Date: 2/10/2026

The 2025 “Split Year”: Navigating the Jan 19 Cutoff (OBBBA)

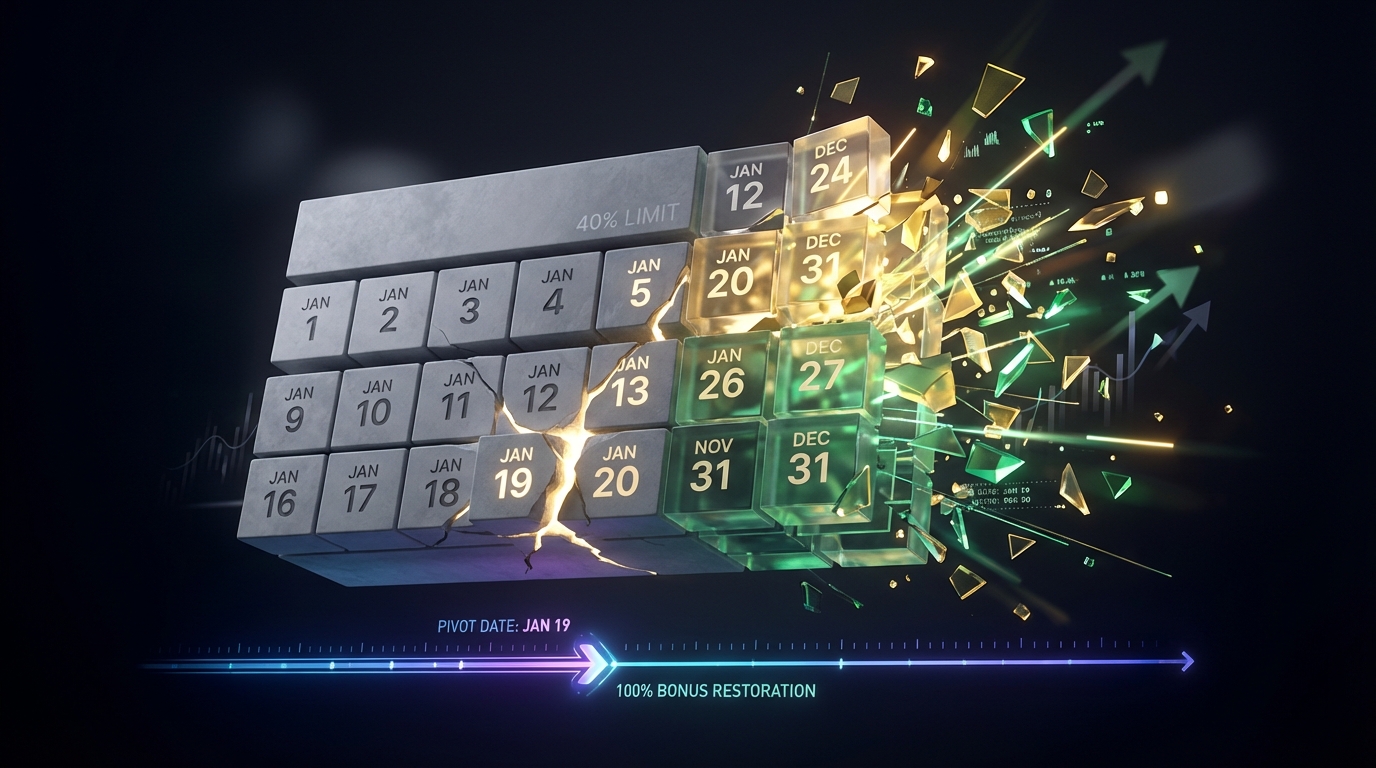

The 2025 tax year introduced a unique challenge for business owners: the “Split Year.” Under the One Big Beautiful Bill Act (OBBBA), your tax savings depend heavily on whether you bought equipment before or after January 19. This “Pivot Date” determines if you get a massive tax break immediately or if you have to spread those deductions out over several years.

If you purchased assets early in the year, you might face different Section 179 deduction limits for business equipment 2025 compared to those who waited just a few weeks. The OBBBA restored 100% bonus depreciation, but only for property acquired and placed in service after January 19, 2025. Anything bought between New Year’s Day and the pivot date is generally stuck at a 40% rate. This creates a two-tiered system that requires careful record-keeping on your 2025 Form 4562.

Bonus Depreciation: The Jan 19 Divide

| Acquisition Date | Placed in Service Date | Bonus Rate |

|---|---|---|

| Before Jan 20, 2025 | Anytime in 2025 | 40% |

| After Jan 19, 2025 | After Jan 19, 2025 | 100% |

To avoid the “Split-Year Trap,” many savvy business owners are reviewing the Section 179 vehicle deduction list for heavy trucks 2025. Since Section 179 allows for a maximum deduction of $2,500,000, you can use it to fully expense equipment bought in early January. This effectively bypasses the 40% bonus limit for those specific items. However, once you hit the $4,000,000 phase-out threshold, your ability to use this “buffer” disappears, and the timing of your purchase becomes the only factor that matters.

For those managing larger portfolios, understanding how to calculate MACRS depreciation for commercial real estate becomes vital during a split year. You might even consider a cost segregation study for commercial property depreciation to identify shorter-lived assets that qualify for the 100% rate. If your income is lower this year, the OBBBA allows you to “elect down” to a 40% rate for all assets in a specific class. This prevents wasting deductions when you do not have enough profit to offset them.

Navigating these rules requires precision. Many taxpayers seek professional CPA services for Form 4562 depreciation schedules to ensure they do not misreport assets on Line 14. This is especially true for bonus depreciation rules for heavy machinery 2025, where the timing of “constructive receipt” can make or break your tax strategy. Remember, if you paid for a machine via credit card on December 31, 2024, it counts as a 2024 expense, even if the equipment did not arrive until January.

Section 179 “Super-Limits”: The $2.5 Million Explosion

The passage of the One Big Beautiful Bill Act (OBBBA) in July 2025 has significantly altered the tax landscape for small and mid-sized businesses. This legislation introduced what tax professionals are calling “Super-Limits,” effectively doubling the Section 179 deduction limits for business equipment 2025. For the first time, business owners can write off up to $2,500,000 in qualifying purchases in a single year, providing a massive incentive to upgrade machinery and technology.

The 2025 Super-Limit Benchmarks

To understand how these changes impact your bottom line, it is essential to review the new benchmarks established by Public Law 119-21. The OBBBA overrode previous inflation adjustments to expand the deduction’s reach significantly.

| Provision | 2025 “Super-Limit” | 2024 Benchmark |

|---|---|---|

| Maximum Section 179 Deduction | $2,500,000 | $1,220,000 |

| Phase-out Threshold | $4,000,000 | Not Specified |

| SUV Deduction Cap (IRC Section 179(b)(5)) | $31,300 | Not Specified |

How the Phase-Out Works

The Section 179 deduction is designed for small to medium businesses. If a company invests in too much equipment, the benefit begins to disappear. For every dollar spent over the $4,000,000 threshold, the $2,500,000 deduction limit drops by exactly one dollar.

For example, if a company buys $5,000,000 of qualifying equipment, it is $1,000,000 over the threshold. The taxpayer must subtract that $1,000,000 from the $2,500,000 maximum, leaving a total allowable deduction of $1,500,000. If you are dealing with larger investments, you may need a cost segregation study for commercial property depreciation to maximize your write-offs elsewhere.

Strategic Interaction with Bonus Depreciation

One of the most significant changes in 2025 is the restoration of 100% bonus depreciation for assets acquired and placed in service after January 19, 2025. When you combine this with the new Section 179 limits, you have a powerful toolkit. You can use Section 179 to target specific assets first, which is helpful when learning how to calculate MACRS depreciation for commercial real estate or managing the bonus depreciation rules for heavy machinery 2025.

Compliance and State Rules

While federal limits have increased, many states do not conform to these “Super-Limits.” States like California and Pennsylvania often decouple from federal rules, capping deductions at much lower amounts, sometimes as low as $25,000. Because of these discrepancies, most business owners require professional CPA services for Form 4562 depreciation schedules to ensure they maintain separate state-specific records.

Additionally, if you are looking at the Section 179 vehicle deduction list for heavy trucks 2025, remember that the $31,300 cap applies specifically to Sport Utility Vehicles rated between 6,000 and 14,000 pounds. All “listed property” must still meet the requirement of more than 50% business use to qualify for these deductions.

CRITICAL WARNING: The “Binding Contract” Trap

Timing is everything in tax law, but for the 2025 tax year, a single weekend could cost your business hundreds of thousands of dollars. The One Big Beautiful Bill Act (OBBBA) restored the 100% bonus depreciation rate, but it came with a hidden “trap” for the unwary. If you signed a binding contract to buy equipment before January 20, 2025, you are legally barred from the 100% rate, even if the gear wasn’t delivered until December.

The IRS defines “acquisition” by the date a written binding contract is executed. This means if you committed to a purchase on January 15, 2025, you are stuck with the old 40% phase-down rate. However, if you waited until January 21 to sign, you qualify for the full 100% “Super-Limit.” When looking at Section 179 deduction limits for business equipment 2025, it is vital to separate your assets by these specific dates to avoid a massive audit headache.

The $600,000 Difference

To understand why this matters to your bottom line, consider a company purchasing bonus depreciation rules for heavy machinery 2025 totaling $1,000,000. If the contract was signed on January 18, the immediate deduction is only $400,000. By simply waiting three days to sign that same contract, the deduction jumps to $1,000,000. This 60% gap represents a significant shift in immediate cash flow that can impact your ability to reinvest in the business.

| Acquisition Date | Placed in Service Date | Bonus Rate |

|---|---|---|

| On or Before Jan 19, 2025 | Any time in 2025 | 40% (Mandatory) |

| After Jan 19, 2025 | After Jan 19, 2025 | 100% (Default) |

| After Jan 19, 2025 | After Jan 19, 2025 | 40% (If Elected) |

Mitigating the Trap with “Elect Down” Provisions

If you find your assets split between these two rates, you might face complex reporting requirements. Under IRC Section 168(k)(10), you can make an irrevocable election to apply the 40% rate to all property within a specific class. This is often a smart move for those who need to manage Net Operating Losses (NOLs) or simplify state tax non-conformity. For larger investments, such as a cost segregation study for commercial property depreciation, choosing the 40% rate across the board can sometimes offer better long-term tax stability.

Reporting and Compliance

When you file, you must report these figures on Form 4562, Part II, Line 14. Auditors are specifically looking for “split-year” filings where taxpayers claimed 100% on assets acquired during the first 19 days of the year. Whether you are reviewing the Section 179 vehicle deduction list for heavy trucks 2025 or learning how to calculate MACRS depreciation for commercial real estate, precision is key. Most businesses will require professional CPA services for Form 4562 depreciation schedules to ensure their purchase orders and contracts match the dates claimed on their returns.

Strategic Moves: Electing Down & The State “Nightmare”

Under the One Big Beautiful Bill Act (OBBBA), the default for qualified property acquired and placed in service after January 19, 2025, is 100% bonus depreciation. However, you have a strategic choice: you can “elect down” to a 40% allowance instead. While it sounds counterintuitive to take a smaller deduction, this move is often a shield against future tax hikes. If your business expects to move into a higher tax bracket in 2026 or 2027, saving 60% of your asset’s basis for future years is often better for your bottom line than a 100% write-off today.

Strategic Use of the 40% Election

The 40% election is irrevocable and must be made at the asset class level, such as for all 5-year or 7-year property. This is particularly useful for preserving Net Operating Losses (NOLs). Because federal rules limit NOL carryforwards to 80% of your taxable income, taking 100% bonus depreciation can sometimes create “wasted” deductions that you cannot use immediately. By electing the lower rate, you keep those deductions for future years when they can offset more income. This strategy is essential when planning Section 179 deduction limits for business equipment 2025 and managing your overall tax liability.

Taxpayers also use Section 179 as a “convention tool” to manage the timing of their deductions. If you place more than 40% of your total equipment in service during the fourth quarter, the IRS forces you to use the Mid-Quarter Convention, which can reduce your total depreciation for the year. To avoid this, you can use Section 179 to expense those Q4 assets immediately. This keeps them off the balance sheet for the convention test, allowing you to use the more favorable Half-Year Convention for the rest of your portfolio. This is a common tactic when applying bonus depreciation rules for heavy machinery 2025.

The State Non-Conformity “Nightmare”

While federal rules have become more generous, many states have refused to play along. This “decoupling” creates a massive administrative burden. For example, while the federal Section 179 limit is $2,500,000, states like Pennsylvania and California may cap your deduction at as little as $25,000. This means you must maintain separate depreciation logs for federal, state, and book accounting purposes. If you are trying to figure out how to calculate MACRS depreciation for commercial real estate or specialized equipment, you will likely need three different schedules.

| Provision | Federal (OBBBA 2025) | State Treatment (Common) |

|---|---|---|

| Section 179 Limit | $2,500,000 | Caps as low as $25,000 |

| Bonus Depreciation | 100% (Post-Jan 19) | Often 0% (Full Add-Back) |

| SUV Sec. 179 Cap | $31,300 | Varies (Often lower) |

| Domestic R&E | Immediate Expense | 5-Year Amortization |

Compliance and Documentation

The January 19th cutoff is a potential trap for the unwary. You must have clear records proving exactly when you acquired an asset. Anything bought between January 1 and January 19 is legally capped at 40% bonus depreciation, while anything bought January 20 or later qualifies for 100%. To navigate these split-year rules and the Section 179 vehicle deduction list for heavy trucks 2025, most businesses require professional CPA services for Form 4562 depreciation schedules. For larger investments, a cost segregation study for commercial property depreciation can help identify which components qualify for these accelerated rates, ensuring you don’t leave money on the table while staying compliant with state-specific “add-back” requirements.

Filing Form 4562: Line 14, Auto Caps, and New Asset Classes

Navigating Part II, Line 14 of Form 4562 requires careful timing this year. Thanks to the One Big Beautiful Bill Act (OBBBA), 2025 introduces a “split-rate” system for bonus depreciation. If you acquired and placed equipment in service after January 19, 2025, you can claim 100% bonus depreciation. However, assets bought before January 20 are generally limited to a 40% allowance. This shift significantly impacts the Section 179 deduction limits for business equipment 2025, as you must decide which incentive offers the best tax shield for your specific situation.

You also have the flexibility to “elect down” to a 40% or 60% allowance for the first tax year ending after January 19. This is a strategic move if you want to avoid wasting Net Operating Losses (NOLs) or manage your future tax brackets. These bonus depreciation rules for heavy machinery 2025 apply to most MACRS property with a recovery period of 20 years or less. This includes off-the-shelf software and Qualified Improvement Property (QIP), provided you meet the specific acquisition dates mentioned in the IRS instructions.

Luxury Automobile Depreciation Caps

The IRS continues to limit how much you can write off for business vehicles under Section 280F. For 2025, Rev. Proc. 2025-16 sets strict depreciation caps for passenger autos, trucks, and vans. If you buy a car and use bonus depreciation, your first-year deduction is capped at $20,200. For those looking at larger options, the Section 179 vehicle deduction list for heavy trucks 2025 shows a cap of $31,300 for vehicles rated between 6,000 and 14,000 pounds. If you lease instead of buy, be aware that a “lease inclusion amount” applies if the vehicle’s value exceeds $62,000.

| 2025 Depreciation Limits (Passenger Vehicles) | Maximum Deduction Amount |

|---|---|

| 1st Year (with Bonus Depreciation) | $20,200 |

| 1st Year (without Bonus Depreciation) | $12,200 |

| 2nd Year | $19,600 |

| 3rd Year | $11,800 |

| Succeeding Years | $7,060 |

New Asset Classes and Reporting Changes

The 2025 Form 4562 features several structural updates, including a brand-new 50-year property class. You must report these specialized assets on Lines 19h or 20e. Knowing how to calculate MACRS depreciation for commercial real estate and these new classes is vital for filing an accurate return. Many property owners are currently using a cost segregation study for commercial property depreciation to identify assets that qualify for shorter recovery periods or bonus depreciation under these updated OBBBA rules.

Other notable changes include Line 23, which now separates capitalized interest costs from other capitalized expenses. There is also a mandatory checkbox on Line 24c for anyone claiming depreciation on owned or chartered aircraft. Because these rules are increasingly complex, many taxpayers seek professional CPA services for Form 4562 depreciation schedules to ensure they don’t trigger an audit. Staying compliant requires tracking every asset’s “placed in service” date with precision to avoid reporting errors in Part II.

FAQ: 2025 Depreciation & Amortization

The enactment of the One Big Beautiful Bill Act (OBBBA) has completely rewritten the playbook for business owners in 2025. If you are buying equipment or upgrading your office, these changes mean more cash stays in your pocket right now. Understanding the new Section 179 deduction limits for business equipment 2025 is the first step toward lowering your tax bill and maximizing your immediate cash flow.

How much can I deduct under Section 179 in 2025?

For the 2025 tax year, the OBBBA pushed the maximum Section 179 deduction to a massive $2,500,000. This allows you to write off the full cost of equipment, software, and even certain building improvements like HVAC or fire systems immediately. However, there is a “spending cap” of $4,000,000. If your total equipment purchases exceed this amount, your deduction starts to shrink dollar-for-dollar, making timing essential for growing companies.

What are the 2025 bonus depreciation rules?

Bonus depreciation is back at full strength, but the “split-year” rule means timing is everything. The bonus depreciation rules for heavy machinery 2025 depend on when you placed the asset in service. If you started using the equipment after January 19, 2025, you qualify for the restored 100% rate. If you placed it in service earlier in January, you are generally limited to a 40% allowance unless you use specific tax elections to manage your brackets.

What are the limits for business vehicles?

The IRS still limits how much you can write off for “luxury” cars, but heavy vehicles get a significant break. If you are looking at a Section 179 vehicle deduction list for heavy trucks 2025, remember that vehicles with a GVWR over 6,000 pounds avoid the standard luxury caps. For smaller passenger vehicles, the first-year depreciation limit is $20,200 if you take bonus depreciation, or $12,200 if you do not.

| Vehicle Type (Placed in Service 2025) | First-Year Deduction Limit |

|---|---|

| Passenger Automobile (with Bonus) | $20,200 |

| Heavy SUV (6,000–14,000 lbs) | $31,300 (Section 179) |

| Standard Mileage Rate | 70 cents per mile |

How do I handle commercial real estate?

Real estate owners have new tools to speed up their tax breaks this year. While you might wonder how to calculate MACRS depreciation for commercial real estate for the new 50-year property class, many owners prefer a faster route. A cost segregation study for commercial property depreciation can identify components of your building that qualify for 5-year or 15-year lives. This move allows you to apply bonus depreciation to those parts, significantly increasing your upfront deductions.

Do I need professional help for Form 4562?

Filing Form 4562 has become more complex due to new technical requirements, such as mandatory aircraft disclosures and bifurcated interest reporting. Many small business owners seek professional CPA services for Form 4562 depreciation schedules to avoid the “mid-quarter convention” trap. This rule triggers if you buy more than 40% of your equipment in the final three months of the year, which can drastically reduce your first-year write-offs if not planned correctly.

About the Author

ARUN KP

With over 15 years of extensive experience in the accounting and taxation industry, Arun KP specializes in cross-border India-US taxation. As an Entrepreneur and AI Content Generator, he leverages cutting-edge technology to simplify complex financial landscapes for individuals and businesses.

Entrepreneur | AI Content Generator | India-US Tax Professional | Accountant

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice.