The IRS isn’t just knocking; it’s using AI. For corporate and enterprise taxpayers, 2026 brings a new era of targeted enforcement. Are you prepared for the mandatory IRS audit thresholds and regulatory shifts that could change your tax liability and compliance strategy? This article examines the new environment of 2026 tax enforcement, offering a clear guide for proactive corporate tax compliance.

Executive Summary

- The IRS significantly increases audit rates for large corporations, complex partnerships, and high-wealth individuals in 2026.

- Advanced data analytics and AI drive highly targeted audits, moving away from random selections.

- Key legislative changes from the One Big Beautiful Bill Act (OBBBA) affect QBI, bonus depreciation, Section 179 expensing, and international tax rules.

- New digital asset reporting (Form 1099-DA) and ongoing Corporate Transparency Act (CTA) requirements demand attention.

- Proactive measures like meticulous documentation, strong internal controls, and professional guidance are essential for effective corporate tax compliance.

- The Compliance Assurance Process (CAP) program offers real-time issue resolution for eligible large corporations.

Introduction: Understanding the New Era of Corporate Tax Enforcement in 2026

Why 2026 is Different: Increased Scrutiny and Advanced Analytics

The 2026 tax year marks a major change in IRS enforcement. Enhanced funding and a strategic operating plan cause this shift. The IRS now uses advanced data analytics and artificial intelligence to identify non-compliance (IRS). This technology helps the agency find discrepancies and match third-party data. Consequently, the IRS shifts from random audits to highly targeted enforcement actions. This new approach shapes the environment of 2026 tax enforcement.

The Stakes for Corporate and Enterprise Taxpayers

Corporate and enterprise taxpayers face significant financial and reputational risks from non-compliance. Heightened scrutiny demands proactive planning. Understanding these changes is no longer optional. It is an essential step for strategic planning and risk mitigation. Therefore, protecting your business against potential audits becomes paramount for strong corporate tax compliance.

Understanding Mandatory IRS Audit Thresholds for 2026

IRS’s Renewed Focus: Large Corporations, Partnerships, and High-Wealth Individuals

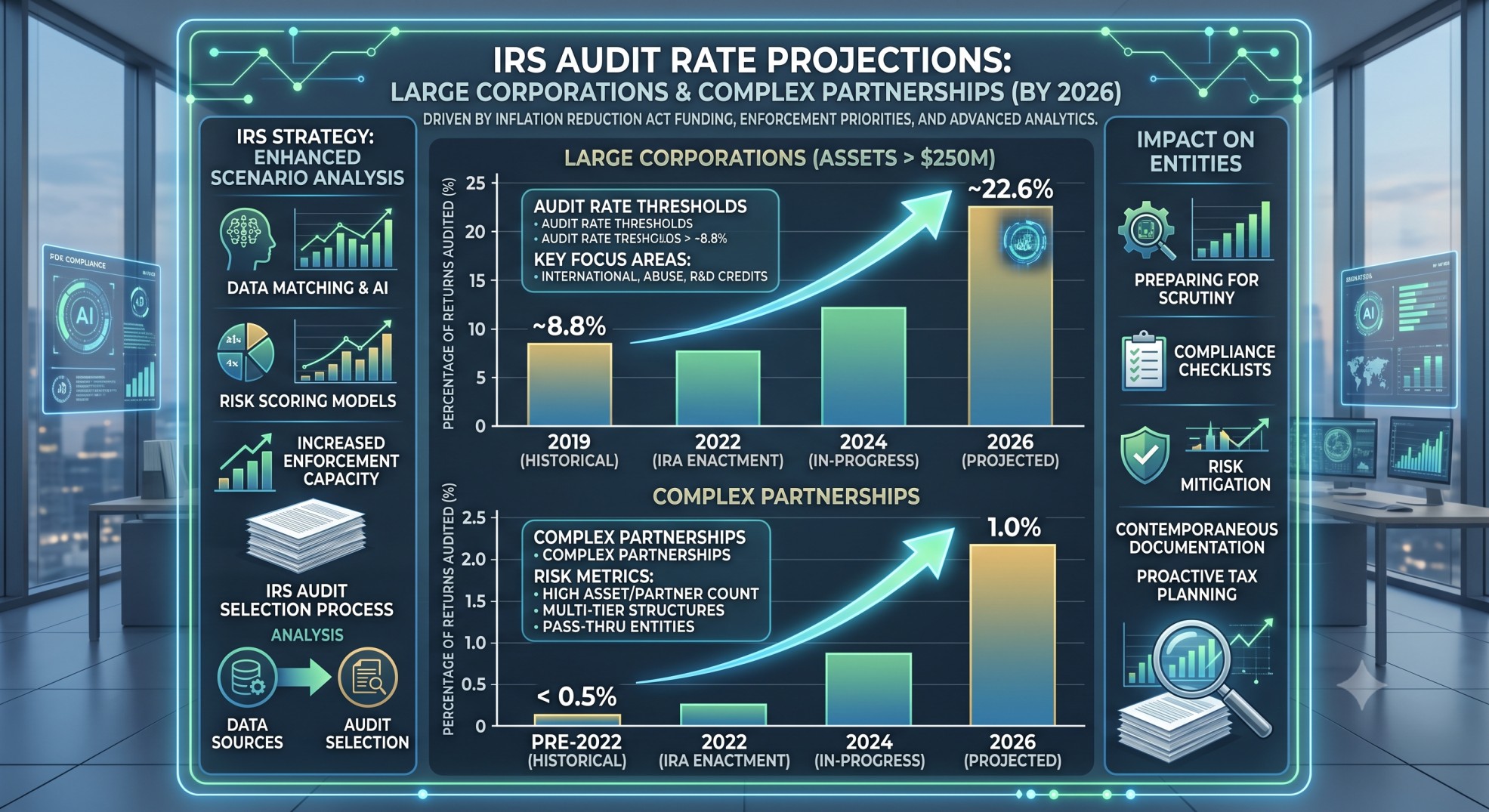

The IRS explicitly targets specific taxpayer segments for increased audits in 2026. Audit rates for large corporations (assets over $250 million) are projected to reach 22.6%. This represents a nearly threefold increase from 2019 levels. Furthermore, large, complex partnerships (assets over $10 million) will see audit rates climb to 1%, a tenfold increase. Wealthy individuals with total positive income over $10 million face projected audit rates of 16.5%. The IRS maintains its commitment to not increasing audit rates for lower-income taxpayers.

Specific Audit Triggers for Corporate Entities

Certain factors can trigger an IRS audit for corporate entities. High gross receipts, for example, exceeding $10 million or $250 million, often draw attention. International transactions and foreign-sourced income also increase scrutiny. Complex deductions, such as Research & Development (R&D) expenses or transfer pricing, are frequent targets. Significant fluctuations in a company’s Effective Tax Rate (ETR) can also flag a business for review. These elements are key considerations for managing IRS audit thresholds.

The Role of Data Analytics and AI in IRS Targeting

The IRS uses technology to identify discrepancies. It uses AI to match taxpayer data with third-party information. This includes W-2s, 1099s, bank records, and digital asset exchanges. This technological shift allows for highly targeted enforcement. It moves the IRS away from random audits. Consequently, the agency can focus resources on areas with the highest potential for non-compliance. This strategy is key to the new era of 2026 tax enforcement.

Key Regulatory Shifts Affecting Corporate Tax in 2026

Legislative Impacts: The One Big Beautiful Bill Act (OBBBA) of 2025

The One Big Beautiful Bill Act (OBBBA) of 2025 introduces several permanent and expanded tax provisions for 2026. This legislation significantly affects corporate tax planning. It provides stability for businesses. For instance, the Qualified Business Income (QBI) Deduction (IRC Section 199A) becomes permanent and expanded for pass-through entities. This ensures its availability beyond previous sunset dates. Furthermore, the OBBBA permanently restores 100% bonus depreciation (IRC Section 168(k)) for qualified assets. It also increases Section 179 expensing limits, with annual inflation adjustments. Foreign-Derived Intangible Income (FDII) and Global Intangible Low-Taxed Income (GILTI) regimes are rebranded to FDDEI and NCTI, respectively (IRC Sections 250, 951A). The Act modifies their deduction percentages, affecting effective tax rates on these income streams.

Digital Asset Reporting (Form 1099-DA) and Increased Visibility

For transactions on or after January 1, 2025, brokers, including cryptocurrency exchanges, must issue Form 1099-DA. This requirement significantly increases the IRS’s visibility into digital asset transactions. Corporate holdings and transactions involving digital assets will face greater scrutiny. Therefore, companies must ensure accurate reporting for their digital asset activities. This new reporting requirement is an important part of 2026 tax enforcement.

Corporate Transparency Act (CTA) and Beneficial Ownership Information (BOI)

The Financial Crimes Enforcement Network (FinCEN) still enforces the Corporate Transparency Act (CTA). This act requires beneficial ownership information (BOI) reporting. It particularly affects LLCs and entities with foreign investors. Companies must comply with these ongoing requirements. Failure to do so can result in significant penalties. More information is available on the FinCEN website.

Continued Scrutiny on Employee Retention Credit (ERC) Claims

The IRS maintains strict auditing and denial of improper or aggressive Employee Retention Credit (ERC) claims. This remains a key enforcement priority for 2026. Businesses must have strong evidence for any ERC claims. Lack of proper documentation can lead to significant disputes and potential litigation.

Key Inflation-Adjusted Figures for 2026

Several key figures are inflation-adjusted for 2026. The Standard Deduction is $32,200 for married couples filing jointly. It is $16,100 for single filers and married individuals filing separately. Heads of households can claim $24,150. The Section 179 expensing limit increases to $2,560,000. The Alternative Minimum Tax (AMT) exemption for unmarried individuals is $90,100. For married couples filing jointly, it is $140,200. The Estate Tax Basic Exclusion Amount reaches $15,000,000. The Employer-Provided Childcare Tax Credit increases to $500,000, or $600,000 for eligible small businesses.

Real-World Impact: InnovateCorp Inc. Case Study (2026)

The Challenge: R&D Amortization vs. Immediate Expensing

InnovateCorp Inc., a leading technology firm, faces the complex environment of 2026 tax regulations. As a large enterprise with significant revenue and international operations, understanding how potential regulatory shifts affect its tax liability and audit risk is essential. This case study shows how a seemingly minor change in tax law can dramatically alter a corporation’s financial outlook and increase its audit profile.

InnovateCorp Inc. Profile and Assumptions

InnovateCorp Inc. is a C-corporation based in California. Its projected financials for 2026 are:

- Gross Revenue: $500,000,000

- Operating Expenses (excluding R&D): $250,000,000

- Total R&D Expenses Incurred: $30,000,000

- Depreciation: $20,000,000

- Interest Expense: $5,000,000

- Foreign-Sourced Income (taxable in US): $10,000,000

Assumed Tax Rates for 2026:

- Federal Corporate Tax Rate: 21%

- California Corporate Tax Rate: 8.84%

Scenario A: Baseline (Favorable R&D Treatment)

In this scenario, InnovateCorp fully deducts its $30,000,000 in R&D expenses in the year incurred.

- R&D Deduction: $30,000,000

- California Taxable Income: $185,000,000

- California State Tax: $16,394,000

- Federal Taxable Income: $168,606,000

- Federal Tax: $35,407,260

- Total Tax Liability: $51,801,260

- Effective Tax Rate (ETR): 25.90%

Scenario B: Regulatory Shift (Less Favorable R&D Treatment)

This scenario reflects a regulatory shift where R&D expenses must be amortized over five years. Only one-fifth of the total R&D expenses ($6,000,000) is deductible in 2026.

- R&D Deduction: $6,000,000

- California Taxable Income: $209,000,000

- California State Tax: $18,479,600

- Federal Taxable Income: $190,520,400

- Federal Tax: $40,009,284

- Total Tax Liability: $58,488,884

- Effective Tax Rate (ETR): 29.24%

Impact Analysis & Audit Implications for InnovateCorp

The regulatory shift in R&D deductibility significantly affects InnovateCorp’s tax burden. The amortization requirement leads to an additional $6,687,624 in total tax liability for 2026. InnovateCorp’s ETR increases by 3.34 percentage points, from 25.90% to 29.24%.

InnovateCorp Inc. is already a prime candidate for IRS and state tax audits due to several factors:

- High Gross Receipts: $500 million in revenue significantly exceeds typical IRS audit thresholds for large corporate audits.

- International Transactions: Foreign-sourced income adds complexity and increases scrutiny.

- Complex Deductions: R&D expenses, even when fully deductible, are often targets for audit.

- Regulatory Shifts and ETR Fluctuations: A sudden increase in ETR, especially driven by a major expense change, can flag a company for review.

The shift to R&D amortization not only increases InnovateCorp’s tax bill. It also alters its financial ratios, potentially drawing more attention from tax authorities. This highlights the importance of understanding IRS audit thresholds.

Non-Applicable Taxes for C-Corporations

For a C-corporation like InnovateCorp Inc., certain taxes and deductions are generally not applicable:

- Alternative Minimum Tax (AMT): The corporate AMT was largely repealed by the TCJA. While the Inflation Reduction Act (IRA) introduced a Corporate Alternative Minimum Tax (CAMT), it typically applies only to corporations with average annual adjusted financial statement income exceeding $1 billion. InnovateCorp’s financials do not trigger the CAMT.

- Net Investment Income Tax (NIIT): This 3.8% tax applies to individuals, estates, and trusts, not directly to C-corporations.

- Section 199A (Qualified Business Income – QBI) Deduction: This deduction is for pass-through entities, not for income earned by C-corporations.

Proactive Strategies for Corporate Tax Compliance and Risk Mitigation

Meticulous Documentation and Record-Keeping

Strong, detailed, and organized record-keeping is the best defense against an audit. Companies must provide evidence for all income, deductions, and complex transactions. This includes maintaining clear records for R&D expenses, international dealings, and any significant tax positions. Therefore, meticulous documentation is crucial for effective corporate tax compliance.

Internal Controls and Regular Tax Health Checks

Implementing strong internal processes is vital. Regular tax health checks help identify potential compliance gaps before they become issues. These periodic reviews ensure adherence to evolving tax laws. They also help maintain accurate financial reporting. Consequently, strong internal controls mitigate audit risk.

Engaging with the Compliance Assurance Process (CAP) Program

The IRS offers the Compliance Assurance Process (CAP) program for large corporate taxpayers. Companies with assets of $10 million or more can apply. The application period for the 2026 CAP program ran from September 3 to October 31, 2025. This program allows for real-time issue resolution before tax return filing. It provides certainty and reduces post-filing audit risk. Therefore, eligible corporations should consider this proactive approach to 2026 tax enforcement.

Strategic Tax Planning and Professional Guidance

Continuous analysis and adaptation are necessary in the changing tax environment. Companies must engage in strategic tax planning. This involves not just minimizing tax but also managing audit risk. Consulting qualified tax professionals, such as CPAs or tax attorneys, is highly recommended. They can provide tailored advice and help navigate complex regulations. This professional guidance ensures strong corporate tax compliance.

Conclusion: Preparing for a More Scrutinized Tax Landscape

Key Takeaways for Corporate Tax Leaders

The 2026 tax year demands vigilance from corporate tax leaders. Staying informed about regulatory shifts is paramount. Understanding specific IRS audit thresholds and risk factors is equally important. Effective tax rate management and strategic, proactive tax planning are essential. Companies must adapt to this new era of 2026 tax enforcement.

The Need for Vigilance and Adaptation

The IRS’s increased enforcement and technological advancements mark a new era. Corporate entities must focus on proactive compliance. Vigilance and adaptation are no longer options; they are essential actions. Preparing now will protect your business against heightened scrutiny and potential liabilities.

Disclaimer

This document is intended for informational and research purposes only and does not constitute tax, legal, or financial advice. Tax laws and regulations are complex and subject to change. The information presented is based on current understanding and available public data as of July 2, 2026. Corporate entities and individuals should consult with qualified tax professionals, such as CPAs or tax attorneys, for advice tailored to their specific situations.

Frequently Asked Questions

What is new about IRS tax enforcement in 2026?

The 2026 tax year introduces a new era of targeted enforcement by the IRS, driven by increased funding and the strategic use of advanced data analytics and AI. This shifts the IRS from random audits to highly focused actions, particularly for large corporations, complex partnerships, and high-wealth individuals.

What are the key IRS audit thresholds for 2026?

In 2026, audit rates are projected to significantly increase for large corporations (assets over $250 million, up to 22.6%), large, complex partnerships (assets over $10 million, up to 1%), and wealthy individuals (income over $10 million, up to 16.5%). High gross receipts, international transactions, complex deductions, and significant ETR fluctuations can also trigger audits.

How does the One Big Beautiful Bill Act (OBBBA) of 2025 affect corporate tax?

The OBBBA of 2025 makes the Qualified Business Income (QBI) Deduction permanent and expanded, permanently restores 100% bonus depreciation, and increases Section 179 expensing limits. It also rebrands and modifies FDII and GILTI regimes, impacting effective tax rates on international income streams.

What are the new digital asset reporting requirements?

Starting January 1, 2025, brokers, including cryptocurrency exchanges, must issue Form 1099-DA for digital asset transactions. This significantly increases the IRS’s visibility into corporate and individual digital asset activities, requiring accurate reporting.

What proactive strategies can corporations use for tax compliance?

Key strategies include meticulous documentation and record-keeping, implementing strong internal controls and regular tax health checks, engaging with the Compliance Assurance Process (CAP) program for eligible large corporations, and seeking strategic tax planning and professional guidance from CPAs or tax attorneys.