Date: 1/20/2026

The 2025 Pivot: OBBBA, The 60% Rule, and The Coming ‘Floor’

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, serves as the definitive legislative pivot for your financial strategy. While the law makes the current individual tax rates permanent, it introduces significant restrictions on giving that do not take effect until 2026. This makes 2025 a “clean year,” providing a unique window for **maximizing tax deductions for charitable donations** before the rules become more restrictive.

The Permanent 60% AGI Limit

A primary benefit of the OBBBA is the permanent extension of the **irs 60 percent adjusted gross income limit** for cash contributions. Previously, this limit was scheduled to revert to 50% after 2025. Now, you can indefinitely deduct cash gifts to qualified public charities up to 60% of your Adjusted Gross Income (AGI). If your generosity exceeds this ceiling in 2025, you can carry the excess deduction forward for up to five years.

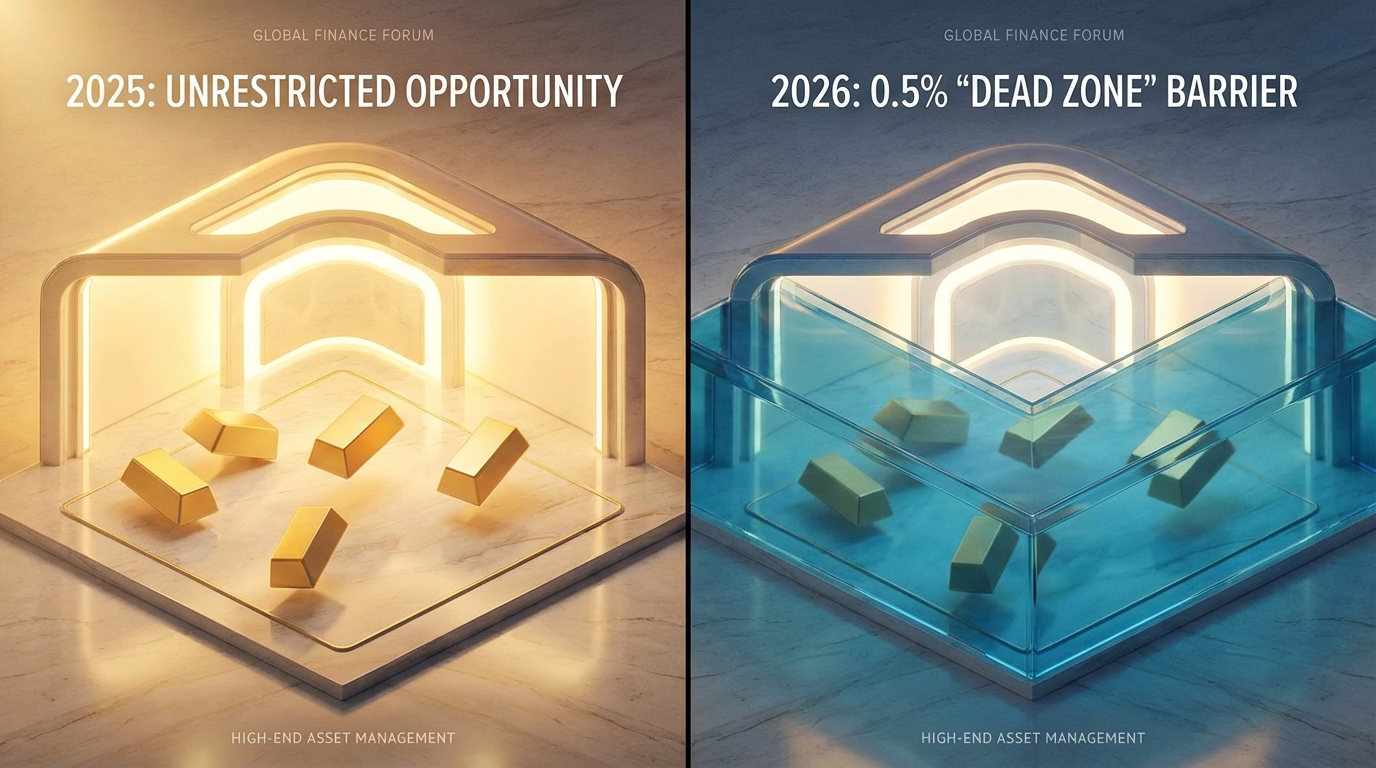

The 0.5% Floor: Navigating the “Dead Zone”

The most jarring change under the OBBBA is the implementation of a deduction floor starting in 2026. This creates a “dead zone” where your initial donations provide no tax relief. Under this rule, itemized contributions are only deductible to the extent they exceed 0.5% of your AGI. For example, if your AGI is $200,000, your first $1,000 in donations yields zero tax benefit. To bypass this, many taxpayers are “bunching” their 2026 and 2027 planned giving into 2025 to ensure every dollar remains deductible.

High-Net-Worth Strategy and Appraisals

For those in the highest tax bracket, **tax planning for high net worth charitable giving** requires extra care. Starting in 2026, a new savings cap effectively reduces the maximum tax value of a donation from 37% to approximately 35%. Furthermore, while cash limits are favorable, non-cash gifts like stocks remain capped at 30% of AGI. You must still secure a **qualified appraisal for non cash charitable contributions** for items exceeding $5,000 to meet IRS standards. Staying compliant with all **documentation requirements for large charitable donations** is essential to protecting these high-value deductions.

New Incentives for Non-Itemizers

If you take the standard deduction, the OBBBA offers a new permanent incentive starting in 2026. You will be able to claim an “above-the-line” deduction for cash gifts up to $1,000 (Single) or $2,000 (Married Filing Jointly). Notably, this specific deduction is exempt from the 0.5% AGI floor, making it a straightforward way to lower your taxable income without itemizing.

Summary of the 2025 vs. 2026 **charitable contribution deduction limits 2025**

| Provision | 2025 (Current) | 2026 (OBBBA Effective Date) |

|---|---|---|

| Cash Deduction Limit | 60% of AGI | 60% of AGI (Permanent) |

| Deduction Floor | None (Deduct from dollar one) | 0.5% of AGI Floor |

| Non-Itemizer Deduction | None | $1,000 (S) / $2,000 (MFJ) |

| Max Tax Benefit | 37% | ~35% (for high earners) |

The Numbers: 2025 Deduction Limits & Carryovers

Understanding the charitable contribution deduction limits for 2025 is the first step in ensuring your generosity effectively lowers your tax bill. The IRS uses your Adjusted Gross Income (AGI) as a yardstick to determine how much you can write off in a single year. If you give more than the allowed limit, you do not lose the deduction; instead, you carry the excess forward to future tax years for up to five years.

2025 AGI Caps by Donation Type

The type of asset you give determines your specific “ceiling.” While cash is the most flexible, non-cash assets like stocks offer significant tax advantages but come with tighter restrictions. This distinction is vital for tax planning regarding high-net-worth charitable giving.

| Donation Type | 2025 AGI Limit | Best For… |

|---|---|---|

| Cash / Check | 60% of AGI | Immediate liquidity needs for the charity. |

| Appreciated Assets (held >1 year) | 30% of AGI | Avoiding capital gains tax on stocks or property. |

The 2025 Itemization Hurdle

You only benefit from these limits if you “itemize” your deductions on Schedule A. This means your total expenses—including charity, mortgage interest, and state and local taxes (SALT)—must exceed the standard deduction. For the 2025 tax year, the thresholds and additional senior bonuses are as follows:

| Filing Status | 2025 Standard Deduction | Senior Bonus (Age 65+) |

|---|---|---|

| Single / Married Filing Separately | $15,750 | $6,000 |

| Married Filing Jointly | $31,500 | $12,000 |

| Head of Household | $23,625 | N/A |

Documentation and Substantiation Rules

The IRS enforces strict documentation requirements for large charitable donations to maintain compliance. If you fail to secure the right paperwork at the time of the gift, the IRS can disallow the entire deduction during an audit. For those maximizing tax deductions, follow these thresholds:

- Gifts of $250 or more: You must obtain a Contemporaneous Written Acknowledgment (CWA) from the charity.

- Non-cash gifts over $500: You must file IRS Form 8283 with your return.

- Non-cash gifts over $5,000: You generally must obtain a qualified appraisal from an independent professional (except for publicly traded securities).

- Volunteer Mileage: You can deduct 14 cents per mile driven for charitable purposes.

The “2026 Cliff” Warning

Proactive taxpayers should view 2025 as a “lock-in” year. Current legislative trends, including the IRS 60 percent adjusted gross income limit, are subject to change. New proposals suggest a 0.5% AGI “floor” could be introduced in 2026, meaning the first half-percent of your income donated would no longer be deductible. Giving heavily in 2025 ensures you receive the full value of every dollar donated before these potential restrictions take effect.

Strategy: Why You Must ‘Bunch’ Donations in 2025

For most taxpayers, the standard deduction has become a “tax-break ceiling” that is increasingly difficult to crack. In 2025, the standard deduction for married couples filing jointly rises to $30,000. If your combined mortgage interest, state taxes, and annual gifts do not exceed this amount, your charitable giving provides no additional tax benefit. By maximizing tax deductions for charitable donations through a strategy called “bunching,” you combine multiple years of giving into a single tax year to surpass that threshold.

The 2025 Standard Deduction Thresholds

To see why bunching is necessary, you must compare your expected itemized expenses against the 2025 IRS thresholds. Taxpayers only receive a tax benefit for their donations if their total itemized deductions exceed the following standard deduction amounts:

| Filing Status | 2025 Standard Deduction |

|---|---|

| Married Filing Jointly | $30,000 |

| Head of Household | $22,500 |

| Single / Married Filing Separately | $15,000 |

Navigating the 2025 Giving Limits

When you bunch donations, you must stay mindful of the charitable contribution deduction limits for 2025. The IRS limits the amount you can deduct based on your Adjusted Gross Income (AGI) and the type of asset donated, as shown in the table below:

| Contribution Type | 2025 AGI Deduction Limit |

|---|---|

| Cash Contributions to Public Charities | 60% |

| Appreciated Assets (e.g., Stocks) | 30% |

Any amount you give above these ceilings is not lost; you can carry the excess deduction forward for up to five years. This carryforward rule ensures that large “bunched” gifts remain tax-efficient even if they exceed a single year’s AGI limit.

Documentation is vital to protect your deduction. You must follow the documentation requirements for charitable donations, which include obtaining a contemporaneous written acknowledgment from the charity for any gift of $250 or more. By concentrating your giving into 2025, you ensure every dollar works harder for both your cause and your financial strategy.

The Receipt Trap: Strict Compliance or Zero Deduction

When it comes to the IRS, “close enough” is a recipe for a $0 deduction. For 2025, maximizing tax deductions for charitable donations requires more than just a generous heart; it requires a flawless paper trail. If you fail to meet specific documentation requirements for large charitable donations, the IRS can legally disallow your entire claim, even if you have a bank statement proving the money left your account. The agency does not allow for “substantial compliance” in this area, meaning a minor clerical error on a receipt can lead to a total loss of the tax benefit.

The $250 “Magic Language” Rule

The biggest pitfall for taxpayers is the $250 threshold. For any gift of this amount or more, you must obtain a written acknowledgment from the charity that contains specific “magic language.” This receipt must explicitly state whether you received any goods or services in exchange for your gift. If the receipt omits the phrase “no goods or services were provided,” the deduction is legally void. If a taxpayer donates an amount exceeding this threshold but the receipt lacks that specific clause, an auditor can strike the entire deduction, regardless of proof of payment.

Non-Cash Gifts and Appraisals

Donating physical items carries even stricter hurdles. While charitable contribution deduction limits 2025 allow for significant write-offs, items like clothing or household goods must be in “good condition” to qualify. If your non-cash gift exceeds $5,000, you must secure a qualified appraisal for non cash charitable contributions. This appraisal must be performed by a professional and documented on IRS Form 8283. If the appraiser signs but the charity fails to sign the “Donee Acknowledgment” section, the IRS routinely denies the deduction in full.

The Timing Trap

Timing is a common trap for taxpayers. You must have your receipts in hand before you file your tax return or before the filing deadline, whichever comes first. You cannot “fix” a missing receipt after an audit begins. This is particularly important for tax planning for high net worth charitable giving, where large sums are often subject to the irs 60 percent adjusted gross income limit for cash gifts. In recent Tax Court cases, such as Albrecht v. Commissioner, taxpayers lost six-figure deductions simply because their receipts were not contemporaneous or lacked the mandatory “no goods” language.

2025 Substantiation Quick Reference

| Threshold | Requirement | Consequence of Failure |

|---|---|---|

| Any Cash | Bank record or receipt | $0 Deduction |

| $75+ (Quid Pro Quo) | Written disclosure of item value | Partial Disallowance |

| $250+ | Written Acknowledgment (with “No Goods” language) | Total Disallowance |

| $500+ (Non-Cash) | Form 8283 (Section A) | Audit Risk / Disallowance |

| $5,000+ (Non-Cash) | Qualified Appraisal + Form 8283 (Section B) | Total Disallowance |

| 60% of AGI | Limit for Cash Contributions | Carryforward (5 years) |

Valuation Watchdogs: Crypto, Art, and Household Goods

When you clear out your closet or transfer Bitcoin to a non-profit, you aren’t just doing good—you’re navigating a complex web of IRS rules. For the 2025 tax year, understanding the charitable contribution deduction limits 2025 is essential to ensure your generosity actually lowers your tax bill. While cash gifts are straightforward, the IRS acts as a strict watchdog when it comes to the “Fair Market Value” (FMV) of physical and digital property.

The Crypto Appraisal Trap

Cryptocurrency is a major focus for the IRS right now. Even though you can see the price of Bitcoin or Ethereum on your phone in real-time, the IRS treats these assets as property, not currency. If your crypto donation exceeds $5,000, the law requires a qualified appraisal for non cash charitable contributions. A simple exchange screenshot is not enough. Failing to hire a human appraiser for high-value crypto gifts can result in the IRS disallowing your entire deduction, regardless of the asset’s clear market price.

Art, Collectibles, and High-Value Assets

For those engaged in tax planning for high net worth charitable giving, art donations carry high stakes. If you claim a piece is worth $20,000 or more, you must attach a signed copy of the appraisal to your tax return. For masterpieces valued at $50,000 or more, you can request a “Statement of Value” from the IRS Art Advisory Panel. This move “locks in” the valuation and helps you avoid a future audit. Remember that if a charity sells your donated art immediately rather than displaying it, your deduction may be limited to what you originally paid for it.

Household Goods: The “Good Condition” Rule

When maximizing tax deductions for charitable donations, don’t expect a tax break for junk. To qualify, clothing and household items must be in “good used condition” or better. You should deduct the thrift-store value—what a buyer would pay at a resale shop—rather than the original price you paid at the mall. If you are donating a single item worth over $500 that is not in good condition, you must include a qualified appraisal to justify the claim.

2025 Documentation Requirements

The following table outlines the documentation requirements for large charitable donations based on the value of your gift. Note that while cash gifts often fall under the irs 60 percent adjusted gross income limit, appreciated assets like art or crypto are generally capped at 30% of your AGI.

| Donation Value | Requirement | Watchdog Action |

|---|---|---|

| $500+ | Form 8283 (Section A) | You must list the date and manner of how you acquired the property. |

| $5,000+ | Qualified Appraisal | Required for Crypto, Art, and Jewelry; appraiser must sign Form 8283. |

| $20,000+ | Appraisal Attachment | A physical copy of the art appraisal must be filed with your return. |

| $500,000+ | Full Filing | The appraisal must be attached for all property types except cash or stocks. |

FAQ: Common Questions on 2025 Charitable Giving

Navigating the tax code can feel like a chore, but 2025 brings significant changes that could put more money back in your pocket. Thanks to recent legislation, the State and Local Tax (SALT) deduction cap has jumped to $40,000. This shift means more taxpayers will find it beneficial to itemize their deductions rather than taking the standard deduction, making it the perfect year for charitable contribution deduction limits 2025 to work in your favor.

If you are donating cash, the irs 60 percent adjusted gross income limit remains the primary benchmark for most taxpayers. This rule allows you to deduct cash gifts to public charities up to 60% of your Adjusted Gross Income (AGI). For example, if your AGI is $100,000, you can deduct up to $60,000 in cash donations. Any amount exceeding that limit doesn’t disappear; the IRS allows you to carry it forward to reduce your taxes for up to five years.

Strategic Giving for High-Value Assets

When it comes to tax planning for high net worth charitable giving, donating appreciated stocks is often a smarter move than giving cash. You can deduct the full fair market value of the stock and avoid capital gains tax entirely, though these gifts are generally capped at 30% of your AGI. However, you must be careful with high-value physical items like art or collectibles. A qualified appraisal for non cash charitable contributions is mandatory for any item (excluding publicly traded stock) valued over $5,000.

To ensure your deductions are safe from an audit, you must follow strict documentation requirements for large charitable donations. For any single gift of $250 or more, you need a written acknowledgment from the charity that confirms the amount and whether you received any goods or services in return. If you are maximizing tax deductions for charitable donations by giving away household goods, remember that items valued over $500 require you to file IRS Form 8283.

2025 Quick Reference Guide

| Donation Type | 2025 Limit | Key Requirement |

|---|---|---|

| Cash | 60% of AGI | Receipt for $250+ |

| Appreciated Stock | 30% of AGI | Held over 1 year |

| IRA Distribution (QCD) | $108,000 | Must be age 70½+ |

| Volunteer Mileage | 14 cents/mile | Log of miles driven |

For seniors, the Qualified Charitable Distribution (QCD) limit has increased to $108,000 for 2025. This allows you to transfer funds directly from your IRA to a charity, satisfying your Required Minimum Distribution (RMD) without adding a penny to your taxable income. This is a powerful tool for those who no longer need their full RMD for living expenses.

About the Author

ARUN KP

With over 15 years of extensive experience in the accounting and taxation industry, Arun KP specializes in cross-border India-US taxation. As an Entrepreneur and AI Content Generator, he leverages cutting-edge technology to simplify complex financial landscapes for individuals and businesses.

Entrepreneur | AI Content Generator | India-US Tax Professional | Accountant

Disclaimer: This article is for informational purposes only and does not constitute professional tax advice.