Date: 1/15/2026

Key Takeaways: The ‘OBBBA’ Tax Revolution

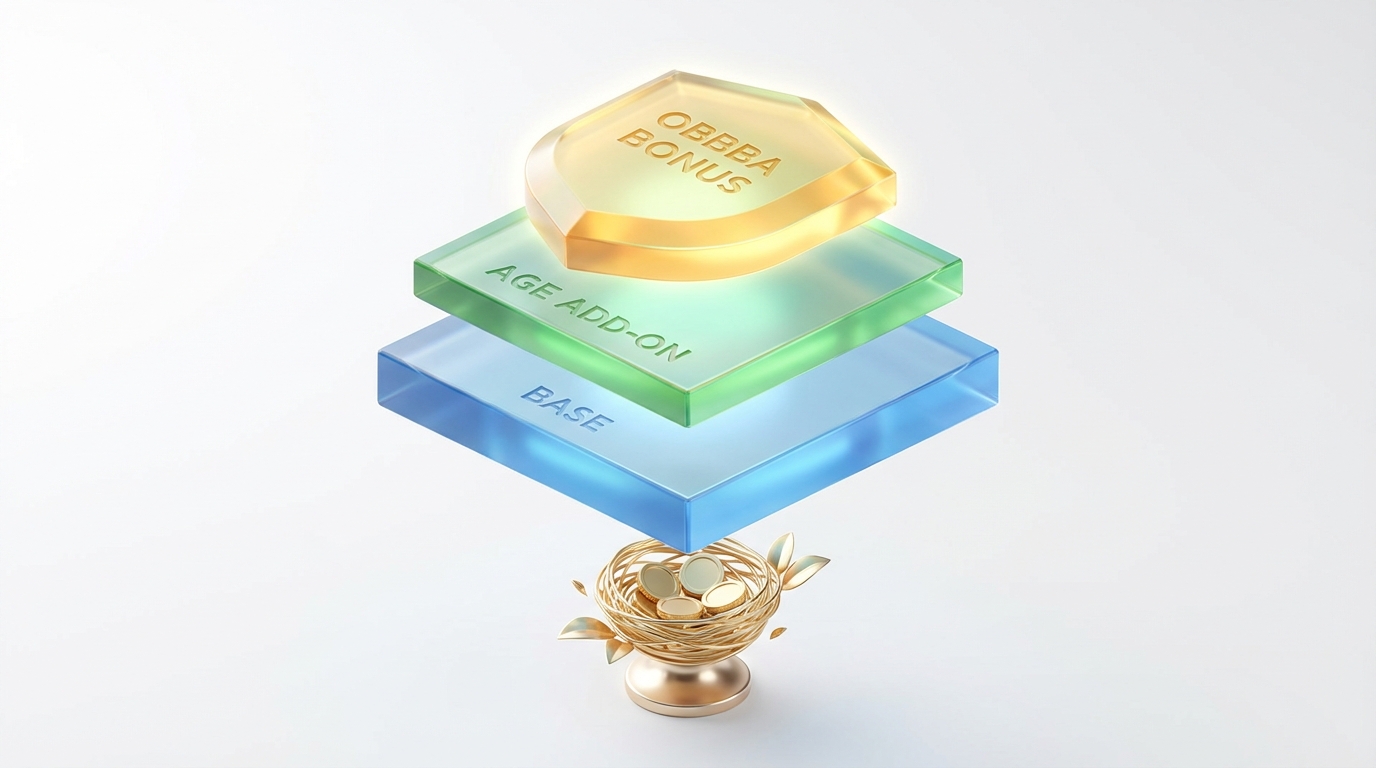

The OBBBA has fundamentally reshaped how retirees view their annual tax bill by introducing a “three-layer” deduction system. For the first time, seniors can stack a new “Bonus” deduction on top of the existing standard and age-related amounts. This creates a massive income shield, allowing a married couple to protect up to $46,700 from federal taxes. Engaging in professional tax planning for high net worth seniors is now essential to ensure you do not accidentally cross the income thresholds that trigger a phase-out of these new benefits.

The 2025 Deduction Stack

The following table illustrates how the OBBBA layers combine for taxpayers aged 65 and older. These figures represent the amount of income you can earn before the IRS begins applying the 2025 tax rates.

| Deduction Layer | Single (Age 65+) | Married Filing Jointly (Both 65+) |

|---|---|---|

| Base Standard Deduction | $15,750 | $31,500 |

| Traditional 65+ Add-on | $2,000 | $3,200 |

| NEW OBBBA Bonus | $6,000 | $12,000 |

| Total Potential Shield | $23,750 | $46,700 |

This expanded shield changes how you should view the 2025 federal income tax brackets for married filing jointly seniors. Because these deductions are subtracted first, your taxable income is often much lower than your gross income. For example, a couple earning $110,000 may find their taxable income drops to $63,300, keeping them firmly in the 12% bracket. This creates a unique opportunity for tax strategies for reducing capital gains in retirement, as many seniors will now fall under the 0% capital gains threshold.

To maximize these savings, retirees are increasingly asking how to minimize taxes on RMD distributions 2025. One of the most effective methods involves qualified charitable distribution strategies to lower taxable income, which keeps your Modified Adjusted Gross Income (MAGI) below the OBBBA phase-out levels ($75,000 for singles; $150,000 for couples). For complex estates, the best tax preparation services for retired business owners can help balance these deductions against static Social Security tax thresholds to prevent a “tax torpedo” effect on your benefits.

1. The New ‘Triple-Layer’ Standard Deduction

The passage of the “One, Big, Beautiful Bill Act” (OBBBA) on July 4, 2025, fundamentally rewrote the rules for retirees. For the 2025 tax year, the standard deduction is no longer a single flat number. Instead, it functions like a “triple-layer cake” that can significantly shield your retirement savings from the IRS. For many, this shift makes understanding the 2025 federal income tax brackets for married filing jointly seniors more important than ever, as your taxable income could drop to zero.

Layer 1 & 2: The Enhanced Foundation

The OBBBA officially raised the base standard deduction (Layer 1) to $15,750 for singles and $31,500 for married couples. On top of this, the traditional “65 or older” add-on (Layer 2) remains in effect. This adds $2,000 for single filers or $1,600 per spouse for those filing jointly ($3,200 if both are 65+). These two layers alone provide a massive buffer before a single cent of your Social Security or pension income is taxed.

Layer 3: The OBBBA “Bonus” Deduction

The most significant addition is the Layer 3 Bonus. This $6,000-per-person deduction is unique because you can claim it even if you choose to itemize your deductions. However, it is specifically targeted at low-to-moderate-income households. If your Modified Adjusted Gross Income (MAGI) exceeds $75,000 (Single) or $150,000 (Married), the bonus begins to phase out at a rate of 6% for every dollar over the limit.

To keep this bonus, many retirees are utilizing qualified charitable distribution strategies to lower taxable income. By sending RMDs directly to a charity, you keep your MAGI lower, preserving your eligibility for the full Layer 3 deduction. This is a core component of professional tax planning for high net worth seniors who want to avoid the 6% phase-out “tax” on their bonus deduction.

2025 Total Deduction Potential

| Deduction Layer | Single (65+) | Married (Both 65+) |

|---|---|---|

| Base (Layer 1) | $15,750 | $31,500 |

| Traditional Add-on (Layer 2) | $2,000 | $3,200 |

| OBBBA Bonus (Layer 3) | $6,000 | $12,000 |

| Total Potential Deduction | $23,750 | $46,700 |

Managing these layers requires precision. For example, knowing how to minimize taxes on RMD distributions 2025 or implementing tax strategies for reducing capital gains in retirement can prevent your income from creeping into the phase-out range. If you managed a company before retiring, the best tax preparation services for retired business owners can help navigate these complex OBBBA phase-out calculations to ensure you do not leave money on the table.

2. 2025 Tax Brackets & The Capital Gains Opportunity

Navigating the 2025 tax year requires a shift in strategy, especially for retirees looking to protect their wealth. With the introduction of the “One, Big, Beautiful Bill Act” (OBBBA), professional tax planning for high net worth seniors has become more critical than ever. These new rules adjust the standard thresholds, providing a unique window to realize investment gains without handing a large chunk to the IRS.

2025 Federal Income Tax Brackets

The IRS has adjusted the 2025 federal income tax brackets for married filing jointly seniors and individuals to account for inflation. However, the OBBBA legislation further modifies how these brackets interact with your total deductions.

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 10% | $0 – $11,925 | $0 – $23,850 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 |

The 0% Capital Gains Opportunity

The real power in the 2025 code lies in the Long-Term Capital Gains (LTCG) thresholds. If you can keep your taxable income below certain levels, your tax rate on sold assets held for over a year is 0%.

- Single Filers: 0% rate applies up to $48,350 of taxable income.

- Married Filing Jointly: 0% rate applies up to $96,700 of taxable income.

Maximizing the “Three-Layer” Deduction

To hit that 0% window, you must aggressively lower your taxable income. The OBBBA creates a massive deduction stack. For a 65+ couple, this includes a $31,500 base, a $3,200 age-based addition, and a new $12,000 “Bonus” deduction, totaling $46,700.

This stack is one of the most effective tax strategies for reducing capital gains in retirement. For example, a couple earning $110,000 can use these deductions to bring their taxable income down to $63,300. This leaves $33,400 of “room” to sell stocks at a 0% tax rate before hitting the $96,700 limit.

Managing this gap is also how to minimize taxes on RMD distributions 2025. By utilizing qualified charitable distribution strategies to lower taxable income, you can prevent Required Minimum Distributions from pushing you into a higher capital gains bracket. For complex estates, the best tax preparation services for retired business owners can help model these “harvesting” scenarios to ensure no tax-free opportunities are wasted.

3. New Rules: Tips, Overtime & The SALT Cap

The One, Big, Beautiful Bill Act (OBBBA) introduces major breaks for hourly workers and homeowners. These changes, effective for the 2025 tax year, aim to reduce the federal tax burden on those who rely on tips or extra hours to make ends meet. If you are still in the workforce, you can now deduct up to $25,000 in “qualified tips” from your federal taxable income. This applies to workers in industries like food service and hospitality. Keep in mind that while this lowers your income tax, you must still pay Social Security and Medicare taxes on that tip income.

Hourly employees also get a boost through the new “No Tax on Overtime” deduction. You can deduct the “premium” portion of your overtime pay—the extra amount earned above your base rate. The limit is $12,500 for single filers and $25,000 for those married filing jointly. If you are researching professional tax planning for high net worth seniors or still working part-time, note that these deductions phase out once your income exceeds $150,000 (or $300,000 for couples).

The SALT Cap Expansion

For homeowners in high-tax states, the State and Local Tax (SALT) cap expansion is a major relief. The previous $10,000 limit has jumped to $40,000 for most filers in 2025. This is a vital change for those looking at tax strategies for reducing capital gains in retirement or managing high property taxes. The cap begins to phase back down to $10,000 only if your income exceeds $500,000. For those seeking the best tax preparation services for retired business owners, these new SALT rules require careful documentation to maximize your itemized deductions.

Retirees should also consider how these changes interact with other income sources. For example, knowing how to minimize taxes on RMD distributions 2025 alongside these new deductions can lower your overall effective rate. You might also pair these breaks with qualified charitable distribution strategies to lower taxable income. By staying informed on the 2025 federal income tax brackets for married filing jointly seniors, you can better time your withdrawals and deductions to stay within lower tax tiers.

2025 Special Deductions Summary

| Provision | Max Deduction (Single) | Max Deduction (Joint) | Phase-out Starts (MAGI) |

|---|---|---|---|

| Qualified Tips | $25,000 | $25,000 | $150,000 |

| Qualified Overtime | $12,500 | $25,000 | $150,000 |

| SALT Cap | $40,000 (Limit) | $40,000 (Limit) | $500,000 |

Because 2025 is a transition year, the IRS is providing reporting relief for employers. If your W-2 does not separately list your overtime pay, you can still claim the deduction, but you must keep thorough records of your pay stubs. This flexibility ensures that workers can benefit from the new law even while payroll systems are being updated to meet the OBBBA requirements.

4. The ‘Hidden Traps’: MAGI Cliffs & Social Security

The 2025 tax year introduces a new “Bonus Senior Deduction,” but it comes with a significant catch. If your Modified Adjusted Gross Income (MAGI) exceeds specific limits, this benefit starts to phase out. This creates a “marginal tax cliff” where earning a few extra dollars could cost you more in lost deductions than the income is worth. Navigating these thresholds requires **professional tax planning for high net worth seniors** to avoid an artificially high effective tax rate.

| Filing Status | MAGI Phase-Out Threshold |

|---|---|

| Single | $75,000 |

| Married Filing Jointly | $150,000 |

The Social Security “Tax Torpedo”

While the new law adds deductions, it fails to update the decades-old thresholds for Social Security taxability. These limits are not indexed for inflation, meaning your annual cost-of-living adjustment (COLA) could push you into a higher tax tier. This “bracket creep” means more of your benefits are taxed every year, even if your standard of living hasn’t changed.

| Provisional Income Level | Taxable Amount of Social Security |

|---|---|

| $0 – $25,000 (Single) / $32,000 (Joint) | 0% |

| $25,001 – $34,000 (Single) / $32,001 – $44,000 (Joint) | Up to 50% |

| Over $34,000 (Single) / $44,000 (Joint) | Up to 85% |

The Capital Gains Stacking Trap

Many retirees are surprised to find their “tax-free” investment gains are suddenly taxable. The IRS “stacks” your capital gains on top of your ordinary income to determine your rate. If a large IRA withdrawal pushes your total taxable income past certain thresholds, your capital gains rate jumps from 0% to 15% instantly. Learning **how to minimize taxes on RMD distributions 2025** is essential to keep your income within the 0% bracket.

| Filing Status | 2025 Total Taxable Income Threshold (0% Rate) |

|---|---|

| Single | Up to $48,350 |

| Married Filing Jointly | Up to $96,700 |

To stay below these cliffs, consider **qualified charitable distribution strategies to lower taxable income** or other **tax strategies for reducing capital gains in retirement**. Understanding the **2025 federal income tax brackets for married filing jointly seniors** is the first step, but for complex portfolios, modeling these interactions is necessary before making a withdrawal that could trigger an unexpected tax bill.

5. Case Study: Robert & Mary’s $46,700 Shield

Robert and Mary, both 72, represent a classic retirement scenario with a combined gross income of $110,000 from pensions and Social Security. Without a clear strategy, a six-figure income often triggers the 22% tax bracket, significantly eroding retirement savings. However, by utilizing a multi-layered “shield,” they successfully navigate the **professional tax planning for high net worth seniors** space to protect their wealth.

The Anatomy of the $46,700 Shield

The couple’s strategy relies on stacking three distinct layers of deductions to lower their taxable income. This ensures they stay within the lower **2025 federal income tax brackets for married filing jointly seniors**, effectively migrating their tax responsibility from a perceived 22% down to an actual 12%.

| Deduction Layer | Benefit Amount |

|---|---|

| Base Standard Deduction | $31,500 |

| Traditional 65+ Add-on ($1,600 per spouse) | $3,200 |

| Bonus Senior Deduction (OBBBA Framework) | $12,000 |

| Total Shielded Income | $46,700 |

Strategic Impact on Taxable Income

By applying this $46,700 shield, Robert and Mary reduce their taxable income to just $63,300. This is a critical move for those learning **how to minimize taxes on RMD distributions 2025**, as it prevents mandatory withdrawals from pushing them into higher tax territory. Because their Modified Adjusted Gross Income (MAGI) remains well below the $150,000 threshold, their bonus deductions remain fully intact.

To achieve similar results, retirees should consider **qualified charitable distribution strategies to lower taxable income**, which can further reduce the impact of RMDs. Furthermore, incorporating **tax strategies for reducing capital gains in retirement** can help maintain a 0% rate on investment growth. For those transitioning from the workforce, the **best tax preparation services for retired business owners** can help identify these specific legislative “shields” to ensure not a single dollar is taxed at a higher rate than necessary.

FAQ: Common Questions About the 2025 OBBBA Rules

How does the OBBBA change my standard deduction?

The One, Big, Beautiful Bill Act (OBBBA) introduces a “Three-Layer” deduction system specifically for taxpayers aged 65 and older. This structure significantly increases the amount of income you can shield from federal taxes. For many, professional tax planning for high net worth seniors will focus on maximizing these layers to protect retirement savings from higher brackets.

| Deduction Layer | Single (65+) | Married (Both 65+) |

|---|---|---|

| Layer 1: 2025 Base | $15,750 | $31,500 |

| Layer 2: Traditional 65+ | $2,000 | $3,200 |

| Layer 3: OBBBA Bonus | $6,000 | $12,000 |

| Total Potential | $23,750 | $46,700 |

Can I still itemize my deductions?

Yes. A unique feature of the OBBBA is that the Layer 3 “Bonus” deduction is available even if you choose to itemize your other expenses. This is a major shift from traditional rules where you must choose between the standard deduction or itemizing. If you are looking for how to minimize taxes on RMD distributions 2025, this bonus provides a powerful new tool to lower your taxable income regardless of your filing method.

Are there income limits for the new bonus?

The OBBBA bonus is designed to help low-to-moderate-income seniors. The $6,000 or $12,000 deduction begins to phase out once your Modified Adjusted Gross Income (MAGI) exceeds $75,000 for individuals or $150,000 for those using the 2025 federal income tax brackets for married filing jointly seniors. If your income is above these levels, you may need tax strategies for reducing capital gains in retirement to keep your MAGI within the qualifying range.

How does this affect my investments and social security?

By increasing your total deductions, the OBBBA makes it easier to stay in the 0% long-term capital gains bracket. For example, a married couple could potentially earn significant income before paying a dime in capital gains taxes. Many retirees use best tax preparation services for retired business owners to coordinate these deductions with qualified charitable distribution strategies to lower taxable income, ensuring their social security benefits and portfolio growth remain as tax-efficient as possible.

About the Author

ARUN KP

With over 15 years of extensive experience in the accounting and taxation industry, Arun KP specializes in cross-border India-US taxation. As an Entrepreneur and AI Content Generator, he leverages cutting-edge technology to simplify complex financial landscapes for individuals and businesses.

Entrepreneur | AI Content Generator | India-US Tax Professional | Accountant

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice.