduction mismatch. If you received an ERC refund but did not reduce your wage deduction in the original filing year, you may include the overstated deduction as income in the year you received the refund — without needing to amend prior tax returns.

This option simplifies compliance considerably for businesses in exactly that position.

How to Protect Your Business From the ERC Two-Year Trap

Start With a Fresh Review of Your ERC Eligibility

A second opinion from a qualified tax professional can surface gaps or errors in your original ERC claim before the IRS does. Review your eligibility under both the government-ordered suspension test and the gross receipts test to confirm your claim genuinely meets all applicable IRS criteria.

Build an Airtight Documentation File

Strong documentation is your single best defense against an ERC audit. Maintain complete payroll records, applicable government orders, and financial statements that directly support your claim’s basis.

Thorough records also strengthen your position considerably if you ever need to pursue an ERC refund lawsuit in federal court.

Understand the IRS Voluntary Correction Programs

The IRS launched a second Voluntary Disclosure Program in August 2024, giving employers a structured path to correct mistakes on previously filed ERC claims. If your claim’s eligibility is in question, voluntary withdrawal or correction can help you avoid penalties and interest charges before the IRS initiates its own review.

Engage Tax Legal Counsel the Moment You Receive a Disallowance Notice

Experienced tax attorneys become essential the moment you receive an IRS disallowance notice. Your two-year deadline for filing an ERC refund lawsuit is absolute — no exceptions, no default extensions.

Qualified counsel can manage your appeals while simultaneously protecting your right to sue in federal court. Waiting until the appeals process concludes on its own is exactly how businesses fall into the ERC Two-Year Trap.

Use Form 907 to Buy Yourself More Time

Form 907 — “Agreement to Extend the Time to Bring Suit” — is a direct mechanism for preserving your rights beyond the two-year window. Requesting the IRS to sign this form extends your filing deadline before it expires.

The IRS introduced a streamlined process for Form 907 in April 2026, specifically designed for taxpayers with six months or less remaining on their two-year window. Acting on it early is one of the simplest protective steps available to you.

What Tax Experts Are Saying in 2026

Tax Professionals Are Flagging High Audit Risk Across the Board

Tax professionals are consistent in their assessment: ERC claims carry elevated audit risk in 2026. The IRS is actively enforcing compliance with substantial penalties for improper claims, and that enforcement posture shows no signs of softening.

Why Passive Waiting Is the Most Dangerous Strategy

Leading tax law firms are issuing direct warnings about the ERC Two-Year Trap. Sitting back while the IRS appeals process runs its course is a high-stakes gamble — one that routinely results in the permanent, unrecoverable loss of a legitimate refund.

When Filing an ERC Refund Lawsuit Is the Right Move

Litigation is not always a last resort — sometimes it is the most effective tool available. Under IRC Section 7422, if the IRS takes no action on a refund claim for six months, you have the right to sue directly in federal court.

An ERC refund lawsuit can preserve your legal rights and compel IRS action when administrative remedies have stalled. The cost of litigation is real — but the cost of permanently losing a six-figure refund by doing nothing is almost always far greater.

Don’t Let Your ERC Refund Disappear

Many businesses owe their survival to the ERC — the credit provided critical financial runway during one of the most economically disruptive periods in recent history. Getting the refund you legitimately earned, and protecting your right to keep it, demands just as much attention in 2026 as it did when you first filed.

The ERC Two-Year Trap is real, it is running right now, and it will not wait for your appeals to finish. Consult a qualified tax professional or attorney today, document everything, and act before a deadline you cannot see eliminates a refund you have already earned.

Disclaimer: This content provides general information for educational purposes only. Tax laws are complex and change often. It is not professional tax, legal, or financial advice. Always consult a qualified tax professional for personalized guidance regarding your specific situation. Ourtaxpartner.com is not responsible for any actions taken based on the information provided herein.